Construction Site Dumper Market 2026: Strategic Imperatives from PW Consulting

As the construction equipment sector navigates post-pandemic demand normalization, raw material volatility, and accelerating electrification, PW Consulting’s latest Construction Site Dumper Market report provides an essential strategic compass for executive teams planning capital allocation and product strategy in 2026. This briefing synthesizes the report’s highest-value intelligence — the directional forces, competitive moves, and decision-grade tools — while intentionally reserving granular segment tables and model outputs to incentivize full-report access.

Construction Site Dumper Market

Market trajectory at a glance

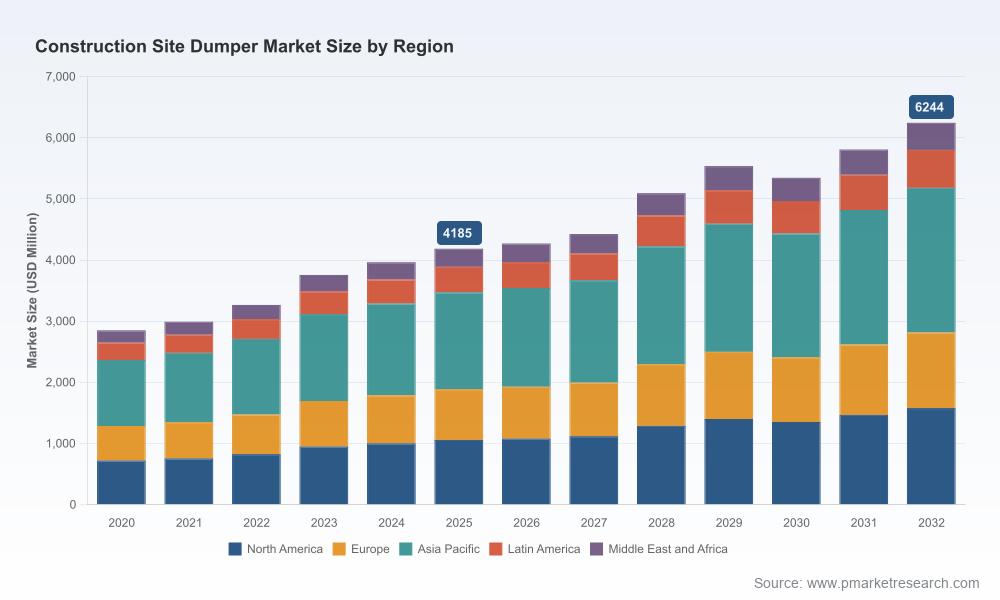

Our baseline analysis shows the global construction site dumper market expanded from a measured base in 2020 through 2025, reaching an estimated USD 4.185 billion in the report’s base year (2025). Under a central-case outlook, the market is expected to grow at a compound annual growth rate (CAGR) of 5.85% through the forecast horizon 2026–2032, reaching approximately USD 6.244 billion by 2032. The near-term (2026–2028) phase is driven by infrastructure stimulus in select markets and fleet renewals targeting site efficiency and operator safety; the medium term reflects wider electrification adoption and productivity-driven replacement cycles.

Construction Site Dumper Market

Why 2026 is a strategic inflection point

- Budget cycles and procurement windows: Many contractors and rental OEMs finalize procurement plans in early 2026, meaning supplier positioning in H1 2026 will materially influence fleet composition over the next 24–36 months.

- Cost inflation convergence: Material cost pressures that fed through 2024–2025 are beginning to normalize, but residual mid-cycle price changes (including a measured 4% increase in mid-sized dumper pricing seen in 2026) will compress low-margin SKUs and reward differentiated value propositions.

- Regulatory and tariff impact: Trade measures on steel and aluminum, and region-specific emissions standards, are concentrating value in localized supply chains and making total cost of ownership (TCO) modeling for global OEMs materially more complex.

Dynamics shaping supplier and buyer strategy

The report highlights four convergent dynamics that executives must internalize to make high-confidence 2026 decisions:

Construction Site Dumper Market

- Electrification and alternative drivetrains: Early commercial electric dumpers and higher-voltage platforms are moving beyond pilot projects, particularly for confined urban sites and municipal fleets. Product portfolios will bifurcate into high-throughput diesel platforms and low-noise, low-emission electric variants.

- Product specialization for site typologies: Urban infill contractors require compact, highly maneuverable units with advanced visibility features; heavy civil and quarry operators emphasize payload productivity and uptime. Manufacturers who can modularize platforms to cover these use cases will capture incremental share.

- Supply-side cost variability: Short-term spikes in steel/aluminum and widening freight/tariff differentials have pushed OEMs to hedge supply and co-locate production closer to demand clusters. Our scenario work shows even small material-cost shocks can alter breakeven points on thin-margin models.

- Channel economics and rental fleet dynamics: Rental houses remain linchpins for adoption; their CAPEX cycles and utilization targets will be decisive in specifying telematics and aftersales terms that OEMs must embed during negotiations.

Competitive landscape — what the major players are doing

The market exhibits moderate concentration: the top three players account for a significant portion of supply, and the top five control a clear majority. This structure favors scale players able to absorb cycle variability while leaving room for specialized manufacturers to win in niche segments.

