Seaweed-Based Packaging Market: Strategic Insights for 2026 — A PW Consulting Preview

Executive summary

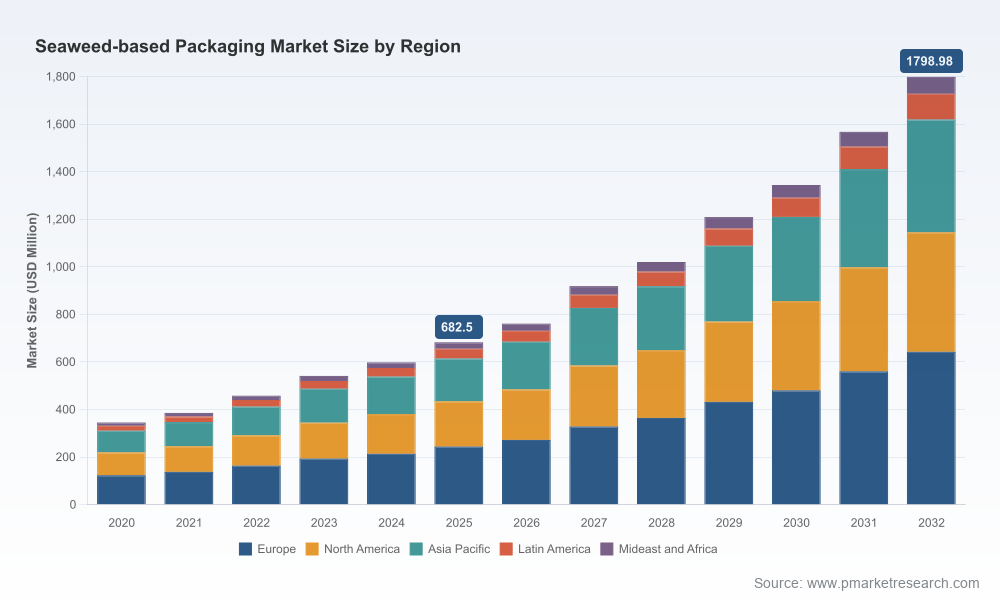

As pressure intensifies on brands to eliminate persistent plastics and meet evolving regulatory thresholds, seaweed-based packaging has transitioned from niche innovation to a strategic option for risk-averse and sustainability-forward companies. Our latest market study — with a 2025 base year and a 2026–2032 forecast horizon — shows the market crossing the USD 682.5 Million threshold in 2025 and accelerating toward nearly USD 1.8 Billion by 2032, driven by a 14.85% CAGR across the forecasting period. These headline dynamics are only the starting point. This release highlights the operational insights and decision frameworks in the full PW Consulting report that will matter most to executives allocating 2026 budgets for procurement, manufacturing, and product portfolios.

Seaweed Based Packaging Market

Why 2026 is a strategic inflection point

Three converging forces make 2026 decisive: regulatory tightening around legacy chemistries, raw-material price signals, and a maturation of near-commercial technologies. Notably, legislative moves in the EU and several high-profile packaging EPR regimes will reprice non-recyclable and PFAS-containing materials starting mid-2026. At the same time, inputs such as sodium alginate and carrageenan are exhibiting price volatility that creates both margin pressure and opportunity for vertically integrated players. Collectively, these forces shift the optimization problem companies face—from purely unit-cost substitution to a multi-dimensional tradeoff across compliance, supply security, performance, and circularity claims.

Seaweed Based Packaging Market

Market trajectory in one glance

- The seaweed-based packaging market scaled rapidly during 2020–2025 and is forecast to continue growing at a high-teens compound annual growth rate through 2032 (14.85% CAGR in the 2026–2032 forecast window).

- Growth is being driven by both single-use replacement opportunities in flexible films and emerging demand for home-compostable rigid items and coatings that enable paper recycling compatibility.

- Despite momentum, the competitive landscape remains fragmented: the three largest firms account for under one-fifth of global revenues (CR3 ≈ 18.4%), and the top five firms capture less than a third (CR5 ≈ 28.6%). This fragmentation creates acquisition and roll-up opportunities for strategic and financial buyers seeking scale and technology portfolios.

Key dynamics reshaping decisions in 2026

- Regulatory acceleration: The EU’s packaging rules banning PFAS above defined thresholds from August 2026, as well as forthcoming recyclability-adjusted EPR fees in the UK and expanding US state EPR programs, will materially change total cost of ownership calculations for consumer-facing brands. Seaweed-based alternatives, which are inherently PFAS-free, will be prioritized where chemical compliance risk is high.

- Raw-material economics and supply risk: Prices for sodium alginate and refined carrageenan have exhibited sharp regional divergence and tightening due to constrained seaweed harvests and processing capacity. This volatility favors offtake agreements, vertical integration, and alternative formulation strategies that reduce dependence on a single polymer.

- Scale and manufacturing compatibility: The most investable technologies are those offering retrofit compatibility with existing film- and thermoforming lines. Suppliers able to supply bio-resins and film structures that integrate into existing converters lower adoption friction and shorten payback horizons.

- Performance expectations: Barrier properties (water, oxygen, grease), mechanical robustness, and recyclability or compostability certifications are the non-negotiables for CPG buyers. Adoption requires validated third-party testing and pilot data across SKU profiles.

