MOCVD Systems Market 2025 Growing at 8.7% CAGR Through 2034 Driven by Compound Semiconductors

Other |

2026-06-16 09:46:42

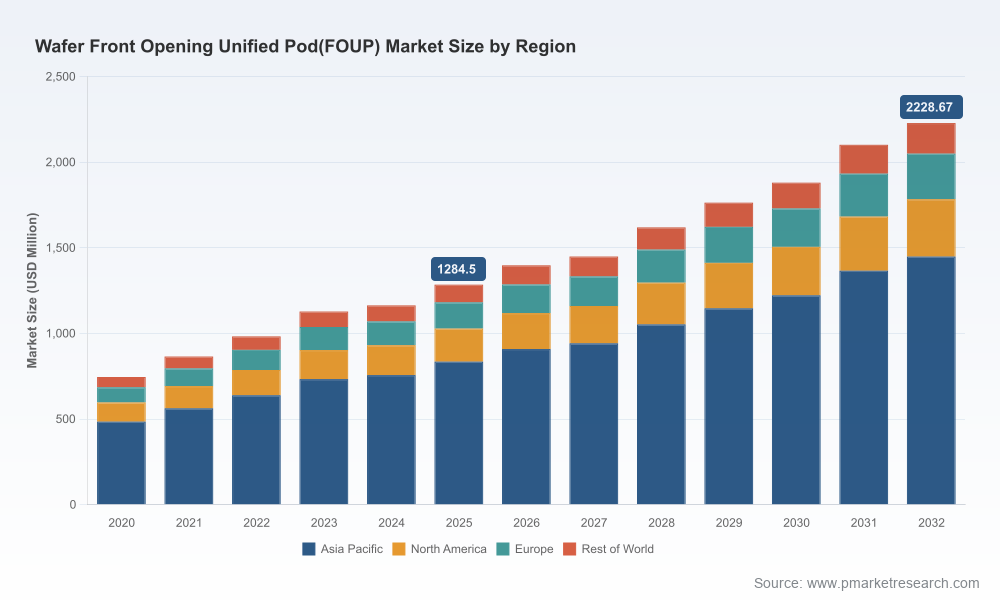

Our new Wafer Front Opening Unified Pod (FOUP) market study, anchored on a 2025 base year and projecting through 2032, delivers a focused playbook for semiconductor OEMs, equipment suppliers, materials vendors, and fabs planning capital and operational investments in 2026. The market demonstrates resilient expansion driven by automation, advanced-node processing requirements, and specialization for non‑standard substrates. From a macro perspective, the global FOUP market is positioned for steady growth at a compound annual growth rate (CAGR) of 8.19% across the forecast window — a pace that amplifies the financial and operational impact of each FOUP design and procurement decision in fab roadmaps.

Wafer Front Opening Unified Podfoup Market

Timing: 2026 is a pivotal year for capital allocation: many fabs are shifting from prototype and pilot lines to production scale for advanced packaging and 3D-stacking workflows. FOUP selection now affects throughput, yield, and contamination risk for the next generation of process nodes.

Wafer Front Opening Unified Podfoup Market

Scale effects: the market size trajectory we model shows continued expansion beyond the 2025 base, underscoring that small percentage improvements in FOUP uptime, purge performance, or automation compatibility translate into material bottom‑line gains for high-volume fabs.

Wafer Front Opening Unified Podfoup Market

Concentration and partner selection: the FOUP market is highly concentrated. The top three vendors account for roughly 72%+ of market supply, with the top five surpassing 88% — a structure that shapes negotiations, lead times, and co‑development opportunities.

Market sizing and scenario forecasts: a 2020–2025 historical baseline and a 2026–2032 forecast offering base, upside, and downside scenarios calibrated to semiconductor capex cycles and adoption curves for advanced-node and 3D substrates.

Supply-side mapping: vendor profiles, capacity and capability overlays, and a supplier‑selection framework that factors dimensional standards, microenvironment control, purge technologies, and AMHS compatibility.

Procurement playbook: a prioritized checklist for specification, qualification, and long‑lead procurement, including recommended test protocols, FAT/SAT considerations, and contract language to mitigate contamination and obsolescence risk.

Design-for-manufacturability (DFM) guidance: practical recommendations for FOUP integration with loadports, EFEMs, and automated handling systems to minimize cycle time impact and maintain cleanroom integrity for thin, warped, and 3D-stacked wafers.

Regulatory and standards mapping: consolidated guidance on SEMI standards relevant to FOUPs and related interfaces, and what practical compliance looks like during vendor qualification and fab integration.

Supply‑chain stress tests: scenario analyses for raw material price volatility, capacity constraints, and regional supply interruptions, supplemented with hedging and sourcing options for critical polymers and components.

Our model shows a market that expands meaningfully beyond the 2025 base year. The combination of node migration, increasing AMHS penetration, and packaging innovations means FOUP demand will be both larger and more technically demanding. For buyers and investors, this results in three operational imperatives for 2026: accelerate FOUP qualification cycles for advanced substrates, negotiate longer lead‑times with selected suppliers to secure continuity, and invest in FOUP testing that mirrors in‑fab edge cases (e.g., thinned wafers, non‑standard carriers).

