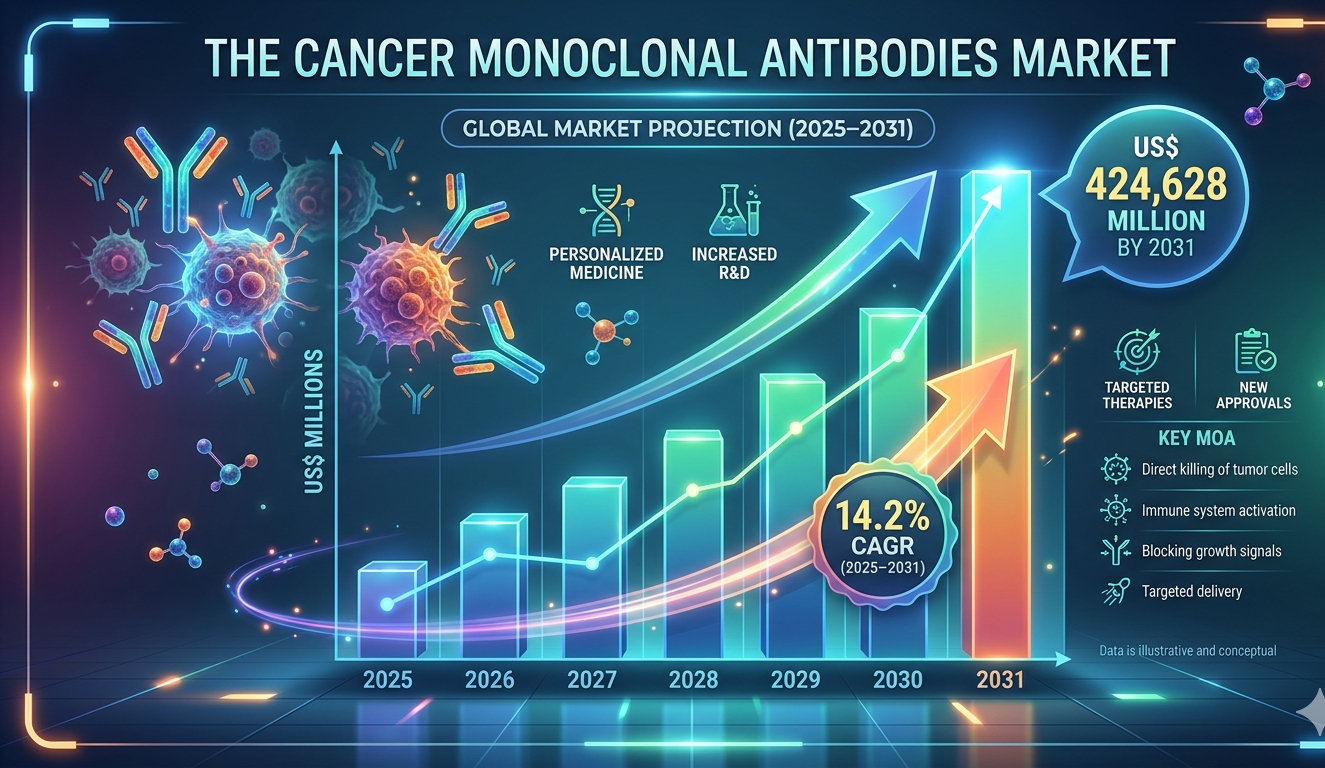

Cancer Monoclonal Antibodies Market: Growth Drivers and Challenges Ahead of 2031

Other |

2026-05-11 15:44:40

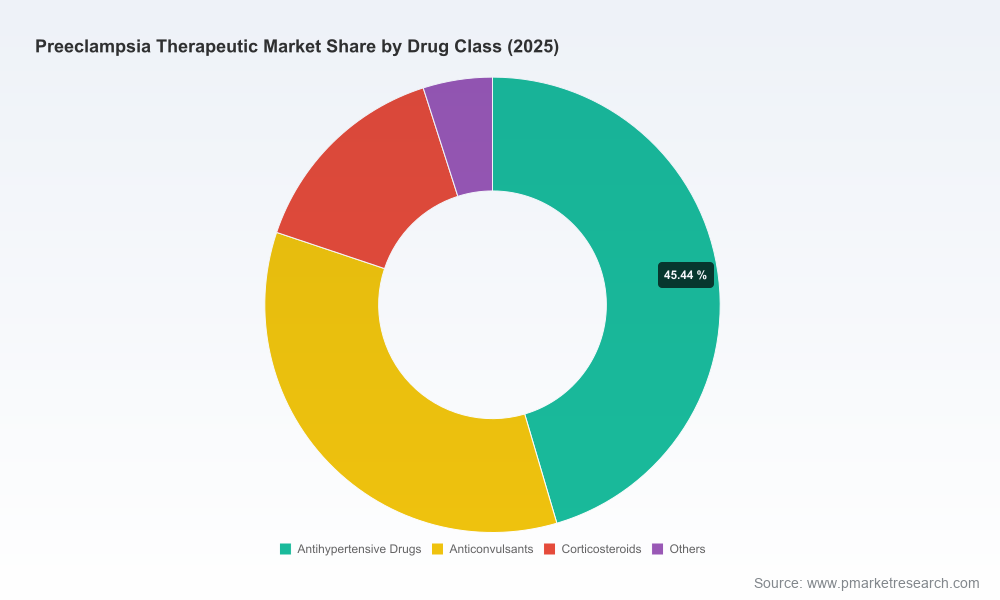

PW Consulting’s new market research release on the Preeclampsia Therapeutic Market provides an actionable, decision-focused roadmap for life sciences executives, investors, and health-system strategists preparing for the 2026 strategic cycle. Anchored on a 2025 base year and a 2026–2032 forecast window, the study models market dynamics under clinical, regulatory, supply-chain and reimbursement scenarios and identifies the inflection points that will determine commercial winners. At a glance, the market is on a steady growth trajectory (CAGR 4.88% over the forecast period), building from a 2025 baseline of approximately USD 1.29 billion to a projected market in the vicinity of USD 1.80 billion by 2032.

Preeclampsia Therapeutic Market

Timing for clinical and regulatory catalysts is compressed. A handful of late-stage programs and platform technologies are positioned to enter pivotal human data windows in 2026–2027, making near-term prioritization critical for licensing, partnering, and capital allocation.

Preeclampsia Therapeutic Market

Market structure favours mid-concentration dynamics: incumbents and well-funded speciality developers collectively command a material share of market influence (CR3 ~41%, CR5 ~57%), but commercial fragmentation persists across modalities and care pathways.

Preeclampsia Therapeutic Market

Clinical and diagnostic convergence is accelerating: advances in predictive testing and targeted interventions could shift spend toward earlier intervention and hospital-delivered therapeutics, altering channel dynamics and payer conversations.

Operational risk is asymmetric. Supply-chain weaknesses in low- and middle-income settings remain a structural constraint for acute-management medicines and could materially affect access strategies and philanthropic models.

Portfolio prioritization: Use a two-stage filter that combines reproductive‑safety-adjusted probability of technical success with commercial defensibility. In preeclampsia, safety in pregnancy and demonstrable maternal/fetal benefit are non‑fungible—programs lacking robust maternal-fetal safety de‑risking should be deprioritised or paired with stronger development partners.

