Frankincense Essential Oil Market Outlook 2034: Innovation, Demand, and Sustainability

Food |

2026-05-06 17:51:58

As companies reset strategies for 2026, PW Consulting’s newest Tubular Cable Lugs Market report provides the decision-grade intelligence executives need to convert uncertainty into competitive advantage. Our analysis synthesizes historical performance (2020–2025), a forward-looking forecast (2026–2032) and bespoke execution frameworks that translate market dynamics into boardroom actions. The market we modelled stood at approximately USD 432.5 Million in 2025 and, under our central scenario, grows at a compound annual growth rate (CAGR) of 7.25% across the 2026–2032 forecast window—reaching a materially larger basin of demand by 2032. This growth trajectory masks important inflection points and risk concentrations that buyers, manufacturers, and investors must navigate now.

Tubular Cable Lugs Market

Cost pressure from raw materials: Early‑2026 spikes in copper pricing (observed in the ~USD 12,000–14,500/tonne range) have immediate pass‑through implications for manufacturers who rely on electrolytic copper and ETP grades. Volatility in copper and aluminum prices reshapes margin profiles and forces urgent revisits of procurement and hedging policies.

Tubular Cable Lugs Market

Standards and product interoperability: Compliance with compression and dimension standards (for example, DIN 46235 for copper compression connections) is not optional for market access in many export markets. Product design changes—particularly for fine and superfine stranded conductor compatibility—are increasingly decisive in procurement evaluations.

Tubular Cable Lugs Market

Shifting demand drivers: Traditional power utilities and construction remain foundational demand pools, while electrification in automotive and growth in industrial manufacturing and renewable energy create differentiated growth pockets and service requirements.

Market structure and consolidation signals: The industry displays moderate concentration: our CR3 and CR5 metrics indicate leading suppliers hold meaningful share but do not dominate the entire value chain—creating deliberate M&A and partnership windows for mid‑market players and financial sponsors.

The report is intentionally tactical and operational. It avoids theory for theory’s sake and delivers tools leaders can deploy in the next 90–180 days. Highlights include:

Verified market sizing and trend maps covering 2020–2025 and a granular forecast for 2026–2032 expressed in USD Million, with scenario sensitivity to commodity prices and construction cycles.

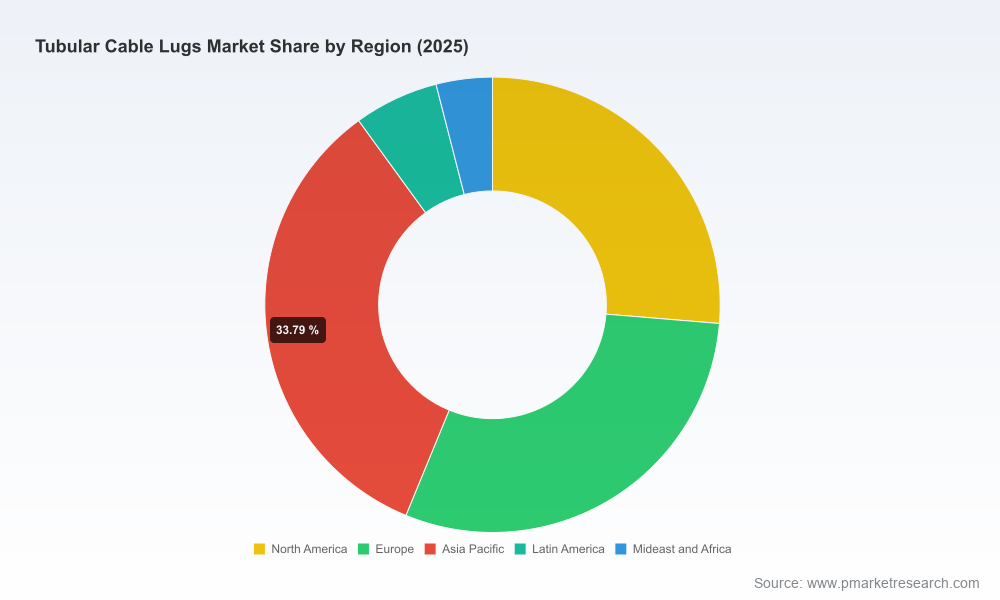

Segmentation frameworks by region, by product type (copper, aluminum, bimetallic tubular lugs), and by end-application (power utilities, construction, automotive, industrial, renewables) that identify where premium vs. volume strategies are most effective. Note: the public summary highlights directional splits; full segment tables and value-share matrices are reserved for report subscribers.

Pricing and margin modelling tools — including break-even maps for copper vs. aluminum manufacturing mixes, and a supplier cost‑to‑serve workbook that can be applied to specific SKUs and factories.

