Industrial Environment Monitoring System Market 2034: US Stands as Largest Shareholder Globally

Other |

2026-04-06 14:51:05

As energy transition priorities intensify and system operators demand higher grid stability, the double fed induction generator (DFIG) segment remains a central pillar of onshore wind strategy. PW Consulting’s new Double Fed Wind Turbine Market report (base year 2025; forecast period 2026–2032) synthesizes historical performance (2020–2025), near‑term inflections, and a seven‑year outlook to equip executives with the insight required to make decisive, risk‑calibrated moves in 2026. The market reached approximately USD 18,450 Million in 2025 and, at a compound annual growth rate (CAGR) of 5.25% across the forecast period, is projected to approach the mid‑to‑upper USD 26,000 Million range by 2032. This release highlights the report’s strategic value while preserving the detailed segment-level data to encourage direct engagement with our full dataset and tools.

Double Fed Wind Turbine Market

Established performance and repowering momentum: Mature supply chains, proven drivetrain architectures, and widespread operational experience mean DFIG remains a favored choice for rapid capacity improvement programs—especially repowering initiatives where modular replacement and balance‑of‑plant considerations dominate.

Double Fed Wind Turbine Market

Grid service expectations changing capital and O&M calculus: Evolving grid codes and higher expectations for voltage and frequency support are increasing the technical complexity—and therefore the cost tradeoffs—of DFIG systems as they integrate additional power electronics and control layers.

Double Fed Wind Turbine Market

Supply chain and material pressure: Rare earth market volatility and other raw material dynamics are shifting comparative economics between DFIG and permanent magnet synchronous generator (PMSG) architectures and must be boarded into procurement and hedging strategies.

The historical dataset through 2025 shows a clear expansion of the DFIG market from 2020 levels, driven by sustained onshore additions, repowering programs and selective offshore deployments where compatibility with existing infrastructure matters. With a forecast CAGR of 5.25% for 2026–2032, our scenario suite projects a steady rise in market value to roughly USD 26.4 billion by 2032 under the central case. The report quantifies downside and upside scenarios tied to commodity shocks, regulatory tightening, and accelerated decarbonisation policy, allowing capital planners to stress‑test capital allocation, levelized cost assumptions and payback horizons.

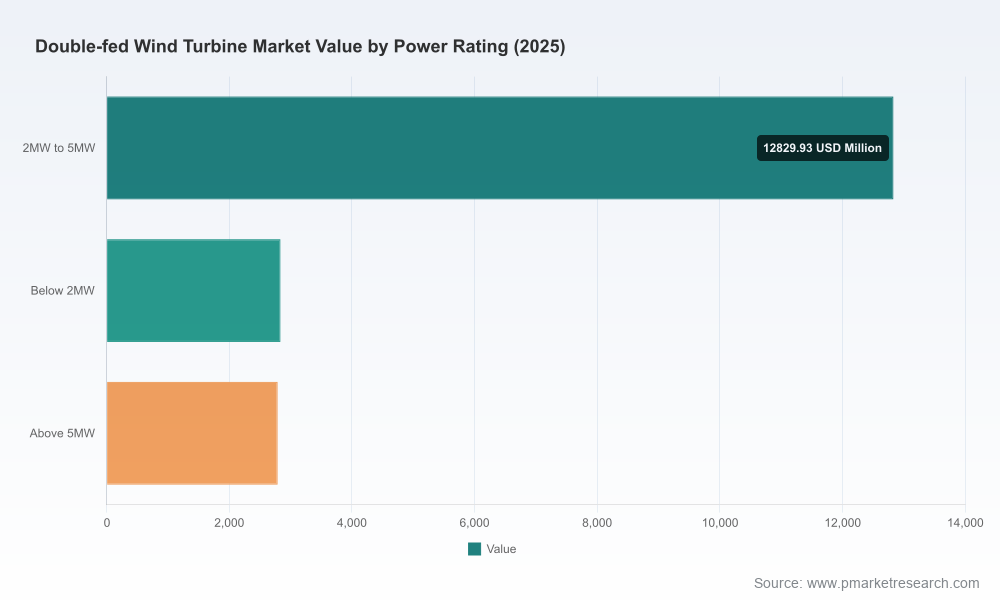

Repowering and the second life of Type III systems: European repowering projects continue to favor 4–6 MW DFIG platforms in many replacement programs, reflecting a cost‑to‑benefit balance between energy yield improvements and civil/connection constraints.

Grid code complexity: New requirements around fault ride‑through, reactive power provision, and frequency response are increasing the design requirements for DFIG solutions. These protocols typically translate into more sophisticated converter and control integration—areas where OEMs with strong R&D and systems integration capabilities will capture competitive advantage.

Technology convergence: Notably, research and pilot demonstrations have shown Type III DFIG platforms operating in grid‑forming modes to support system stability—expanding the operational envelope of DFIG beyond historical limits and opening a new class of service‑driven revenue streams.