Regulatory sequencing: Engage early with major regulators (FDA, Health Canada, EMA, and national agencies in target expansion markets). Recent productive pre‑IND interactions and country‑level trial clearances illustrate that regulatory playbooks in this field are both bespoke and decisive.

Clinical trial strategy: Secure high‑quality obstetrics trial sites and build centralized safety monitoring. Recruitment timelines will be the gating item for 2026 launches; partnerships with academic centers and foundations can materially reduce time‑to‑first‑in‑human and enrollment risk.

Commercial and diagnostic linkage: Prepare reimbursement dossiers that integrate diagnostic stratification with therapeutic value. Point‑of‑care and laboratory sFlt‑1/PlGF ratio testing, for example, will shape how payers and health systems perceive value; separate selling and bundled pathways should be modelled.

Manufacturing and supply resilience: For developers and suppliers of repurposed supportive medicines, invest in multi‑sourcing and regional buffer strategies to mitigate episodic stock‑outs in constrained markets.

The competitive landscape is composed of modality‑diverse players (biologics, oligonucleotide/siRNA approaches, small molecules, and device/apheresis platforms). Clinical trajectories and regulatory footprints differ materially across companies; a selective view of key strategic actors and their near‑term catalysts is summarized below to illustrate the strategic choices facing buyers, partners, and investors.

DiaMedica Therapeutics (Minneapolis, MN; https://www.diamedica.com) — Advancing DM199 (rinvecalinase alfa), a recombinant tissue kallikrein‑1 candidate for early‑onset preeclampsia. Notable 2025–2026 milestones include a productive pre‑IND meeting with the FDA (additional non‑clinical data requested; results expected Q2 2026) and Health Canada clearance for a Phase 2 study with recruitment anticipated in 2026. Strategic implication: DiaMedica’s regulatory progress makes it a near‑term partner or acquisition candidate for organizations seeking an advanced biologic with a defined regulatory path.

