Human Elisa Kits Market: Strategic Preview for 2026 Decision‑Making

Executive Snapshot

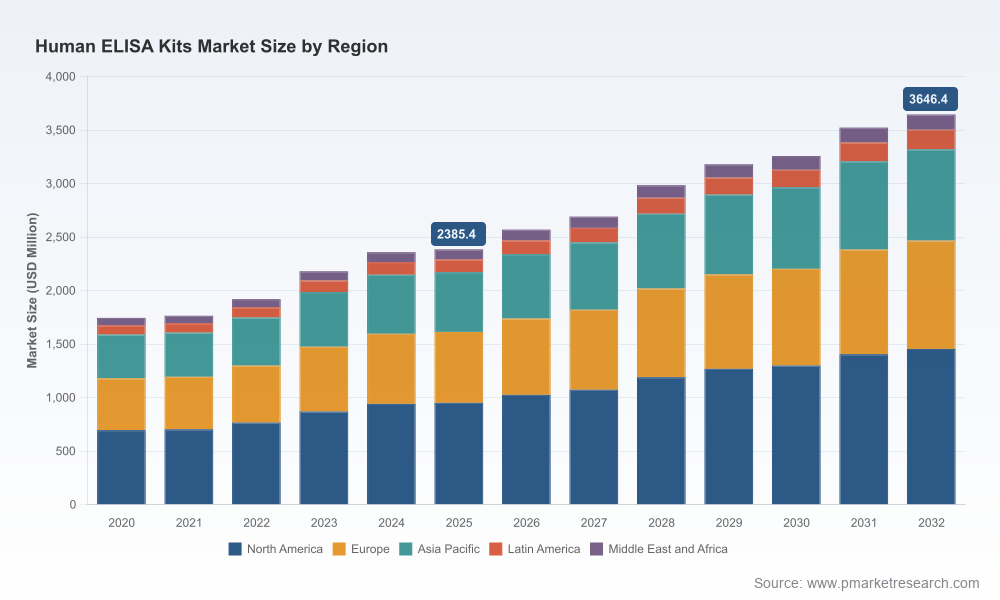

PW Consulting’s latest industry brief on the Human Elisa Kits market synthesizes five years of historical performance and a seven‑year outlook to provide boards, business units, and investors with an actionable strategic framework for 2026. The market has expanded from the mid‑single billions in 2020 to roughly USD 2.39 billion in 2025, and our base‑case forecast shows continued, steady growth—driven by research demand, select clinical assay conversions, and steady technological refinement—at a compound annual growth rate (CAGR) of 6.25% through 2032, when the market is projected to approach USD 3.65 billion.

Human Elisa Kits Market

Why 2026 Is a Strategic Inflection Point

Three converging dynamics make 2026 especially important for commercial and product strategy in the ELISA kit value chain:

Human Elisa Kits Market

- Normalization of post‑pandemic research funding patterns and renewed emphasis on translational pipelines that convert research assays into regulated diagnostics.

- Intensifying buyer expectations around kit robustness, supply certainty, and documented validation data—factors that favor vendors with both broad assay portfolios and demonstrable quality systems.

- Regulatory clarifications and high‑profile approvals (including a 2025 FDA de novo authorization for a companion diagnostic ELISA) that are lowering the perceived technical and regulatory risk of targeted IVD conversions.

What the Full Report Contains (Practical, Actionable Deliverables)

Our report is structured as a working toolkit for executives executing growth, risk‑mitigation, and M&A plays. Highlights include:

Human Elisa Kits Market

- Market sizing and trajectory: verified historical series (2020–2025), base‑year normalization (2025), and a quantified forecast through 2032 with scenario bands and sensitivity tables.

- Commercial playbooks: go‑to‑market approaches for research kits versus IVD conversions, tender and institutional procurement mapping, and pricing‑model templates tuned for margin recovery in 2026–2027.

- Regulatory navigation: a concise decision tree differentiating RUO, RUO‑to‑IVD transition steps, and pathways for companion diagnostics—illustrated with recent case precedent and checklist for pre‑submission readiness.

- Manufacturing and quality assessment: practical KPIs for bench‑level QC, supplier audit checklists, and capital planning assumptions for scaling ISO‑compliant production capacity.

- Technology and product roadmaps: prioritization matrices for assay sensitivity, multiplexing, automation compatibility, and reagent stability that correlate to commercial uplift in target end‑markets.

- M&A and partnership templates: diligence scorecards, valuation stress tests, and three archetype inorganic plays (bolt‑on, platform consolidation, and capability buy) with example thresholds for 2026 dealmaking.

- Risk register and mitigation playbook: supply‑chain scenarios, IP and patent landscape flags, and contingency plans for sudden regulatory or reimbursement shifts.

To preserve the report’s commercial utility for subscribers, we intentionally present high‑granularity analysis and interactive segment tables only in the full publication—this brief is designed to signal strategic direction while directing practitioners to the detailed datasets and annexes.

