Solid State Chip Battery Market: 2026 Strategic Briefing — What Growth, Competition and Regulation Mean for Executive Decision-Making

As PW Consulting’s lead industry analyst, I present a strategic briefing derived from our new market research report on the Solid State Chip Battery market (base year 2025; historical window 2020–2025; forecast 2026–2032). The market is in an inflection phase as the combination of materials advances, pilot-scale manufacturing and system-level integration accelerates commercial pathways. Our modeled market trajectory shows a compound annual growth rate (CAGR) of 19.0% across the 2026–2032 forecast window, underpinned by rapid adoption in micro-power, IoT endpoints, wearables and nascent automotive formats. Total industry revenue expanded materially between 2020 and 2025 and continues into 2026 under our base scenario, with projected market scale rising substantively through 2032 (figures reported in USD Million in the source report).

Solid State Chip Battery Market

Why this report matters for 2026 decision-makers

- Timing and runway: 2026 is a critical year for translating pilot demonstrations into qualified supply for system OEMs. Our forecast and scenario models quantify the market opportunity and the sensitivity of that opportunity to key gating factors — electrolyte cost, interface stability, qualification timelines and regulatory acceptance.

- Capital allocation: With a high-growth outlook and pronounced technology risk, capital must be staged against de-risking milestones. The report provides a capex and cash-burn playbook mapped to technology maturity states so CFOs can align financing rounds, JV structures and milestone-based tranches.

- Partnership and go-to-market design: For product and BD leaders, we map the appropriate partnership archetypes — from licensing and tolling to equity partnerships and co-development — based on application class, cell format and target OEM qualification cycles.

- Supply chain and operations: Manufacturers face moisture-sensitive materials, special handling and new equipment requirements. Our operations playbook prioritizes the top manufacturing investments and process controls that yield the earliest unit-cost reductions.

Market snapshot (high-level)

From a practical vantage, the market has moved from research and small-scale pilots into multiple, concurrent pilot/early-commercial tracks. Our report records the historical revenue curve through 2025 and provides a year-by-year forecast from 2026 to 2032. The modeled base case — reflecting current project announcements, pilot lines and known customer qualifications — yields a long-term CAGR of 19.0%. This reflects a shift from premium-priced, specialized applications toward broader adoption as manufacturing scale, supply chains and standards converge.

Solid State Chip Battery Market

Importantly, the market is neither hyper-fragmented nor highly consolidated: the top three firms control a meaningful share of the market, but the top-five still represent only a majority rather than near-total domination. This competitive structure creates room for differentiated entrants to win valuable niches through technology specialization, manufacturing excellence or strategic OEM relationships.

Solid State Chip Battery Market

What executives will find in the report (actionable content)

- Proprietary forecasting model: Scenario-based forecasts (base, accelerated, delayed) with sensitivity levers for electrolyte cost, yield improvements, and OEM qualification timing.