The FOUP sector blends a few global leaders with strong engineering portfolios and a range of regional specialists focused on niche performance or cost leadership. The following strategic observations summarize comparative strengths and likely partner roles in 2026:

Entegris (United States): Positions itself as a technology leader in microenvironment control and advanced wafer isolation. Their product families emphasize contamination control, handling thin/warped wafers, and automation interoperability. For fabs targeting aggressive yield improvements at advanced nodes, Entegris remains a top candidate for co‑engineering and high‑spec FOUP programs.

Shin‑Etsu Polymer (Japan): A high‑precision molding and materials specialist that brings strength in manufacturing consistency and material engineering. Their approach suits customers prioritizing dimensional accuracy and large‑volume supply with established quality processes.

Miraial Co., Ltd. (Japan): Differentiates on standards compliance and long-term operational stability, delivering solutions optimized for continuous high‑availability production. Their profile is attractive where tight SEMI compliance and low lifetime TCO are priorities.

ePAK International (United States): Offers modular, AMHS‑friendly carriers with multiple purge options and practical AMHS integration features. ePAK’s catalog approach is useful for fabs seeking flexible platforms that can be tailored quickly without full custom development.

Gudeng Precision (Taiwan) and regional manufacturers: Provide cost‑sensitive options and rapid customization cycles, with increasing capability around purge functions and E‑series SEMI compliance. These vendors often serve fast‑moving local projects and secondary capacity needs.

Other specialist players (e.g., Pozzetta, 3S Korea, Chuang King, Dainichi Shoji): Typically fill niches around high‑mix lines, specialized carrier formats, or regional OEM partnerships. Their agility can be an advantage for pilot lines or non‑standard substrate programs.

Product refreshes and trade show activity continue to drive standards‑level interoperability. Exhibitions and catalog updates in 2025 demonstrated vendor priorities around purge performance, AMHS compatibility, and diffusion control — all trends we expect to accelerate in 2026.

Raw material moves: Polycarbonate pricing has diverged by region in early 2026, with notable softness in parts of Northeast Asia and firmer levels in some European markets. These input cost swings will influence supplier pricing strategies and sourcing decisions for large buyers during contract renewals.

Standards and compliance: SEMI standards remain the baseline for interoperability and automation. We see increasing emphasis on higher‑resolution dimensional and contamination metrics as fabs push advanced and non‑standard wafer formats into production.

For operating fabs and equipment OEMs, the immediate actions should be tactical and measurable:

Procurement: Lock in multi‑year supply agreements for FOUPs in parallel with validation contracts that include performance SLAs tied to contamination and handling metrics.

Testing: Expand in‑house FOUP qualification to include stress cases for thinned, warped, and stacked wafers. Replicate AMHS integration testing at scale prior to production ramp to avoid late‑stage interface issues.

Supplier strategy: Prioritize a dual‑sourcing approach where possible — a primary technology partner for co‑development and a regional supplier for capacity and cost flexibility. Use the market’s concentration structure to negotiate technology transfer or joint development slots.

Risk management: Monitor polymer market indicators and incorporate price‑adjustment clauses or hedging strategies into procurement to insulate fabs from short‑term volatility.

In keeping with our “trailer” approach, this release intentionally omits the granular regional, application, and type splits that form the core of our competitive and go‑to‑market modeling. Those segment‑level matrices, vendor share maps, and supplier pricing curves are included in the full PW Consulting report and are essential for tactical sourcing and investment decisions. We designed this brief to provide enough directional clarity for 2026 planning while reserving the detailed, executable datasets for clients and licensed report purchasers.

Scenario planning: Align capital budgets with the report’s three demand scenarios to stress test FOUP-related procurement across conservative, base, and aggressive fab‑ramp assumptions.

Vendor due diligence: Use our supplier scorecards to fast‑track vendor qualification, focusing on microenvironment metrics, automation compatibility, and proven performance on non‑standard wafers.

Negotiation playbook: Leverage market concentration insights and supply‑chain stress test outputs to structure contracts that balance availability, price stability, and performance guarantees.

For executives allocating CapEx and operations teams finalizing production integrations in 2026, this FOUP market context is more than market sizing — it’s a decision accelerator. The forecasted growth trajectory and concentrated supplier base mean that choices made this year on FOUP partners, interface standards, and qualification rigor will materially affect yield, throughput, and time‑to‑volume for advanced processes. PW Consulting’s full report contains the segment‑level intelligence, vendor shares, and test protocols necessary to operationalize these choices; consider this brief your strategic heads‑up and a prompt to engage the full dataset before committing to long‑lead equipment and supply contracts.

For access to the complete analysis, supplier scorecards, and procurement templates, please visit PW Consulting’s market report portal or contact our industry practice to schedule a tailored briefing.

For detailed analysis of this topic, please visit the official page:Wafer Front Opening Unified Podfoup Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com