Comanche Biopharma (USA) — Developing CBP‑4888, an siRNA targeting sFLT1 isoforms. RNAi programs bring distinct delivery and durability trade‑offs in pregnancy; success requires integrated maternal‑fetal toxicology packages and delivery platforms tuned to obstetric physiology.

Gmax Biopharm (China/USA) and Vicore Pharma (Sweden) — Companies advancing novel candidates that target disease mechanisms rather than symptomatic control, representing strategic options for partners seeking mechanism‑led portfolios.

Kyowa Kirin (Tokyo; https://www.kyowakirin.com) — A major player with therapeutic candidates under evaluation and global development capabilities; potential strategic acquirer or late‑stage partner for emerging innovators.

Evergreen Therapeutics (USA) and MirZyme Therapeutics (UK) — Early‑stage small molecule and prevention candidates; these programs are attractive to investors with longer horizons and to acquirers seeking prevention‑focused assets.

Advanced Prenatal Therapeutics (USA; https://www.advancedprenatal.com) and Aggamin LLC (USA) — Device/apheresis and recombinant protein approaches respectively; they emphasize the breadth of intervention types and the need for multi‑modality commercial strategies.

Recent non‑company developments provide additional context: Trinity Biotech secured regulatory clearance to provide an FDA‑cleared sFlt‑1/PlGF ratio test in New York State in 2025, and academic centers (e.g., Medical College of Wisconsin) are launching vascular‑function trials supported by philanthropic funding. These events accelerate the diagnostic‑therapeutic nexus and create earlier pathways for real‑world evidence generation.

Market sizing and scenario‑based forecasting (2020–2032), including base, upside and downside scenarios driven by regulatory approvals, reimbursement timing and access constraints.

Clinical pipeline map with program‑level profiles: mechanism of action, development stage, regulatory status, likelihood‑of‑success scoring adjusted for maternal‑fetal safety considerations.

Regulatory playbooks for the US, Canada, EU and selected emerging markets: recommended pre‑IND/IMPACT meeting topics, endpoints accepted by regulators, and safety packages necessary for pregnancy indications.

Commercial playbooks: go‑to‑market segmentation, payer engagement templates, diagnostic linkage models, and hospital channel strategies.

Operational risk matrices: manufacturing scale‑up checklists, supply‑chain mitigation plans for essential medicines, and quality governance for pregnancy‑exposed products.

BD&L and M&A screening tools: target scoring templates, valuation sensitivities, and integration checklists tailored to preeclampsia assets.

Primary research appendix: executive interviews, clinical opinion leader survey results, and anonymised payer interview excerpts to support pricing and access assumptions.

Note: this press summary deliberately omits detailed regional and segment line‑item splits. The full report provides granular segmentation by region, drug class and distribution channels, along with downloadable tables and appendices for transaction diligence.

Investment committees: use our probability‑weighted scenario outputs to stress‑test valuations and inform tranche‑based investments tied to clinical milestones and regulatory readouts.

BD&L teams: prioritize programs that demonstrate both reproductive safety and scalable delivery. Shortlist candidates for exclusive option rights before pivotal dat a readouts widen competition.

Commercial teams: align early with diagnostics providers and hospital systems to co‑design pilots that can be converted into reimbursement pathways upon positive clinical evidence.

Manufacturing and supply leaders: incorporate redundant sourcing and regional buffer inventories for supportive medicines to maintain credibility in LMIC access programs and to avoid disruptions in trial supply.

Key near‑term milestones to watch include regulatory and clinical activity expected in 2026 (e.g., requested non‑clinical study completions, Phase 2 recruitment starts, and diagnostic rollouts). These events will materially re‑shape investor sentiment and create actionable windows for partnerships and M&A. For teams setting 2026 budgets and strategic plans, the next 90–180 days are decisive: align clinical, regulatory and commercial timelines now to avoid reactive, higher‑cost moves later in the cycle.

PW Consulting’s Preeclampsia Therapeutic Market report is designed as the operational intelligence layer that turns market forecasts into executable plans. For full access to the granular segmentation tables, pipeline dossiers, valuation models and downloadable diligence templates, visit the Preeclampsia report page on the PW Consulting portal or contact your PW Consulting account lead for an executive briefing.

For detailed analysis of this topic, please visit the official page:Preeclampsia Therapeutic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com