لماذا يفضل الكثيرون زراعة الشعر في الرياض

Health |

2026-06-24 08:06:03

PW Consulting's latest market research — the Energy Storage Bidirectional AC‑DC Converter Market report (base year 2025, forecast 2026–2032) — is timed to inform a pivotal year for energy storage procurement, project structuring, and industrial strategy. After a period of rapid expansion through 2020–2025, the market reached USD 3,950 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 16.52% across the 2026–2032 forecast window, reaching an estimated USD 11,504.8 Million by 2032. For executives preparing capital allocation, vendor selection, or policy response in 2026, this report synthesizes the evidence, scenarios, and practical tools needed to convert market momentum into defensible outcomes.

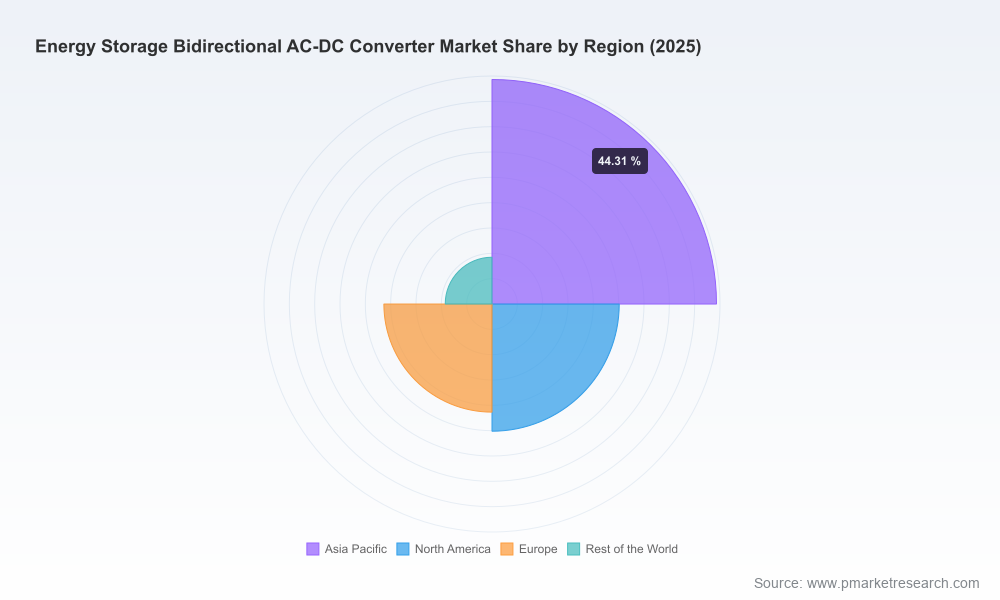

Energy Storage Bidirectional Ac Dc Converter Market

Macro inflection converges with tactical choice: The growth trajectory through 2025 established bidirectional AC‑DC converters as a core enabler for grid flexibility, behind‑the‑meter optimization, EV integration, and microgrid resilience. In 2026, organizations face the first intersection of maturing product portfolios, tightening reliability standards, and new regulatory drivers that together will shape procurement windows and strategic partnerships.

Energy Storage Bidirectional Ac Dc Converter Market

Decision timelines compress: Equipment lead times, interconnection queue dynamics, and incentive program windows mean that decisions made in 2026—on technology architecture, supplier contracting, and warranty structures—will materially influence project returns across the decade.

Energy Storage Bidirectional Ac Dc Converter Market

Risk and opportunity are less symmetrical: Falling cell costs and more predictable LFP supply reduce system-level price risk, while regulatory updates and rising operational requirements increase supplier and controls risk. The report quantifies these shifts and translates them into procurement and design imperatives.

Market-sizing and scenario modeling: A clear baseline anchored to 2025 market scale and a set of 2026–2032 demand scenarios driven by policy adoption, utility procurement, EV penetration, and grid reliability interventions. Each scenario maps sensitivity to capital cost declines and regulatory shifts.

Technology and architecture playbooks: Comparison of converter topologies, cooling approaches, and control strategies with guidance on selecting architectures for utility-scale, commercial & industrial, and residential use cases. The analysis highlights tradeoffs in efficiency, modularity, power density, and integration complexity.

Supplier scorecards and procurement templates: Due‑diligence checklists, warranty and service‑level clauses, performance testing protocols, and an objective scoring framework to evaluate vendors on product maturity, manufacturing footprint, software controls, and lifecycle O&M costs.

TCO and revenue-stack models: Region‑agnostic total cost of ownership templates and monetization pathways (capacity services, energy arbitrage, ancillary markets, V2G) with configurable inputs to test project-level IRR across contract and regulatory permutations.

