Piezo On Insulator (POI) Market: Strategic Insights for 2026 — Executive Brief from PW Consulting

PW Consulting’s latest Piezo On Insulator (POI) Market report provides a decision-grade, forward-looking framework for executives and investors navigating the accelerating adoption of POI substrates across RF filters, resonators and emerging micro-acoustic systems. Built on a 2025 base year and a seven-year forecast horizon (2026–2032), the study combines high-resolution market modeling, supplier intelligence, scenario analysis and actionable playbooks designed for teams making near-term capital allocation, sourcing and product roadmap decisions in 2026.

Piezo On Insulator Poi Market

Why the POI market matters now

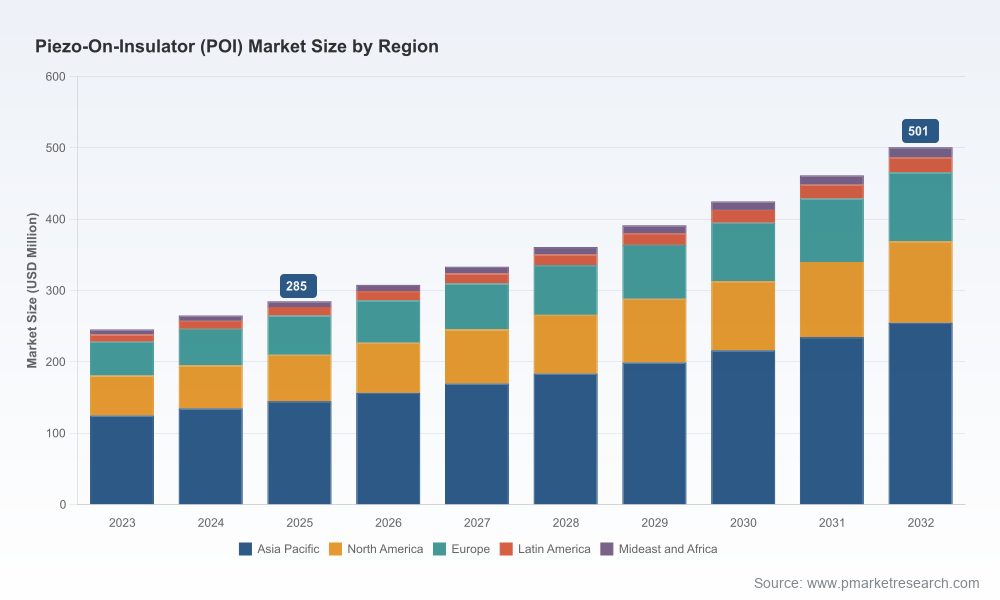

POI substrates — thin-film lithium tantalate (LiTaO3) and lithium niobate (LiNbO3) bonded to SiO2 on silicon — are rapidly moving from specialty research volumes into high-volume RF and sensing supply chains. This transition is driven by the imperatives of 5G/6G RF front-ends, higher-performance timing and resonator functions, and a growing set of non-telecom applications (ultrasonic sensing, MEMS-acoustic integration). Our macro modeling shows a clear, sustained expansion: the global POI market increases from a 2025 base to a significantly larger market by 2032, tracking a compound annual growth rate (CAGR) of 8.42% across the forecast window. In USD Million terms (base year 2025), our model projects a steady increase year-on-year through 2032, underscoring durable demand drivers rather than a one-off cycle.

Piezo On Insulator Poi Market

What PW Consulting’s report delivers (practical, procurement-ready content)

- Demand and revenue model: A transparent, bottom-up market model that maps end-market demand drivers to wafer-level consumption and revenue forecasts across the 2026–2032 horizon (unit and value outputs expressed in USD Million).

- Supplier scorecards and capacity maps: Granular operational intelligence on leading POI substrate producers, including factory capacities, technology roadmaps, wafer diameters supported and quality/qualification timelines — calibrated to support sourcing negotiations and dual-sourcing strategies.