Key corporate moves we flagged in the fieldwork:

- Thwaites Limited (UK): Thwaites continues to reinforce its manufacturing density with a late-2025 factory extension adding production capacity (~15% uplift). Its product cadence — including larger rotator models and a hi-swivel electric previewed at Bauma 2025 — signals an integrated strategy of volume and technology transition toward electrified mid-duty machines.

- Wacker Neuson (Germany): The launch of the DV125 Dual View model (12.5-tonne payload, 180-degree rotating controls) demonstrates a premium, safety- and visibility-led play targeted at contractors who prioritize operator ergonomics and compact site productivity.

- JCB (UK): JCB’s comprehensive lineup — including continued roll-out of electric 1TE and safety-focused cabins — underscores its twin approach: defend high-volume segments while incubating electrified offerings for urban and rental customers.

- Mecalac (France) and Bergmann Maschinenbau (Germany): Both emphasize compact footprint and niche-site specialization; Mecalac is strong in swivel and front-tip configurations for constrained urban environments, while Bergmann’s tracked and electric variants aim at mixed-terrain and reclamation projects.

- Caterpillar Inc. (USA): Caterpillar’s scale in articulated dump trucks and higher-capacity site dumpers positions it as the go-to for heavy civil and quarry customers that prioritize throughput and integrated dealer support.

Collectively, these moves show a competitive split between scale-driven volume plays and agile, niche-focused innovators. Our benchmarking shows winners will combine product differentiation with localized after-sales networks and data-enabled uptime services.

Practical implications for executives in 2026

PW Consulting’s analysis yields four pragmatic priorities to inform boardroom debates, procurement strategy, and R&D resource allocation:

- Prioritize fleet TCO over sticker price: Given material and tariff-driven cost variability, procurement teams must shift KPIs toward lifecycle cost — factoring in energy, maintenance intervals, residual value, and telematics-driven utilization improvements.

- Segment product roadmaps by site archetype: Firms should explicitly map product families to site archetypes (urban infill, heavy civil, quarry/mining, rental-focused) and avoid one-size-fits-all platforms. Modularity will reduce SKUs and accelerate electrified variants.

- Strengthen local supply and dealer footprints: Expect a premium on locally produced or assembled units in markets with trade frictions. Strategic investments in regional assembly can shorten lead times and insulate ASPs from tariff shocks.

- Embed telematics and service monetization: Fleet operators increasingly value uptime guarantees. OEMs can capture aftermarket margin through subscription telemetry, predictive maintenance, and bundled rental programs.

What PW Consulting’s report delivers — high-value, operational tools

To support the above priorities, the report includes executive-grade deliverables designed for immediate operational use (available in full report):

- Dynamic market-sizing model (2020–2032) with scenario toggles for raw material inflation, electrification uptake, and rental penetration.

- Deal-ready TCO templates that unitize acquisition vs. operating cost under variable energy and maintenance assumptions.

- Competitor benchmarking dashboards covering product portfolios, recent investments, and go-to-market strengths across dealer networks.

- Regulatory and tariff tracker with near-term action items for procurement and supply-chain teams.

- Playbooks for market entry, portfolio rationalization, and M&A screening criteria tuned to CR3/CR5 concentration dynamics.

Note: following the “trailer” principle, the report previews the structure, methodology, and actionable recommendations above while reserving granular regional, type, and application splits in downloadable datasets behind the report portal.

Scenario implications and decision frameworks

We provide three decision frameworks tailored to executive use in 2026:

- Hedged Growth — For OEMs prioritizing market share expansion: focus on flexible SKUs, localized assembly, and rental partnerships to accelerate adoption with controlled capex.

- Margin Protection — For incumbents defending profitability: rationalize low-margin SKUs, index procurement contracts to critical commodity baskets, and upsell aftermarket services to stabilize revenue.

- Technology Leap — For challengers and investors: target compact electrified platforms and telematics-first bundles for fast-adopting urban and municipal segments, using pilot programs to de-risk scale-up investments.

How to use this intelligence in 90 days

- Immediate (0–30 days): Run the TCO templates with your fleet and supplier cost inputs to identify at-risk SKUs and potential immediate procurement renegotiations.

- Short-term (30–90 days): Use our scenario model to stress-test product roadmaps and decide where to accelerate electrified launches or postpone diesel refreshes.

- Quarterly (90+ days): Align dealer incentives and rental-house contracts to secure utilization guarantees that support residual value assumptions for new platforms.

Conclusion — why this report matters for 2026

2026 will be a year where procurement cycles, raw-material normalization, and the operationalization of electrified platforms intersect to reconfigure competitive positions across the construction site dumper market. PW Consulting’s Construction Site Dumper Market report equips leaders with the scenario models, TCO tools, and competitor maps necessary to make informed, defendable decisions — from R&D prioritization and M&A screening to procurement and dealer strategy.

For access to the full dataset, regional and application splits, downloadable models, and an interactive competitor dashboard, please visit the report page. The full report contains the granular segmentation and model outputs that underpin the strategic signals summarized here.

For detailed analysis of this topic, please visit the official page:Construction Site Dumper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com