Competitive benchmarking and supplier scorecards that combine technical compliance, capacity, lead times, geographic reach, and after‑sales capabilities into a single actionable procurement ranking.

Deal origination playbook and a vetted shortlist of consolidation targets informed by market concentration indicators and partner fit criteria.

Operational playbooks: raw material hedging strategies, SKU rationalization templates, factory footprint optimization scenarios, and a rapid implementation checklist for product redesigns that improve compatibility with fine‑stranded conductors.

Risk heatmaps that translate macro inputs (commodity swings, regulatory changes, shipping disruptions) into probabilistic impacts on revenue and working capital.

The market is populated with technically proficient regional champions and a set of exporters that serve global OEMs. Our qualitative and quantitative diligence highlights several archetypes among incumbents and potential disruptors.

Klauke (Germany) — A European technical leader, noted for high‑quality copper tubular lugs and compliance with DIN/EN standards. Recent product updates (July 2025) redesigned two‑hole lugs with enlarged internal features to improve compatibility with fine‑stranded cables, reflecting a product development agenda oriented around conductor trends.

Pioneer Power International (India) — A broad manufacturer offering copper and aluminum tubular lugs and heavy‑duty XLPE types. Its strength lies in cost‑competitive manufacturing and diversified product breadth for both domestic and export markets.

MG Electrica (India) — ISO‑certified producer with a catalogue that spans copper and aluminum tubular lugs. The company released an updated price list and catalog in May 2025, signaling active commercial engagement and production continuity.

Axis Electricals (India) — UL‑listed manufacturer that emphasizes high‑conductivity ETP copper solutions targeting applications where electrical performance and safety certifications command price premiums.

Yueqing Lilian Electric Co., Ltd. (China) — Exporter/manufacturer serving global electrical markets with a wide SKU set; competitive on lead times for regional buyers and OEMs.

Apple International (India) — Specialized in battery cable ends and tubular lugs, a supplier to both aftermarket and OEM channels.

Collectively, the top three players account for a sizeable share of the market (our CR3 and CR5 metrics are included in the full report). This configuration creates strategic choices for buyers (consolidate to capture scale), suppliers (pursue differentiation through standards and services), and investors (selectively pursue bolt‑on acquisitions to scale footprint and technical capability).

Our analysis generates five near-term priorities for executives building robust 2026 plans:

Lock in material cost exposure. Deploy layered hedges and dual-sourcing contracts for copper and aluminum; incorporate commodity‑indexed clauses in customer contracts to protect margin. Use the report’s pricing sensitivity models to stress‑test scenarios by commodity price and lead time.

Accelerate product compliance and interoperability upgrades. Prioritize redesigns that align with DIN 46235 and fine‑stranded conductor trends; a small number of SKU investments can unlock new OEM contracts and reduce aftermarket returns.

Rationalize SKUs and optimize cost‑to‑serve. Apply our SKU rationalization template to reduce low‑velocity items and reallocate capacity to higher‑margin threaded, bimetallic, or specially plated lines.

Pursue targeted M&A and partnership plays. Given the industry’s moderate concentration, bolt‑ons that add geographic reach or specialized plating/pressing capability are high‑impact. The report includes diligence checklists and valuation multiples tailored to the sector.

Embed resilience into supply networks. Map single‑point failures, re‑optimize safety stock for critical terminals, and regionalize inventory to control lead times—supported by our supplier scorecards and supply chain playbooks.

The value of market intelligence is realized through action. PW Consulting’s Tubular Cable Lugs report is structured to be operational: board briefs for C-suite alignment, a working Excel model for financial planners, procurement scorecards for category managers, and an M&A playbook for strategy teams. For clients seeking faster execution, we offer tailored strategy workshops and scenario simulations that apply the report’s models to company‑specific cost and product portfolios.

Leadership in the tubular cable lugs sector in 2026 will be defined less by forecasting certainty and more by the speed at which firms translate risk into strategic choices—hedging material exposure, upgrading compliance‑led product design, and selectively consolidating capabilities. PW Consulting’s report equips decision makers with the quantified market view (historical 2020–2025, base year 2025, and forecast 2026–2032), competitive diagnostics, and practical toolkits to prioritize capital, procurement, and product decisions that preserve margin and accelerate growth.

For access to the full dataset, proprietary segment tables, and the complete set of implementation tools referenced in this release, please visit PW Consulting’s Tubular Cable Lugs Market report page. The public summary is intended as a substrate for decision making — the full report provides the granular models and actionable appendices that senior teams use to build 2026 plans with confidence.

For detailed analysis of this topic, please visit the official page:Tubular Cable Lugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com