- Use-case ROI calculators: Decision tools that allow product and platform teams to simulate cost/benefit trade-offs for migrating from bulk piezo materials to POI substrates across RF filter and resonator architectures.

- Scenario and sensitivity analysis: Up/down scenarios that stress-test revenue and supply outcomes against key variables — wafer yield improvements, layer-thickness standardization, raw-material price shocks and geopolitical supply disruptions.

- Regulatory and standardization playbook: A compliance timeline and proactive remediation checklist tied to environmental sourcing scrutiny and nascent standardization gaps that affect qualification cadence.

- M&A and partnership screening: A prescriptive framework and shortlist for potential inorganic moves and strategic partnerships, including a valuation lens that aligns with projected mid-term cash flows and concentration risk.

Market trajectory and concentration — what executives need to know

Our research demonstrates a market moving from concentrated specialist supply to a cautiously diversifying landscape. Three-firm concentration metrics indicate a meaningful share controlled by a few established producers, while a five-firm concentration shows increased but still significant aggregation. For 2026 strategists, the implication is two-fold: entrenched suppliers will continue to influence price, qualification timelines and technology standards, but there is real upside for entrants and regional champions who can close quality and capacity gaps.

Piezo On Insulator Poi Market

Competitive landscape — capabilities, positioning and near-term moves

The competitive map of POI suppliers blends global engineering leaders with agile regional specialists. Key players we analyze in-depth include:

- Soitec (Bernin, France): A leading provider of engineered substrates built on Smart Cut™ technology. Soitec has focused product lines for SAW RF filters in 5G/6G applications and offers multilayer LT and LN on insulator wafers at 150mm and 200mm. Recent developments — including a multi-year commercial agreement to supply volume POI wafers for a major RF platform and technical evaluations for space-grade SAW filters — underscore Soitec’s dual commitment to scale and qualification for demanding applications.

- Jinan Jingzheng Electronics / NANOLN (Jinan, China): A specialist in single-crystal LNOI and LTOI thin films, offering ultrathin film stacks and wafer services. Their focus on sub-micron film thicknesses positions them well for design wins where acoustic confinement and mode control are critical.

- Shanghai Novel Si Integration Technology (NSIT): Provides heterogeneous integration platforms addressing micro-acoustic and high-performance RF filters. Their portfolio is notable for integration of POI variants into downstream process flows for device makers.

- Beijing Qinghe Jingyuan: A domestic-oriented supplier concentrating on POI materials to meet local high-frequency filter demand, important for regional supply chain resilience in Asia.

- NGK Insulators (Nagoya, Japan): Leveraging ceramics and materials expertise to develop POI substrate variants, NGK’s know-how supports high-temperature and reliability-focused applications.

- frec’n’sys SAS: A wafer and device manufacturer with historical ties to the Soitec group, active in translating POI films into SAW/BAW devices.

- Inno Semiconductor Technology, PAM‑Xiamen (Powerway), Partow Technologies, Alfa Chemistry: A mix of advanced-material suppliers, substrate specialists and service providers enabling wafer processing, compound semiconductor support, and custom piezoelectric solutions for sensors and transducers.

Across these players, we track three competing strategies: (1) scale-and-integrate (industrialize Smart Cut or equivalent at larger wafer diameters), (2) specialization around ultrathin-film performance and process flexibility, and (3) regional supply‑chain capture through price/qualification speed. Our vendor scorecards evaluate each supplier on technology readiness, capacity scalability, qualification cycle, and geopolitical risk exposure.

Industry dynamics that will shape 2026 decisions

- Raw-material & production realities: POI substrates rest on LiTaO3 and LiNbO3 top layers in the sub-micron to micron range bonded to SiO2 on high-resistivity silicon. Top-layer thickness control and bond uniformity materially affect device performance and yield — a technical constraint that buyers and process engineers must explicitly model into qualification timelines.

- Standardization gap: There is no universally accepted standard for POI layer thickness, doping profiles or uniformity thresholds. That lack of interoperability slows cross-supplier integration and extends qualification cycles unless OEMs enforce strict incoming acceptance criteria or co-develop standards with suppliers.