Competitive Landscape: Who Matters and Why

The market exhibits moderate concentration: the top three firms account for a material but not overwhelming share of commercial activity, and the top five firms represent just over half of the industry footprint—conditions that create space for both incumbent scale plays and targeted challengers. The names to monitor closely are a mix of legacy life‑science platforms, highly cited assay specialists, and vertically integrated kit manufacturers.

- Bio‑Techne (R&D Systems) — recognized for an extensive catalog and high citation rates across research publications. Their breadth of target analytes and reputation for reagent quality make them a de‑facto standard in many discovery workflows; this confers cross‑sell advantages when customers migrate assays toward validation phases.

- Thermo Fisher Scientific — strong channel reach and diversified life‑science offerings enable bundled solutions (kits + instrumentation + consumables), which is a defensive moat for retaining enterprise customers who prefer single‑vendor procurement simplicity.

- Abcam — momentum in citation growth and focus on high‑specificity assays positions Abcam as an influential player in research laboratories that require reproducible, validated reagents.

- Bio‑Rad Laboratories — its ELISA MAX collections and platform compatibility speak to customers in immunology and biomarker discovery where platform reproducibility and standardized protocols are essential.

- Emerging and specialist vendors (Boster Biological Technology, BioLegend, LSBio, Elabscience, Biomatik, ICL Lab, Proteintech, Surmodics IVD) — these firms combine focused product lines, manufacturing certifications (notably ISO 13485 for select vendors), and service differentiators such as rapid fulfillment, ready‑to‑use formats, or validated natural sample kits.

The practical implication for 2026: incumbents will continue to compete on portfolio depth, quality documentation, and channel scale, while specialist vendors compete on speed, targeted validation data, and price/performance niche wins.

Regulatory and Quality Dynamics That Shape Commercial Strategy

Two regulatory realities are central to positioning and go‑to‑market choices:

- Most commercially available human ELISA kits remain designated for Research Use Only (RUO); this simplifies market access but constrains clinical adoption and reimbursement pathways.

- When kits move into clinical use—as companion diagnostics or regulated IVDs—they typically require formal authorization (e.g., FDA de novo routes), higher documentation burdens, and tighter manufacturing controls. The 2025 FDA de novo approval for a companion diagnostic ELISA underscores that such transitions are achievable but require deliberate regulatory and evidentiary investments.

For manufacturers, an explicit RUO vs IVD strategy should be a board‑level decision in 2026: the revenue uplift from clinical adoption must be balanced against the time, cost, and organizational changes required for regulated manufacturing and post‑market surveillance.

Strategic Recommendations for 2026 Decision‑Makers

- Articulate a clear product classification roadmap. Define which assays are kept in the RUO channel and which will be targeted for IVD conversion, using a near‑term (12–24 month) priority list based on clinical need and ease of validation.

- Invest in quality and supply‑chain resilience. ISO‑aligned manufacturing and supplier diversification are increasingly table stakes; firms without robust QC and contingency logistics face commercial leakage during demand spikes.

- Pursue modular partnerships. Collaborations with diagnostic companies, labs, or contract manufacturers can accelerate IVD timetables while preserving capital—especially attractive for firms that lack deep regulatory expertise.

- Differentiate on validation data and documentation. For research markets, shorten adoption cycles by publishing third‑party validations and reproducibility studies; for clinical targets, allocate resources to prospective studies that support regulatory submissions.

- Prioritize product features that align with automation and multiplex workflows. Buyers increasingly select kits compatible with high‑throughput platforms and laboratory automation to improve throughput and reduce total cost of testing.

- Screen M&A targets with a two‑lens approach: immediate commercial synergies (sales channels, complementary assays) and strategic capability buys (ISO‑certified manufacturing, clinical validation know‑how).

How PW Consulting’s Offering Amplifies 2026 Outcomes

Clients who deploy the full PW Consulting dataset and the associated consulting engagement receive:

- Customizable financial models tied to the forecast scenarios in the report, enabling C‑suite teams to stress‑test acquisition paybacks and new product roll‑out economics.

- Go‑to‑market playbooks that convert market intelligence into sales targets, distributor scorecards, and promotional messaging tested against buyer personas.

- Regulatory readiness checklists and an engagement plan that map evidence generation to submission milestones for target jurisdictions.

Conclusion — What to Act on Now

2026 represents a window in which deliberate strategic moves—building ISO‑grade manufacturing resilience, selectively converting high‑value RUO assays to IVD, and crystallizing partnership approaches—will deterministically shape market position over the next five to seven years. PW Consulting’s full Human Elisa Kits Market report contains the granular segment tables, regional and application breakdowns, company scorecards, and annexes that operational teams need to convert this preview into executable plans. For executives needing immediate decision support, PW Consulting offers tailored briefings and scenario workshops that translate the report’s findings into board‑ready investment cases.

For detailed analysis of this topic, please visit the official page:Human Elisa Kits Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com