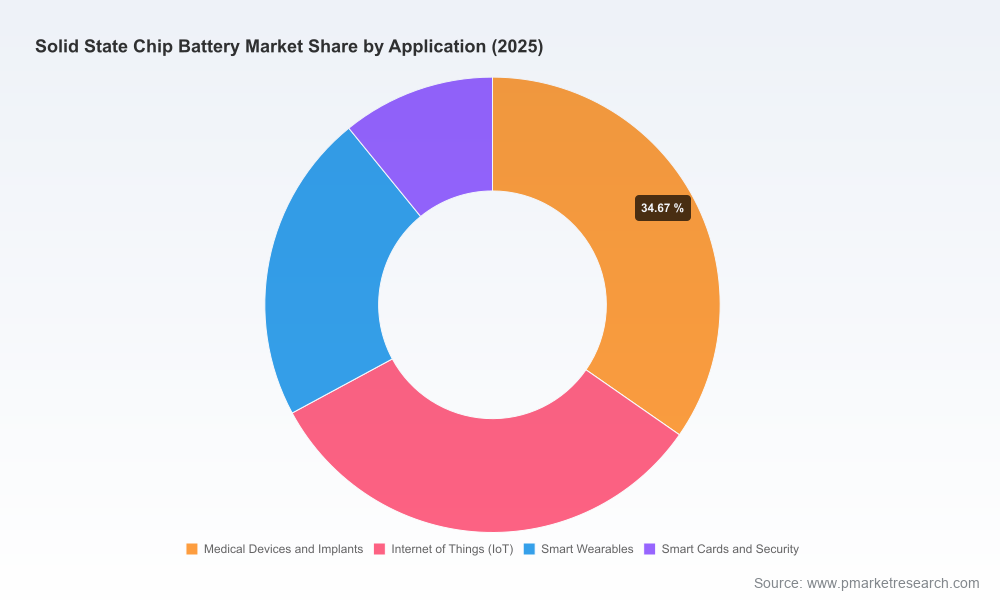

- Go-to-market playbooks: Concrete GTM strategies by application cluster (micro-power, IoT, wearables, smart cards and automotive pilot programs) including channel mapping, sample-to-qualification timelines and pricing corridors.

- Capex & unit-cost modeling: Detailed equipment lists, floor-plan templates and an incremental cost curve showing the path to parity with incumbent lithium-ion for selected formats.

- Supply chain risk matrix: Sourcing strategies for solid electrolytes and critical precursors, alternative supplier maps and inventory policies to mitigate moisture-sensitive materials risk.

- Manufacturing scale-up templates: Pilot-to-volume stage-gates, automation investments, environmental controls, and recommended yield tracking metrics tailored to solid-state chemistries.

- Regulatory and standards playbook: A compliance checklist tied to emerging national standards, air-transport and hazardous-materials rulemaking, and vendor qualification requirements.

- Competitive heatmaps and M&A target shortlist: A qualitative and quantitative assessment of players by technology readiness, IP position and partnership traction, plus suggested diligence questions for acquirers.

- Decision-support appendices: Term sheets, sample commercialization milestones, and scenario decision trees designed to support board and investment committee deliberations in 2026.

Competitive landscape — what matters to strategy teams

Solid-state battery development now encompasses a spectrum of approaches — thin-film, bulk and semi-solid formats — each with different manufacturability and application implications. Several firms demonstrate clear leadership in particular vectors:

- QuantumScape (San Jose) continues to push high-energy lithium-metal concepts targeted at automotive energy density gains. Its sample shipments to automotive customers and focus on anode-less architectures position the firm as a flagship for high-risk, high-reward EV applications.

- Solid Power (Colorado) has oriented to automotive-scale qualifications by leveraging more traditional lithium-ion process heritage, forging strategic OEM partnerships that reduce the integration risk for carmakers pursuing a step-change in cell safety and energy density.

- Factorial Energy (Methuen) and Ilika (UK) illustrate divergent but complementary playbooks: Factorial has moved rapidly to assembly-scale pilot lines and broad OEM collaboration spanning drones to passenger vehicles; Ilika focuses on both micro-power thin-film strengths and scaling to larger formats with its Goliath prototypes.

- ION Storage Systems’ recent customer qualification milestone marks an important commercial inflection — demonstrating a pathway for US-based cell suppliers to move from samples to qualified units for consumer electronics cohorts.

- ProLogium, Blue Solutions and several Asian incumbents are notable for practical engineering progress and a focus on safety and pack-level integration targeting both mobility and stationary markets.

- Large incumbents and OEMs — notably CATL and Toyota — are significant to watch because their patent activity, pilot initiatives and supply-chain heft can accelerate standards, regulatory alignment and scale economics once commercialization windows open.

For corporate strategists, the competitive implication is straightforward: seek partnerships that reduce first-of-kind integration risk and align incentives across suppliers, integrators and OEMs to accelerate qualification cycles. Our competitive matrix in the full report helps prioritize which partners are best suited for equity, JV, or toll-manufacture arrangements — guidance that is intentionally granular and available in the detailed report.

