Ascorbic Acid Market Leadership Analysis: Competitive Landscape and Strategic Direction

Other |

2026-06-01 07:37:46

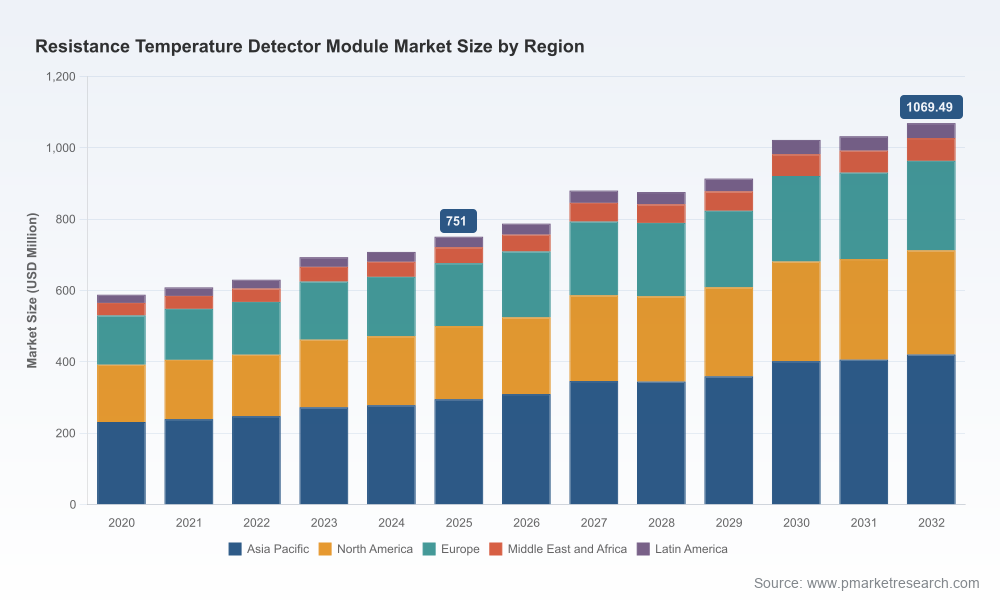

PW Consulting’s latest market research on Resistance Temperature Detector (RTD) modules delivers an action-oriented intelligence package designed to inform executive decisions in 2026. Built on a proprietary blend of bottom‑up supply mapping, buyer interviews, standards analysis, and scenario-driven forecasting, the report tracks the market from 2020 through a 2025 base year and projects through 2032. The RTD module market—already expanding from the mid‑single‑hundreds of millions of USD in 2020 to roughly three‑quarters of a billion by 2025—is modeled to reach just over one billion USD by 2032, representing a steady mid‑single‑digit CAGR over the forecast window. This brief summarizes the strategic implications without revealing the granular segment matrices reserved for subscribers.

Resistance Temperature Detector Module Market

Prioritize capital allocation with clarity: the report’s forecast envelope and sensitivity scenarios translate market momentum into prioritized investment opportunities across product, channel and geography.

Resistance Temperature Detector Module Market

De‑risk sourcing and raw‑material exposure: with platinum‑based sensing elements remaining commercially dominant, procurement teams can use the report’s supplier risk frameworks to secure throughput and margin targets.

Resistance Temperature Detector Module Market

Design go‑to‑market blueprints: product managers receive actionable playbooks to accelerate adoption of RTD modules within PLC/DCS ecosystems and adjacent automation stacks.

Inform M&A and partnership screening: the market concentration analysis and vendor scorecards flag consolidation targets and potential integration risks for acquirers.

Align compliance and engineering roadmaps: the report translates major standards into engineering and QA checklists to shorten time‑to‑certification.

Market sizing & forecasting: transparent methodology (base year 2025; historical 2020–2025; forecast 2026–2032), scenario runs, and a modular financial model that lets clients re‑cast projections under alternate assumptions.

Demand‑driver heatmaps: decomposition of end‑market pull (industrial automation, process control, HVAC and building systems, and critical infrastructure) and short‑term vs structural growth vectors.

Supply‑chain map and raw‑material analytics: upstream concentration, critical component suppliers for thin‑film platinum elements, and sourcing levers to mitigate price and availability shocks.

Competitive intelligence: vendor scorecards, capability matrices, product roadmaps and benchmarking against interoperability standards.

Commercial playbooks: channel segmentation, pricing elasticity guidance, contract language templates, and a checklist for value‑added services (calibration, extended warranties, remote diagnostics).

Implementation tools: downloadable Excel models, vendor selection templates, sensitivity analyses, and a procurement risk register tailored for 2026 projects.

