PW Consulting Strategic Brief: 10B Enriched Potassium Fluoroborate Market — A 2026 Decision-Maker’s Guide

Our newly published 10B Enriched Potassium Fluoroborate (K10BF4) market study — anchored on 2025 as the base year and projecting through 2032 — converts complex supply-chain realities into operational choices for industrial buyers, system integrators, and strategic planners. The market has expanded materially in the past half-decade and continues to compound: the research shows a steady increase from the early-2020s and an expected trajectory to 2032 at a compound annual growth rate (CAGR) of 6.41%. For executives planning capital allocation, sourcing, or M&A in 2026, this report is a tactical instrument for converting uncertainty into competitive advantage.

10B Enriched Potassium Fluoroborate Market

Why this matters for 2026 corporate strategy

- Procurement certainty in a concentrated market: The supply base for isotopically enriched boron compounds is highly concentrated. A small group of industrial processors and regional distributors account for the majority of commercially available product. That structural concentration amplifies supplier leverage and raises the bar for rigorous qualification and multi-sourcing strategies.

- Capital and operational planning: Forecasted market expansion through the next decade implies persistent demand for enriched boron across nuclear, semiconductor, and specialty materials applications. Organizations deciding on capex, inventory policy, or plant qualification programs in 2026 need a data-driven view of both near-term availability and medium-term price risk.

- Regulatory and logistics constraints: Enriched isotopes are subject to technical export controls, handling and transportation restrictions, and security protocols that materially affect lead times and total landed cost. These non-price frictions must be embedded into vendor selection and contract design.

- Technology and product specification: The isotopic enrichment of boron (commonly delivered at enrichment levels above 95–96% and, in some commercial offers, exceeding 99%) materially alters application performance and qualification pathways. Choosing enrichment level is a trade-off between unit cost and component/system performance that must be assessed case-by-case.

What PW Consulting’s report delivers (practical, usable content)

- Transparent market-sizing and a reproducible methodology: clear assumptions, historic baselines, and a scenario-driven forecast through 2032 that executives can adapt to their portfolio.

- Supply-map and supplier scorecard: verified profiles of leading processors and regional distributors, multi-dimensional supplier scoring (capacity, enrichment capability, regulatory posture, commercial terms), and a supplier risk index that supports procurement prioritization.

- Commercial playbook for contracting: recommended clauses for lead-time guarantees, price adjustment mechanisms, force majeure treatment specific to isotope manufacture, and sample term-sheet language for multi-year supply agreements.

- Operational checklists: inbound quality acceptance, isotopic verification protocols, storage and handling requirements, and logistics routing to minimize compliance risk.

- Scenario models and stress tests: demand-shock, supply-constriction, and regulatory-shock scenarios with actionable mitigation paths — inventory buffers, dual-sourcing triggers, strategic outsourcing, and contingency manufacturing partners.

- Cost and price sensitivity tools: unit cost curve estimations, break-even analyses for vertical integration vs. long-term contracting, and guidance on when to pursue strategic inventory investments.

Competitive landscape — who matters and what to watch

The market’s operational reality is shaped by a small set of technically capable firms and specialized distributors. Our analysis highlights three types of participants and their strategic implications:

10B Enriched Potassium Fluoroborate Market

- Large processors with proprietary enrichment technology: Global processors with in-house isotope enrichment capabilities can offer ultra-high enrichment grades and faster qualification for critical nuclear applications. These players tend to set technical benchmarks and are pivotal in global supply assurances.

- Integrated specialty-chemical manufacturers: Corporations that produce enriched boron compounds as part of a broader portfolio can leverage scale and cross-selling to stabilize commercial availability. Their continued commercial offerings and corporate disclosures indicate ongoing investment in production continuity.

- Regional distributors and application-focused suppliers: Local partners are essential for downstream qualification, just-in-time delivery in sensitive markets, and regional regulatory navigation. These distributors often provide the bridge between global processors and end users in regulated industries.

Three commercial names referenced repeatedly in primary-source interviews and filings are illustrative of these archetypes: a major global technical-ceramics and enrichment processor, a Japanese specialty-chemicals producer with confirmed mass-production capability for enriched boron compounds, and regional distributors that manage end-market integration in East Asian markets. Our report includes verified corporate profiles, recent corporate developments confirming ongoing commercial availability, and an implications matrix for partnership, procurement, or defensive strategic moves.

10B Enriched Potassium Fluoroborate Market

Market dynamics and technical considerations you cannot ignore

- Neutron absorption potency: The boron-10 isotope has significantly higher thermal neutron cross-section than natural boron; that differential is the core technical rationale for specifying enriched material in radiation-control and spent fuel applications. This physics-driven value proposition makes enrichment level a mission-critical specification rather than a cost-only trade.

