What are the different types of acne?

Health |

2026-06-24 10:29:41

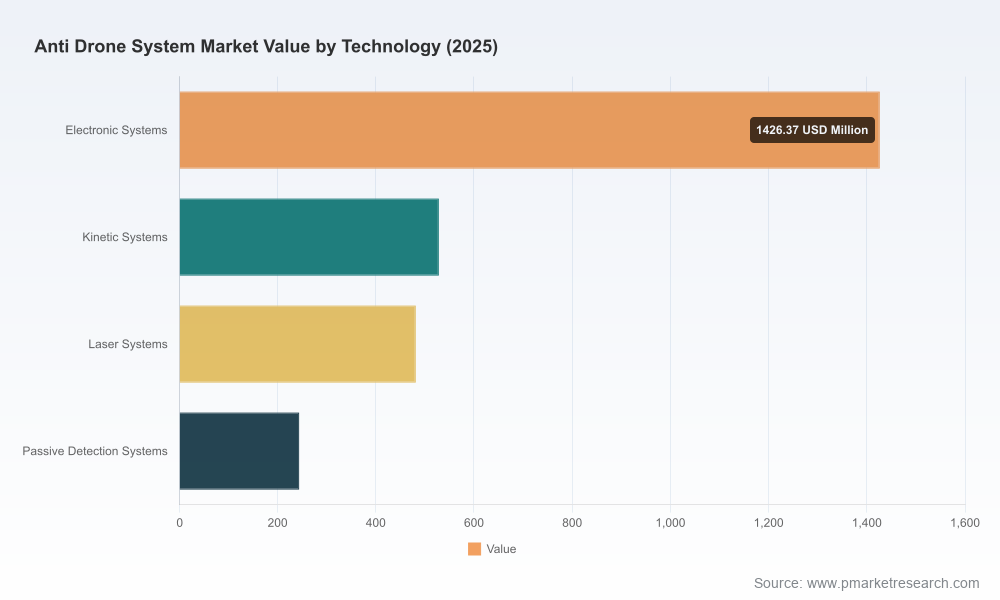

PW Consulting’s new market study on Anti-Drone Systems positions 2026 as an inflection year for both procurement and technology strategy. Using 2025 as the base year, our analysis finds the market expanding at a compound annual growth rate (CAGR) of 26.35% across the 2026–2032 forecast window. Measured in USD (Millions), the global market more than quadruples from the 2025 baseline over the forecast period, reflecting a rapid transition from ad hoc mitigation to institutionalized airspace security programs. For executive teams charged with budgeting, procurement, technology roadmaps, or M&A strategy in 2026, this report provides the strategic lenses and operational playbooks required to convert opportunity into sustainable capability.

Anti Drone System Market

Regulatory tightening is accelerating procurement timelines. Recent FAA enforcement updates and expanded counter‑UAS authorities in national defence budgets have increased both the risks of non-compliance and the urgency to field effective countermeasures.

Anti Drone System Market

Institutional testing and validation are moving from pilot projects to standardized evaluation. NATO’s new Innovation Range and Joint Interagency Task Force guidance on testing and privacy create a de facto playbook for interoperable, certifiable solutions.

Anti Drone System Market

Procurement programs are scaling. Dedicated offices and program-level funding streams — illustrated by recent government investments targeted at high-profile events and force protection needs — are shifting spend from tactical buys to multi-year, systems-of-systems contracts.

The anti‑drone market is being reshaped by four mutually reinforcing forces: rising operational threats, regulatory and standards momentum, rapid technology maturation, and a changing procurement landscape. Adversary adoption of inexpensive, swarm‑capable platforms has elevated mission risk across theaters from urban events to forward operating bases. In parallel, regulators and defense authorities are clarifying the legal and technical boundaries for detection, interception, and privacy protection. These dynamics are tightening requirements for demonstrable performance against defined scenarios — an evolution that favours vendors able to deliver integrated, testable, and legally compliant solutions.

Layered architectures dominate procurement thinking: persistent detection (radar, passive sensors, RF), classification (EO/IR, sensor fusion, AI), and modular defeat options (electronic warfare, non‑kinetic RF/cyber takeover, kinetic, and directed energy) are now expected elements of a defensible capability.

AI and autonomy are rapidly moving from analytics to operational control. Autonomous C2 platforms and automated cueing materially reduce human-in-the-loop burdens but raise questions about certification and rules-of-engagement.