Commodity volatility: Upstream material cost movements—most prominently rare earth price surges—are altering the relative cost profile of generator technologies. Year‑over‑year spikes of nearly 90% in certain rare earth prices in early 2026 underscore the need for purchasing strategies and design flexibility that minimize single‑commodity exposure.

The DFIG market remains characterized by a mix of global majors and regionally dominant OEMs. A concentrated supplier base means that top vendors currently control a substantial share of shipments, intensifying competition on product differentiation, service ecosystems and localization strategies. Key players addressed in our analysis include industry leaders and national champions such as Goldwind Science & Technology, Vestas, Siemens Gamesa, GE Vernova, Envision Energy, MingYang, Nordex SE, Suzlon, Shanghai Electric, Dongfang Electric, and CSSC Haizhuang. Our vendor profiles examine:

Product families and drivetrain choices (geared high‑speed DFIG vs. alternative architectures)

R&D pipelines and recent field demonstrations (including grid‑forming trials)

SERVICES: O&M frameworks, digitalization and remote diagnostic capabilities that extend margin capture post‑commissioning

Manufacturing footprint and supply‑chain linkages that affect delivery risk and local content strategies

For procurement teams, the report’s vendor scorecards highlight relative strengths in technology maturity, systems integration, proven field performance and aftermarket capability—enabling a defensible vendor selection process without relying solely on headline price comparisons.

PWC’s market release is intentionally action‑oriented. Deliverables are designed for quick assimilation into board papers, procurement RFPs and capital budgets. Highlights include:

Strategic executive summary with scenario-driven capital planning implications for 2026 decisions

Market forecast model (2026–2032) with sensitivity toggles for commodity price shocks, policy change, and repowering uptake

Vendor scorecards and procurement due‑diligence templates (technical, commercial, and operational criteria)

Repowering playbook: tender structures, balance‑of‑plant considerations, transition timelines and ROI calculators

Supply‑chain stress test: identification of single‑point vulnerabilities, alternate sourcing strategies and cost pass‑through mechanics

Regulatory compliance matrix aligned to evolving grid codes, plus a mapping of required control upgrades for DFIG platforms to meet next‑generation fault‑ride‑through and reactive support standards

Investment memos and investor Q&A decks tailored to project finance and strategic M&A use cases

To preserve strategic advantage for clients, granular segment tables and raw datasets (regional splits, power‑rating slices and application breakdowns) are held within the full report and interactive dashboards available from our web portal.

Reassess repowering pipelines through an integrated lens: prioritize sites with constrained grid capacity where DFIG’s operational flexibility can materially improve delivered energy without prohibitive civil works.

Hedge material exposure: build commodity‑linked clauses into long‑lead component contracts and pursue multi‑vendor sourcing for generator and converter assemblies to reduce single‑supplier dependence.

Invest selectively in control-system upgrades: retrofits that enable grid‑forming behaviours and advanced reactive management can unlock new ancillary revenue and simplify interconnection terms.

Operationalize vendor scorecards: adopt our procurement templates to quantify TCO drivers—availability, digital services, spare parts lead times and upgrade pathways are increasingly decisive.

Embed regulatory scenario planning into capex approvals: require projects to pass stress tests against tighter fault‑ride‑through and voltage control requirements before sanction.

Pursue partnerships for regional scale: OEMs and developers focusing on local manufacturing footprints and service networks will gain advantaged access to repowering and merchant projects that demand fast O&M response.

Sector developments underscore our strategic conclusions: major European repowering initiatives in 2025 prioritized 4–6 MW DFIG units to enhance yield without extensive site reconstruction, while an April 2026 offshore milestone demonstrated DFIG configurations remain relevant in broader project strategies. These examples validate the report’s core contention: DFIG technology is not simply legacy kit; it’s an adaptable asset class that, when combined with modern control upgrades and savvy supply‑chain management, will retain a meaningful role in the near term.

CFOs and portfolio managers: use the forecast and scenario tools to set capital allocation bands and to size hedging buffers for procurement exposure.

Procurement and technical teams: apply vendor scorecards and procurement templates to upcoming tenders to reduce delivery risk and shorten time‑to‑commission.

Regulatory and system planners: leverage the compliance matrix and grid‑forming readiness guidance to engage with TSOs and policymakers on credible interconnection timelines.

M&A and strategy teams: use the market concentration metrics and competitor profiles to identify consolidation targets, technology partnerships, or strategic joint ventures.

DFIG technology occupies a practical, strategic niche: it delivers value through repowering, aligns with existing infrastructure in many markets, and can be evolved through control and component upgrades to meet next‑generation grid duties. Our central forecast—market expansion from a 2025 base of roughly USD 18.45 billion at a 5.25% CAGR through 2032—underscores that the next 12–18 months will be decisive. Leaders who combine prudential procurement, commodity risk management, targeted control‑system investments and disciplined vendor selection will convert these market dynamics into durable advantage.

For a full set of segmented datasets, interactive models, vendor scorecards, and the repowering playbook referenced here, access the complete Double Fed Wind Turbine Market report and dashboards on PW Consulting’s official report page.

For detailed analysis of this topic, please visit the official page:Double Fed Wind Turbine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com