Technology, manufacturing and supply-chain dynamics

Two technical friction points determine near-term commercial outcomes: (1) the cost and manufacturability of solid electrolytes and (2) interface stability at scale. Industry intelligence indicates solid electrolyte raw-material and processing costs are currently multiple times higher than for conventional Li-ion electrolytes. Moisture sensitivity, specialized deposition and handling requirements create distinct CAPEX and OPEX profiles for new lines. Our manufacturing playbook quantifies these trade-offs and prescribes a staged investment approach to preserve runway while achieving targeted unit-cost declines.

Operational leaders should prioritize pilot investments that validate yield and interface stability under real-world assembly conditions. We provide recommended acceptance gates and test protocols that accelerate customer qualification without exposing partners to undue risk.

Regulatory and standards environment — a decisive influence in 2026

- Global standardization initiatives are converging in 2026. National and international rules — from China’s planned national technical standard to evolving PHMSA/IATA/ICAO alignments and UL-led safety standards — will materially affect transport, storage and field-use constraints for certain cell formats.

- Mandatory state-of-charge limits for certain battery shipments and proposed hazardous materials harmonization are already altering packaging, logistics and field-replacement strategies. Firms that integrate regulatory compliance into early design and logistics planning will enjoy faster time-to-market and lower thermal-hazard insurance costs.

PW Consulting’s regulatory matrix in the report maps out jurisdictional variances and recommends policy engagement approaches for industry consortia and corporate public affairs teams.

Recent industry developments to factor into 2026 plans

- CATL published patents in early 2026 targeting sulfide electrolyte stability and a 500 Wh/kg class cell with a pilot production timeline — a reminder that large incumbent battery manufacturers are actively pursuing breakthrough-density architectures.

- ION Storage Systems’ customer qualification milestone in March 2026 underscores that US-based developers can achieve commercial validation milestones in consumer electronics cohorts.

- Ilika’s shipment of higher-capacity prototypes and Factorial Energy’s pilot-line commissioning illustrate how multiple technology pathways are entering production-readiness stages simultaneously.

Investment, M&A and partnership implications

For corporate development and PE teams, the market presents staged buy-and-build opportunities: acquire specialized cell designers to secure IP, or invest in automation and environmental-control vendors to capture manufacturing margin. Our deal-framework appendix ranks acquisition targets by strategic fit, required follow-on investment and expected time-to-positive-cash-flow under each forecast scenario.

Key recommendations for 2026:

- Adopt milestone-linked investment: Tie follow-on capital to clear technical milestones (e.g., customer qualification, pilot yield thresholds, electrolyte cost parity targets).

- Form consortiums for standards engagement: Lead or join cross-industry consortia to shape standards and accelerate acceptance for transport and safety protocols.

- Prioritize modular manufacturing pilots: De-risk through modular, scalable lines that allow mixed-format production until a dominant cell architecture emerges.

- Negotiate OEM co-development agreements that align IP sharing with volume commitments to accelerate qualification and procurement timelines.

Accessing the full intelligence

This briefing highlights the strategic contours you must consider in 2026, but it intentionally omits the granular sub-segmentation numbers and detailed company-by-company forecasts that underpin our advisory recommendations. To obtain the full dataset — including application- and format-level demand curves, pricing bands, supplier scorecards and the proprietary forecast workbook — please consult the complete PW Consulting Solid State Chip Battery Market report and supporting dashboards available on our website. The detailed analysis will equip executives to make defensible, time-sensitive capital and partnership decisions in this rapidly evolving market.

For bespoke advisory support — scenario workshops, due-diligence support or negotiation playbooks tied to the report’s findings — PW Consulting’s industry team stands ready to translate these insights into executable plans aligned to your corporate objectives.

For detailed analysis of this topic, please visit the official page:Solid State Chip Battery Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com