Competitive landscape: what the leading innovators signal

The market’s profile is defined by a mix of deep-technology start-ups, regionally focused manufacturers, and a handful of scaling platform plays. The companies profiled in our report illustrate differentiated strategic routes to market:

Seaweed Based Packaging Market

- Notpla Limited (London): Focused on event- and foodservice-grade coated containers, rigid utensils, and liquid pods, Notpla’s recent Horizon Europe award underscores the importance of consortium models for shared R&D and accelerated commercialization in Europe. Their emphasis on home-compostability and ingredient simplification makes them well-positioned against PFAS restrictions.

- Sway Innovation Co. (California): Sway’s strategy to deliver thermo-plastic resins and flexible films compatible with existing film-manufacturing lines addresses a major buyer pain point: capital avoidance. Strategic wins with fashion and retail brands demonstrate cross-category applicability beyond food.

- Evoware (Indonesia) and LOLIWARE (US): These players focus on edible and sachet-form products, tapping into foodservice and single-portion applications. Their routes to scale hinge on food-contact certification and supply chain partnerships in high-volume categories such as instant noodles and on-the-go beverages.

- B'ZEOS, Zerocircle, FlexSea, Kelpi, Uluu, PlantSea: These firms represent a spectrum from coating specialists to industrial-scale bioplastic manufacturers. Recent funding rounds and facility-scale announcements signal that capital markets view production scale as the next critical battleground.

Recent corporate milestones tracked by PW Consulting are illustrative: late-2025 and early-2026 funding and program launches (including significant Series A and Horizon grants) confirm investor appetite for capacity-build and consortium-based commercialization. These developments materially improve the supply outlook but also intensify competition for feedstock and skilled talent.

What the PW Consulting report delivers — practical, transaction-ready intelligence

Our full report is structured to support procurement decisions, commercial pilots, and M&A diligence across 2026. It includes:

- Actionable go-to-market playbooks for CPG, retail, and foodservice buyers that map decision trees for pilot, scale, and substitution across packaging types.

- Supply-chain risk matrices and procurement levers — including scenario analysis for alginate/carrageenan price shocks, logistics disruptions, and regulatory pivots.

- Techno-economic models and investment calculators tailored to retrofit conversions vs. greenfield lines, with sensitivity testing on raw-material pricing, throughput, and yield improvements.

- Supplier scorecards and procurement templates to standardize RFPs, verification checkpoints, and commercial terms for offtake and joint-development agreements.

- Commercial adoption scenarios and SKU-level migration roadmaps that show phasing from pilot to full roll-out without revealing proprietary segmentation-level revenue shares (those granular tables are reserved for report access).

- Regulatory impact analysis and compliance checklists tied to 2026 rule changes, including PFAS restrictions and EPR fee modulation frameworks.

Strategic recommendations for 2026 decision-makers

- Prioritize pilot-to-scale projects that reduce capital friction. Favor solutions that are compatible with existing converting equipment or that include commercial partners willing to underwrite co-investment in retrofits.

- Lock in feedstock risk mitigation now. Negotiate multi-year offtake or joint-venture frameworks with upstream seaweed processors, or structure price collars to protect margins against alginate and carrageenan volatility.

- Use procurement levers to drive supplier maturity. Shift to milestone-based supplier agreements that condition volume commitments on validated barrier performance and compostability/recyclability certifications.

- Monitor regulatory timing and embed compliance triggers. Model the immediate and delayed impacts of EU PFAS limits and EPR banding into price-to-market scenarios; re-evaluate SKU prioritization where EPR fees materially alter economics.

- Treat capability as M&A-ready. Given low market concentration and multiple early-stage players securing funding, build an M&A watchlist for bolt-on technologies that add either feedstock control, barrier performance, or scalable film production.

How PW Consulting’s intelligence reduces execution risk

Transitioning to seaweed-based packaging presents novel technical and commercial risks. The full report de-risks decision-making by combining primary interviews, pilot test data, proprietary supply-cost models, and regulatory timelines into a single executable narrative. We provide prioritization matrices that show which SKUs to convert in Year 1 vs. Years 2–3, the minimum certification thresholds buyers should demand, and a list of potential industrial partners that can absorb scale-up risk.

Conclusion — the 2026 mandate

For corporate leaders, 2026 will not be a year of benign experimentation — it will be a year of irreversible sourcing and compliance commitments. Seaweed-based packaging is moving from an R&D curiosity to a mainstream substitution lever for companies that need to demonstrate rapid compliance and credible sustainability claims. With strong headline growth and continued fragmentation, the market offers both first-mover advantages and consolidation opportunities. Our PW Consulting report translates this complexity into prescriptive actions: what to pilot, who to partner with, and how to secure supply at competitive economics.

Next steps

PW Consulting’s full Seaweed-Based Packaging Market report contains the granular supplier matrices, SKU migration models, and transaction-ready annexes that executives will require to make confident 2026 decisions. Access to the complete dataset and the implementation playbooks is available through PW Consulting’s report page and client services team — contact us to schedule an executive briefing and to receive the proprietary annex that supports procurement and M&A actions.

For detailed analysis of this topic, please visit the official page:Seaweed Based Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com