Interoperability and open architectures are procurement differentiators. Systems that can integrate with existing air-defence networks and C2 infrastructures accelerate fielding and reduce lifecycle friction.

The market exhibits a mix of prime defense contractors, specialized niche players, and venture-backed innovators. Market concentration metrics indicate that the top vendors hold meaningful share collectively, while a broad long tail of companies continues to innovate in sensor fusion, RF countermeasures, and autonomous defeat tools. Recent large contracts and financing events illustrate this dynamic: prime contractors are securing system-level awards that bundle radar and effector capabilities, while well‑funded startups are pushing the sensing and AI frontier.

Prime systems integrators (examples): Established defense primes continue to win large integrative contracts by leveraging proven radar, EW and directed-energy platforms and by offering lifecycle services and supply-chain scale. These firms are strategic partners for national programs and institutional customers seeking turnkey, certifiable solutions.

Specialists and innovators (examples): Small and mid-size companies are differentiating through RF-centric detection, AI-driven C2, and novel defeat options such as autonomous capture. Their agility and technology depth make them attractive partners for capability augmentation or bolt-on acquisitions.

Market signals: Large prime awards and significant private funding rounds alike underscore a bifurcated market: incumbents capture system-level, long‑term spend while agile innovators drive technology shifts and create acquisition opportunities for strategic buyers.

We designed the study to be an operational tool for decision-makers, not just an academic forecast. Key modules include:

Strategic decision frameworks for capability prioritization across operational theatres and risk profiles.

Procurement playbooks: RFP templates, test & evaluation criteria, interoperability checklists, and scoring matrices aligned with current regulatory guidance.

Vendor assessment and scoring methodology that blends technical performance, integration risk, sustainment economics, and compliance posture.

Total cost of ownership (TCO) models and scenario-based budget simulations tailored to different acquisition pathways (rapid procurement, phased modernization, or CAPEX investment).

Operational case studies illustrating successful deployments, failure modes, and mitigation strategies learned from recent real-world incidents and government testing programs.

M&A and partnership playbooks identifying capability gaps and acquisition targets to accelerate in‑house competence.

Adopt a layered, risk‑based procurement strategy: specify detection, classification, and defeat as separable, tested modules within a system-of-systems contract to avoid vendor lock and to enable incremental capability upgrades.

Prioritize interoperability and open standards in procurement language to ensure long-term integration with national airspace management and defense C2 systems.

Fund rigorous testing and validation early: allocate budget for compliance testing against national test ranges and independent verification to accelerate certification timelines.

Hedge technology risk with dual‑track sourcing: pair prime integrators for scale with specialist vendors for rapid innovation, especially in AI, RF sensing, and directed energy.

Embed privacy and legal compliance into procurement requirements to mitigate program delay and litigation risk as regulatory frameworks tighten.

Explore strategic partnerships or targeted acquisitions to acquire niche capabilities (autonomous C2, RF-cyber takeover, or advanced sensors) that are costly to develop in-house.

Investors should view the market as a rapid-growth sector with differentiated risk: prime contractors offer exposure to large, stable contracts and lifecycle services, while venture-backed firms present high upside tied to technology adoption or strategic buyouts. Buyers within government and critical infrastructure must balance speed-to-field with long-term sustainment and legal/regulatory compliance. The report’s TCO and scenario modules help translate growth forecasts into defensible budget requests and procurement timelines for 2026–2027 cycles.

Our study combines a forward-looking market forecast with operationally focused deliverables — from procurement templates to vendor scorecards — that executives can apply directly in 2026. The market’s 26.35% CAGR and the rapid expansion projected over the forecast period create both urgency and opportunity. Whether you are executing a rapid fielding for a high‑profile event, modernizing force protection, or assessing strategic investments, this research provides the evidence-based roadmaps and implementation checklists required to reduce program risk and accelerate capability delivery.

PW Consulting encourages decision-makers to use the report as the basis for their 2026 counter‑UAS strategy workshop. The full dataset, vendor scorecards, procurement templates and scenario financials are available in the complete report and accompanying analyst briefings. Contact PW Consulting to schedule a tailored briefing that aligns the report’s insights to your organization’s risk profile and operational requirements.

For detailed analysis of this topic, please visit the official page:Anti Drone System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com