PW Consulting: Strategic Brief — 2,2‑Dimethylbutyric Acid Market Insight for 2026 Decision‑Makers

As industrial chemistry and specialty intermediates converge with shifting global trade dynamics, 2,2‑Dimethylbutyric Acid (DMBA) is transitioning from a niche building block to a strategically important component across pharmaceuticals, agrochemicals and specialty chemical formulations. PW Consulting’s latest market study — covering historical performance from 2020–2025 and a forward forecast through 2026–2032 — is designed to translate the market’s quantitative trajectory into actionable decisions for 2026 planning cycles.

22 Dimethylbutyric Acid Market

Market trajectory at a glance

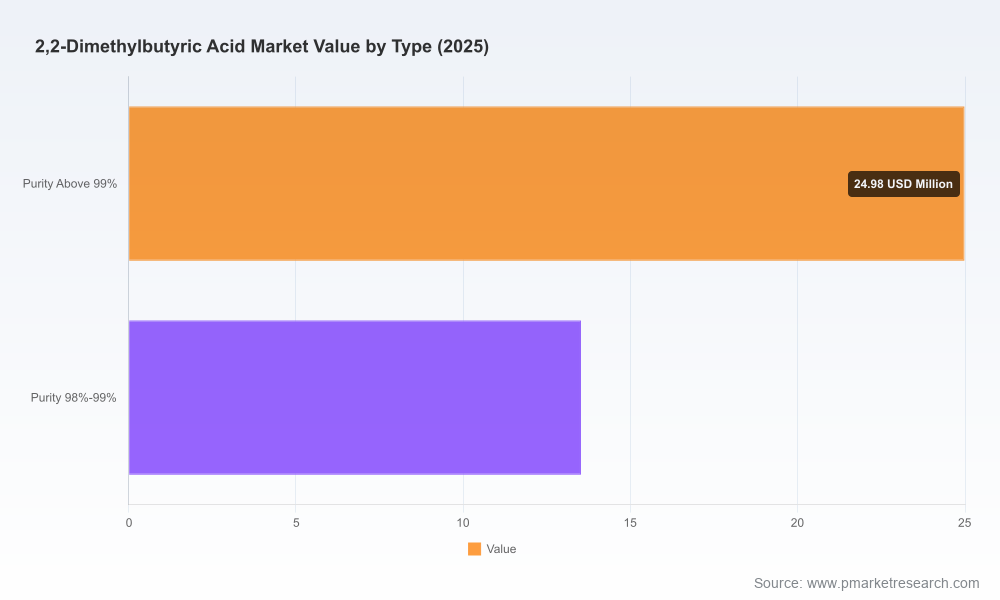

Between 2020 and 2025 the global DMBA market exhibited steady expansion, rising from USD 30.45 million in 2020 to USD 38.5 million in 2025. Our base‑year analysis (2025) and scenario modeling project continued growth through 2032, with the market approaching an estimated USD 53.52 million by 2032. The compound annual growth rate (CAGR) underpinning our central forecast is 4.82% for the 2026–2032 horizon. Market concentration indicates meaningful incumbent strength: the top three firms account for a majority share, and the top five reach a high concentration level — a structural feature buyers and investors must factor into strategic planning.

22 Dimethylbutyric Acid Market

Why this report matters for 2026 strategy

- Timing: 2026 will be a pivot year for procurement and capacity decisions — supply visibility from the back‑end of 2025 is insufficient for multiyear contracts and CAPEX planning. Our report converts recent historical trends into supply‑side and demand‑side scenarios that are tailored to typical 18–36 month decision cycles.

- Risk management: Rising regulatory scrutiny on classifications, customs regimes and inspection requirements is changing cross‑border transaction economics. Tactical adjustments in sourcing, contractual terms and logistics can materially alter landing costs in 2026.

- Competitive positioning: Concentration metrics and supplier capabilities create windows for both consolidation plays and targeted supplier development. Buyers can secure preferential terms by moving earlier in the sourcing cycle; investors can identify attractive roll‑up targets with near‑term margin improvement potential.

What the PW Consulting report delivers — a practical, decision‑ready toolkit

Our objective is to arm procurement leaders, R&D heads, business development teams and corporate strategists with pragmatic intelligence that supports executable decisions in 2026. The study includes:

22 Dimethylbutyric Acid Market

- Market sizing and validated demand forecasts (2020–2032) with scenario analysis (baseline, upside, downside) and sensitivity testing against feedstock price shocks and regulatory shifts.

- Supply‑side mapping: vetted supplier database, capacity estimates, and production footprints with an emphasis on scale, quality certifications, and export capability.

- Cost‑curve construction and landed cost models incorporating feedstock inputs, typical process yields and purification overheads — enabling negotiation of forward‑looking offtake agreements.

- Patent and process landscape: comparative review of documented synthesis routes, technical bottlenecks, and patent expiry timelines that affect manufacturing economics and potential process licensing.

- Regulatory and trade matrix: HTS classification impacts, tariff profiles, licensing and inspection regimes, and compliance checklists for major export/import flows.

- Supplier scorecards and a procurement playbook: quality, capacity, transport reliability, certification status, and sample contracting language for risk allocation.

- Strategic options and investment returns: M&A screening criteria, greenfield vs brownfield CAPEX sizing, and scenario IRR models for expansion or backward integration.