The RTD module market exhibits a moderate level of concentration: the top three players hold a meaningful share of industry revenues, and the top five capture a clear majority of industry value. This structure creates a dual strategy for incumbents and challengers alike—scale and integration offer margin and channel advantages, while niche specialization and services create defensible pockets of value.

Omega Engineering, Inc. (Norwalk, Connecticut, USA; https://www.omega.com): breadth of product lines and strong lab/industrial brand recognition make Omega a default partner for engineering teams; their strategy centers on configurable assemblies and rapid delivery.

TE Connectivity (Schaffhausen, Switzerland; https://www.te.com): deep materials and thin‑film expertise positions TE as a materials‑to‑module supplier; their investments in standards compliance and ruggedized elements are a competitive moat in harsh environments.

Minco Products, Inc. (Minneapolis, Minnesota, USA; https://www.minco.com): long history of custom and mission‑critical sensors gives Minco a premium position in aerospace, defense and medical segments where tailored solutions and qualification support win contracts.

Honeywell (Charlotte, North Carolina, USA; https://automation.honeywell.com): integration into automation ecosystems and enterprise service offerings favor Honeywell where buyers seek end‑to‑end control solutions rather than point components.

Watlow (St. Louis, Missouri, USA; https://www.watlow.com): combining RTD sensing with heating systems allows Watlow to capture higher value by selling integrated thermal subsystems.

Dataforth Corporation (Tucson, Arizona, USA; https://www.dataforth.com): specialist in signal conditioning and isolation—critical for customers focused on measurement integrity in noisy industrial environments.

Pyromation, JUMO, ABB, Rockwell Automation, Axiomatic Technologies, Opto 22: collectively they represent a mix of industrial incumbents, PLC/DCS integrators, and niche module designers. Each leverages channel strength or vertical focus to defend share.

Standards and interoperability: IEC 60751 remains the cornerstone for platinum RTD interchangeability, and updated standards (including ASTM‑aligned guidance) have direct implications for module linearization, calibration protocols and field replacement procedures. Engineering teams must map product specs against these standards to avoid rework and warranty exposure.

Materials and sourcing: platinum‑based thin‑film sensing elements continue to underpin module performance. The market for thin‑film platinum components is large and growing, which influences lead times and procurement strategies for module manufacturers.

Automation adoption: broader digitization in process control and building systems increases demand for RTD modules with higher stability, better noise rejection, and integrated diagnostics—features that command price premiums and recurring service revenue.

Regulatory and safety expectations: end users increasingly require documented calibration chains, traceability to standards, and cybersecurity considerations when modules interface with control networks; vendors that embed compliance into product design shorten sales cycles.

Secure critical inputs: develop multi‑tier supplier relationships for thin‑film platinum elements and negotiate capacity guarantees or forward‑buy arrangements where appropriate.

Productize reliability: invest in linearization algorithms, isolation, and self‑diagnostics to differentiate in engineering‑led procurements; certify modules against IEC 60751 and relevant ASTM guidelines.

Pursue selective consolidation: acquirers should target niche specialists that provide complementary capabilities (e.g., signal conditioning, harsh‑environment scanners, or calibration services) rather than horizontal roll‑ups alone.

Monetize services: bundle calibration, remote diagnostics, and lifecycle management to move from single‑sale hardware to recurring revenue models.

Channel optimization: align sales and technical resources with PLC/DCS integrators and system houses; streamline compatibility matrices for major automation platforms to reduce integration friction.

Invest in field validation: accelerate adoption by funding pilot programs with anchor customers, using structured ROI templates and service SLAs to reduce buyer risk.

Beyond the strategic analysis above, the full PW Consulting report provides the granular segmentations, vendor scorecards, downloadable financial models, and prioritized initiative roadmaps necessary to operationalize your 2026 strategy. Subscribers gain access to a locked dataset that includes segment‑level forecasts, channel economics, and competitive positioning matrices—designed so corporate development, product, and procurement teams can move from insight to execution within weeks, not months.

If your 2026 planning cycle includes procurement, product development, or M&A related to thermal sensing and control, use this report as the single source of truth for scenario planning and risk mitigation.

To obtain the full intelligence package (segment tables, fill‑rate models, vendor heatmaps and implementation templates), visit our PW Consulting research portal or contact our advisory team for a tailored briefing that maps the findings directly to your P&L and project timeline.

PW Consulting’s RTD Module Market report is intentionally crafted as a decision engine: it surfaces the commercial contours you need today, and the tactical toolset to act on them in 2026—with the detailed segment‑level data and downloadable assets reserved for report subscribers to preserve the competitive advantage that comes from exclusive, actionable intelligence.

For detailed analysis of this topic, please visit the official page:Resistance Temperature Detector Module Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com