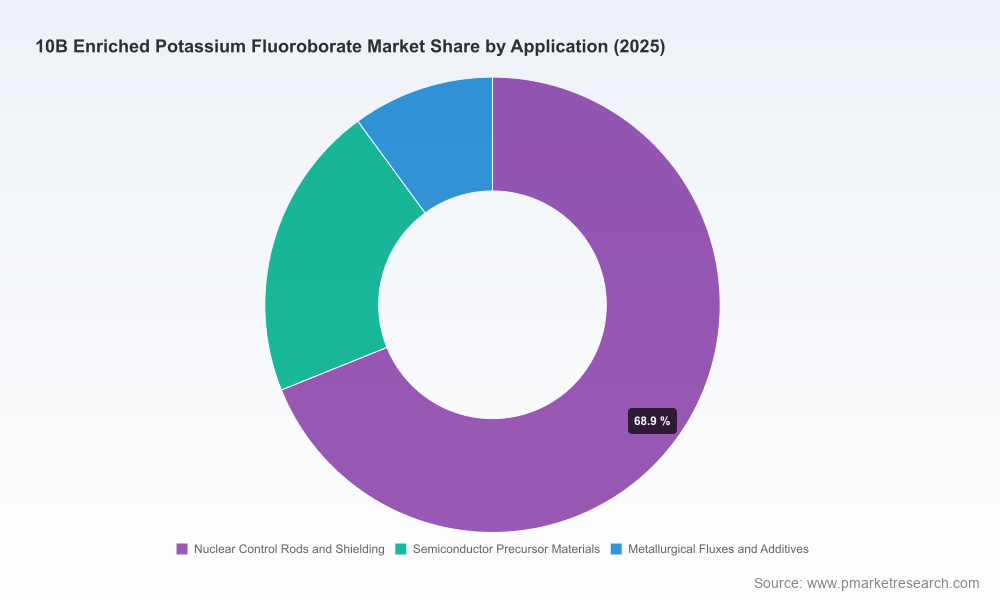

- Application diversity — different buyers, different drivers: End markets include neutron control and shielding for nuclear installations, precursors for advanced semiconductor processes, and specialty metallurgical additives. Each buyer cohort has distinct acceptance criteria, certification pathways, and commercial tolerance for supply risk.

- Constrained and specialized manufacturing: Isotopic enrichment and associated chemical processing are capital- and expertise-intensive. Manufacturing is geographically concentrated and requires long qualification times; therefore, capacity expansions are multi-year decisions with significant lead time.

- Policy and regulatory sensitivity: Changes in nuclear policy, spent-fuel management strategies, or export control regimes can rapidly reallocate demand and alter the cost of compliance for suppliers and buyers alike.

Outlook to 2032 — scenarios that should shape 2026 plans

Our baseline forecast, which assumes continuation of current nuclear fleet management policies and gradual recovery in semiconductor cycles, projects material market growth through 2032 with the mid-decade period representing an important inflection for procurement commitments. Under an accelerated nuclear-build scenario, demand rises faster and premium material grades command a larger share of procurement budgets. Under a constrained-supply scenario — driven by export restrictions, unplanned plant outages, or sudden surges in regional demand — buyers face higher premiums and extended lead times.

For 2026, the policy takeaway is clear: organizations should avoid binary choices (buy now vs. wait) and instead build flexible strategies that include staged procurement, supplier diversification, and contractual protections that kick in under specific supply-stress triggers. The report provides modeled P&L impacts across these scenarios to facilitate board-level discussions during the 2026 planning cycle.

Practical action checklist for executives in 2026

- Initiate verified supplier diligence immediately: prioritize technical audits, enrichment verification testing, and contractual clauses for isotopic compliance.

- Negotiate staged multi-year frameworks rather than single-year spot buys: combine fixed-volume and volume-flex windows to balance price and availability.

- Qualify at least one alternative supplier and one regional distributor for each critical site to reduce single-source exposure.

- Incorporate regulatory and logistics buffers into lead-time assumptions and total cost models.

- Run a 12–24 month stress test on inventory policies: compute the cost of carrying safety stock versus the risk-adjusted cost of supply disruptions.

- Explore strategic partnerships or JV options with enrichment-capable suppliers if securing guaranteed long-term supply is mission-critical to your operations.

Why PW Consulting’s 10B Enriched Potassium Fluoroborate report is a 2026 must-have

- Primary-source verification: supplier disclosures, corporate filings, and executive interviews are triangulated to reduce informational blind spots.

- Action-first deliverables: instead of only analysis, the report includes operational templates, contractual language, and step-by-step qualification and logistics checklists tailored to procurement and engineering teams.

- Strategic scenario toolset: executives receive not just point forecasts but a set of decision-preserving scenarios and quantified impacts to support board-level capital allocation conversations.

- Confidential client support: for organizations needing tailored supply-risk mapping or supplier engagement playbooks, PW Consulting provides advisory retainers to operationalize the findings.

We intentionally limit detail in this public brief to preserve the strategic value of the underlying dataset and to encourage direct engagement. The full report contains granular segmentation, supplier-level capacity triangulation, price and cost curves, and downloadable procurement templates that are essential for executing the 2026 actions outlined above.

To access the full intelligence package, model, and implementation toolkit, please consult the official PW Consulting report page for the 10B Enriched Potassium Fluoroborate Market. The deeper datasets and supplier analyses contained therein are designed to be directly operationalized by procurement, engineering, and corporate strategy teams in 2026.

For detailed analysis of this topic, please visit the official page:10B Enriched Potassium Fluoroborate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com