Regulatory impact matrix: A concise tool mapping major regulatory actions (building codes, grid reliability orders, carbon border adjustments) to procurement, compliance cost, and market access effects for converters and integrated BESS projects.

Integration and deployment playbooks: Best practices for control integration, cybersecurity hardening, factory acceptance testing (FAT), and site commissioning that lower soft‑cost risk and accelerate commercial operations.

The competitive set is heterogeneous: vertically integrated multinationals, regional power‑electronics specialists, and fast‑moving OEMs from Asia and Europe. Market concentration is moderate: the top three suppliers account for roughly 38.5% of market revenue, and the top five about 55.2%, underscoring competitive pockets alongside meaningful global players.

Honle Group (Germany, with China operations): Known for three‑level topologies in its HPCS series, Honle emphasizes high conversion efficiency (>98.5%), modular scaling, and hybrid microgrid capabilities. Their portfolio is relevant where high efficiency and UPS functionality are contractually required.

Infypower (China): Focused on high power density modules for C&I and industrial ESS, including offerings tailored for V2G and both isolated/non‑isolated DCDC variants. Their strengths are compact designs and application-specific power electronics expertise.

Shenzhen UUGreenPower (China): Blends residential ESS and V2G solutions, integrating bidirectional AC‑DC technology into charging and home energy management systems. They are a notable option for integrators pursuing combined EV and behind‑the‑meter strategies.

Shenzhen Acadie New Energy (China): Active in export markets with modular PCS and converters across a range of power ratings, including ruggedized units for mixed on‑grid/off‑grid deployments and battery test integration — a pragmatic choice for system integrators seeking flexibility.

Epic Power Converters (Spain): Specializes in bidirectional DC‑DC and hybridization solutions for energy recovery, supercapacitor pairing, and microgrid edge applications; differentiated where hybrid energy storage architectures are in play.

ABB (Switzerland): Offers broad-spectrum PCS and high‑power solutions for utility and traction markets; a strategic vendor where established grid‑scale control interfaces, project delivery capability, and long‑term service are procurement priorities.

Delta Electronics (Taiwan): Competes on modular PCS architectures for grid‑tied and C&I segments, with a strong history in scalable power electronics and energy management systems.

Sungrow (China): Focused on utility‑scale systems with liquid‑cooled string PCS and high efficiency; appeals to large BESS projects where deployed thermal management and reliable grid‑tie performance are key.

Product introductions have continued into 2026, with firms launching higher‑efficiency and application‑specific converters tailored to both on‑grid and off‑grid use.

Large project awards and commissioning activity (including extra‑high‑voltage and multi‑MW installations) show system integrators and utilities accelerating deployment of bidirectional assets for grid services and capacity deferral.

Policy updates—especially building codes and executive orders focused on grid reliability—are shifting technical requirements and certification expectations for converters used in both new construction and grid‑support projects.

Falling battery costs and LFP availability: Recent market evidence points to materially lower cell prices for stationary applications, which reduces the battery share of total project capex and increases the relative importance of power electronics and controls as differentiators.

Regulatory tightening on grid impacts: National and subnational measures to address intermittency and system stability are raising technical bar for converter behavior, testing, and reporting; procurement specifications must align to evolving reliability standards.

Supply chain and carbon policy: Emerging carbon‑content and border measures will increasingly influence sourcing decisions for power electronics components, and buyers should factor in compliance costs and supplier traceability.

Prioritize supplier evaluation against system‑level value, not just price: Use the report’s TCO and performance modeling to stress‑test bids under realistic revenue stacks and regulatory scenarios.

Lock down interoperability and testing protocols early: Insist on standardized FAT and interoperability acceptance criteria to avoid integration rework during commissioning windows.

Design for optionality: Select converter architectures and contract terms that preserve flexibility for upgrades, secondary markets, and lifecycle services as business models for storage evolve.

Embed regulatory watch into procurement: The report’s regulatory impact tools help align contract warranties and operational assumptions to new code and market requirements expected to influence deployments in 2026 and beyond.

PW Consulting’s Energy Storage Bidirectional AC‑DC Converter Market report combines a structured market‑sizing framework (historical 2020–2025 baseline, 2026–2032 forecasts), supplier profiling, product benchmarking, and transaction‑oriented tools. The report is designed for energy buyers, project developers, equipment OEMs, utilities, and policy teams who need to translate macro growth—reflected in a projected CAGR of 16.52%—into executable 12–36 month plans.

Note: This release intentionally highlights strategic findings and the report’s practical outputs while preserving the detailed regional and application segmentation inside the full report. For the complete dataset, regional and application splits, company scorecards, and downloadable procurement templates, visit our report page to access the full research package and enterprise licensing options.

For detailed analysis of this topic, please visit the official page:Energy Storage Bidirectional Ac Dc Converter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com