- Technical annexes: standard specifications, SDS comparisons, recommended analytical methods and a reproducible due‑diligence checklist.

Competitive landscape: selective company analysis and implications

The DMBA market displays a moderate to high level of concentration. In our assessment, three firms exert outsized influence on supply dynamics, while the top five substantially shape pricing and quality benchmarks. Below we provide a concise, actionable snapshot of selected industry participants and the strategic signals they send to market actors.

- TNJ Chemical (China) — TNJ positions itself as a certified manufacturer and supplier with a 99% minimum assay product offered as an intermediate in standard industrial packaging. The company’s combination of export capability and third‑party certifications makes it a default counterparty for buyers requiring scale and documented quality compliance. Strategic takeaway: buyers seeking integrated supplier audits and routine volume should prioritize advance qualification agreements with TNJ.

- OTTO KEMI (India) — Focused on puriss‑grade material and global shipments, OTTO KEMI is an agile supplier capable of supporting shorter lead‑time, research and development requirements. Strategic takeaway: pharmaceutical R&D teams and specialty formulators can leverage suppliers like OTTO KEMI for experimentation and small‑volume continuity while negotiating pathway to scale.

- Central Drug House (CDH) Fine Chemicals (New Delhi) — As an ISO certified manufacturer offering analytical reagent grades, CDH is oriented toward quality assurance and smaller pack sizes suitable for laboratories and formulation testing. Strategic takeaway: for firms requiring consistent analytical standards across regulatory jurisdictions, CDH’s ISO pathway reduces validation burden.

- Tokyo Chemical Industry (TCI) (Japan) — TCI’s role as a lab and building‑block supplier, with detailed specifications and safety documentation, supports customers that prioritize traceability and robust SDS materials for regulated R&D environments. Strategic takeaway: premium documentation and batch traceability can be decisive in regulated markets and downstream filings.

- Shijiazhuang Dowell Chemical (China) — A fine chemical manufacturer supplying DMBA and derivatives with substantial export volumes; the company reports sizable annual capacity in the low‑hundreds of metric tons and an explicit focus on pharmaceutical and pesticide intermediates. Strategic takeaway: large‑volume buyers and formulators should model scenarios around Dowell’s capacity when evaluating long‑term supply security.

Across these supplier profiles, three strategic inferences emerge: (1) quality certification and export readiness materially reduce transactional friction; (2) nimble, small‑volume suppliers remain critical for R&D and pilot supply; (3) scale players influence spot pricing and capacity availability — a structural feature that supports both procurement consolidation and targeted supplier development strategies.

Supply chain, process routes and regulatory friction — practical implications

Our analysis synthesizes process disclosures and patent filings that remain commercially relevant for 2026 planning. Established synthetic routes include carbonylation of isoamyl alcohol with formic acid under acid catalysis, Grignard addition to carbon dioxide followed by hydrolysis, and halide‑to‑nitrile intermediates that are subsequently hydrolyzed. Published process reports indicate achievable purities approaching 99% after purification and overall yields above 80% for certain pathways. These technical differentials are not academic: they feed directly into OPEX and purification capex considerations, and thus into supplier selection and backward‑integration economics.

On the trade side, DMBA’s HTS classification places it within a group of saturated acyclic monocarboxylic acids that are subject to customs scrutiny in several jurisdictions. For example, China’s MFN tariff and some general tariff formulations, together with supervision and inspection certificate requirements, can create non‑trivial landed cost delta and lead‑time risk. Procurement teams must account for customs regimes and inspection schedules when negotiating lead times and buffer inventories.

Strategic recommendations for 2026

- Embed scenario‑based procurement: implement at least two conditional supply agreements (one assured capacity, one responsive small‑volume supplier) to manage both scale and innovation pipelines.

- Prioritize supplier audits focused on process yields and purification steps: small improvements in crude yield or impurity management translate into material margin gains at scale.

- Assess tactical backward integration only when feedstock exposure and demand certainty exceed 3–5 year thresholds; otherwise favor capacity‑linked offtake and optionality.

- Negotiate customs and inspection clauses: pricing alone won’t secure margins — contractually allocate inspection delay risk and specify remedies for tariff reclassification events.

- Target bolt‑on acquisitions in markets where concentration is high but technical differentiation is low; CR3/CR5 concentration levels make localized consolidation an immediate path to margin expansion.

- Invest in greener, higher‑yield synthesis trials where regulatory trends favor lower solvent usage and fewer hazardous reagents — this both de‑risk regulatory exposure and creates differentiation.

How to use the full report

This strategic brief is a preview of the deeper, practitioner‑focused study published by PW Consulting. The full report contains the granular segmentation, supplier scorecards, historic pricing series and regional/application splits that are essential for contractual negotiation, bid modeling and investment memoranda. PW Consulting adheres to a “preview, then convert” approach: we present the evidence and frameworks that underpin strategy, while reserving detailed data slices and proprietary models for subscribers and clients who require the complete dataset for execution.

For corporate strategy teams preparing 2026 budgets, procurement leaders negotiating FY‑2026 contracts, or private equity and corporate development teams screening midstream opportunities, this report offers a clear, action‑oriented path from market insight to executable steps. Engage with PW Consulting for the full dataset and tailored advisory to convert 2026 market dynamics into measurable value.

For detailed analysis of this topic, please visit the official page:22 Dimethylbutyric Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com