- Regulatory & ESG scrutiny: Environmental and sourcing compliance for piezoelectric materials is tightening. Expect extended documentation requests, longer supplier audits and potential cost impacts related to traceability and responsible-material programs.

- Supply-chain and geopolitical exposure: Rare-earth and piezoelectric-related material volatility, plus regional concentration of capacity, introduce single-point risks. Companies should test dual-sourcing strategies and consider buffer capacity in 2026 procurement planning.

- Production scale-up: Leading substrate producers have announced or demonstrated capacity expansions; some report high annual wafer-equivalent outputs using proprietary lifting/bonding technologies. For OEMs this creates opportunities to secure long-term supply but also the imperative to lock commercial terms that reflect yield improvement timelines.

Strategic actions for 2026 — prioritized playbook

Based on our forecasts, risk analysis and supplier intelligence, PW Consulting recommends a prioritized set of actions for companies planning 2026 initiatives:

- Accelerate supplier qualification for strategic SKUs: Start parallel qualification with both incumbent and high-potential regional suppliers now. The industry’s non-standardized layer specs extend qualification timelines; early engagement buys critical lead time.

- Negotiate flexible offtake and NRE clauses: Favor commercial agreements that include step-up volumes, yield-linked pricing, and clear NRE amortization schedules to align incentives during scale-up phases.

- Invest in materials traceability and ESG compliance: Build supplier data requirements into RFPs and incorporate traceability clauses to preempt regulatory and buyer-driven due-diligence demands.

- Fund pilot lines and co-development partnerships: For OEMs dependent on acoustic performance differentiation, co-funded pilot fabs or process-shared R&D with substrate vendors can compress time-to-market and secure priority access to capacity.

- Stress-test architectures for POI migration: Use the report’s ROI calculators to evaluate when and where migration to POI yields durable system-level benefits versus incremental cost impacts.

- Maintain optionality through cross-domain suppliers: Consider partnerships with suppliers that have cross-product capability (e.g., ceramics, compound semiconductors, wafer services) to reduce single-technology dependency risks.

How corporate leaders should use this report in 2026

Product, procurement, corporate development and regulatory teams will each find specific sections of immediate use. Product teams can run device-level sensitivity analyses; procurement can use supplier scorecards and contract negotiation playbooks; strategy teams can adapt the scenario outputs for M&A prioritization; and compliance teams can deploy the regulatory timeline and checklists to close documentation gaps before qualification freezes.

Methodology note and access

Our findings are underpinned by a blended methodology: proprietary bottom‑up demand modeling, primary interviews with substrate and device manufacturers, and triangulation of public disclosures (press releases, patent filings, procurement notices). The study covers historical years leading into a 2026 start point and extends to 2032, providing a multi-year runway for capital planning. Aggregate market sizing and CAGR figures are published in this release to demonstrate macro trend alignment, while the full report contains the detailed segmentation, supplier scorecards, financial projections and templates required to operationalize the insights.

To preserve commercial leverage and client value, granular sub‑segment tables and per-region/application breakouts are intentionally gated in the public brief. PW Consulting encourages interested stakeholders to access the full report for detailed datasets, supplier contact matrices and the interactive decision tools referenced above.

Closing — what to act on in Q1–Q2 2026

2026 will be a pivotal year for firms betting on POI as a differentiator: markets are expanding at a robust mid-to-high single-digit CAGR, supplier concentration remains meaningful, and material/standardization dynamics will determine who moves fastest. Organizations that combine early supplier engagement, disciplined scenario planning, and targeted co-development will be best positioned to capture the operational and performance upside of POI while controlling supply and regulatory risk.

For access to the full PW Consulting Piezo On Insulator (POI) Market report, including the detailed vendor scorecards, scenario models and procurement playbooks, please visit our official report page or contact PW Consulting’s industry team for a briefing.

For detailed analysis of this topic, please visit the official page:Piezo On Insulator Poi Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com