Distilled Gum Turpentine Market — Strategic Imperatives for 2026

PW Consulting’s newest market study on the Distilled Gum Turpentine sector synthesizes five years of observed dynamics and a seven‑year forecast to deliver board‑grade insight for commercial, procurement, and investment decision‑makers planning for 2026. The market briefing is designed as a high‑signal “teaser” — enough analytical depth to inform near‑term strategy and risk mitigation, while reserving the full set of proprietary segment tables and supplier-level volumes for the full report available on our portal.

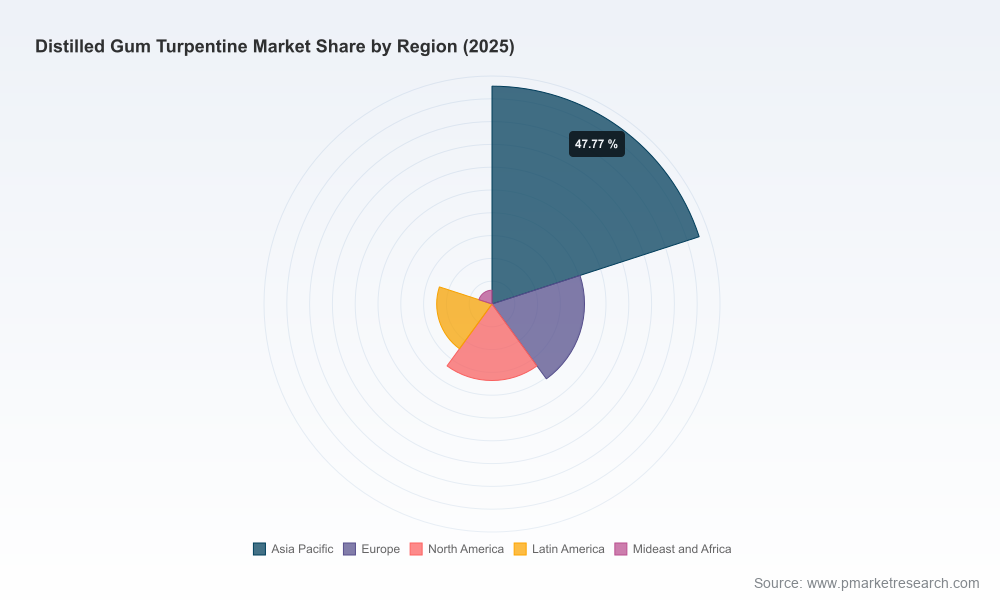

Distilled Gum Turpentine Market

Executive snapshot

After tracking the market through the 2020–2025 period, PW Consulting’s base‑year analysis confirms a durable recovery and gradual expansion of the distilled gum turpentine market. Total industry revenue moved from the mid‑500s (USD Million) in 2020 to the mid‑700s by 2025, reflecting recovering end‑market activity and feedstock‑driven pricing cycles. Our forecast period (2026–2032) produces a steady compound annual growth rate (CAGR) of approximately 4.81%, culminating in a market size that exceeds the billion‑dollar threshold by the early 2030s under our central scenario.

Distilled Gum Turpentine Market

Market concentration is moderate: the three largest producers account for well under half of global supply, while the top five capture just over half — a structure that preserves local competitive advantages and creates room for nimble entrants and regional champions to influence price and service dynamics.

Distilled Gum Turpentine Market

Why 2026 is an inflection year

- Feedstock volatility. Recent episodes of constrained gum rosin processing and fluctuating tapping yields have pushed regional turpentine prices sharply higher at specific points, and continue to transmit margin pressure downstream. These shocks have exposed the sensitivity of processors and formulators to upstream availability and logistics.

- Upgrading and premiumization. Producers are investing in rectification and fractionation capacity to supply higher‑purity grades (including pharmaceutical‑grade and ultra‑high‑alpha pinene fractions). This bifurcates supply into commodity solvent streams and premium specialty inputs, creating differentiated margin pools.

- Regulatory and labeling pressure. Ongoing EU substance registrations and regional consumer‑safety labeling requirements (including U.S. consumer product rules for concentrated turpentine formulations) necessitate proactive compliance roadmaps. Non‑compliance risk is not hypothetical: it can materially impede market access or alter product formulation economics.

- Strategic investment window. Capacity announcements and product launches over the past 18 months indicate a tightening window for securing offtake and raw‑material contracts — a critical factor for manufacturers looking to scale into adjacent chemical intermediates or fragrance markets in 2026.

What the PW Consulting report delivers — practical, board‑usable content

The full report is structured to translate market intelligence into executable choices. Key deliverables include:

- Proprietary market sizing and a scenario‑based forecast model (2026–2032) that can be instantiated with client assumptions for price, feedstock, and demand elasticity;

- An actionable supplier and asset map highlighting capacity types (commodity distillation, continuous rectification, terpene fractionation) and where premium grades are emerging;

- Price and margin drivers analysis coupling feedstock cost paths with downstream formulation demand cycles and logistics constraints;

- Regulatory compliance playbook tailored to EU REACH and U.S. consumer‑product labeling requirements, including recommended registration timelines and technical dossiers;

- M&A and partnership screening framework with a shortlist of target archetypes, integration risks, and valuation sensitivities;

- Commercial negotiation templates and an offtake scoring matrix to prioritize suppliers by technical fit, security of supply, sustainability credentials, and total cost of ownership.

To preserve competitive value for clients, the report’s full segmentation tables and supplier‑level volumes are included only in the paid deliverable — the summary above is intentionally diagnostic while remaining non‑exhaustive.

Competitive dynamics — profiles and strategic implications

The market is populated by both long‑tenured regional specialists and global chemical players. Notable incumbents demonstrate differentiated strategies that should inform competitive response and sourcing decisions:

- Yunfu Linxing Pine Chemicals Co., Ltd. — A seasoned Chinese producer with extensive experience in producing high‑quality gum turpentine for solvents and intermediate processing. Their scale and product breadth make them a logical partner for manufacturers prioritizing integrated supply chains.

- ACM Resinas — A European supplier with a forest‑sourced supply proposition, well positioned to serve regional coating and varnish sectors where sustainability narratives and traceability are prioritized.

- PT Global Darya Mandiri — An Indonesian producer leveraging Pinus merkusii feedstock; their alpha‑pinene‑rich streams are attractive to formulators seeking solvent performance and derivative chemistry feedstock.

- Diamond G Forest Products, LLC — A U.S. family agribusiness that underscores the role of on‑farm, sustainable sourcing and traditional distillation. Their model is instructive for niche supply strategies focused on provenance and small‑volume specialty grades.

- DRT (Dérivés Résiniques et Terpéniques) — A European terpene specialist that has signaled capacity expansion of fractionation assets; this will materially increase availability of ultra‑high‑purity fractions when commissioned, shifting feedstock economics for downstream specialty chemistries.

- Wuzhou Pine Chemicals Ltd. — Recent facility upgrades to produce pharmaceutical‑grade rectified turpentine illustrate how capital projects can unlock new end‑markets and improve margin capture for producers willing to certify to pharmacopeia standards.

- Kraton Corporation — A bio‑platform player introducing high‑purity alpha‑pinene products under a renewables brand; their upstream integration into pine chemical streams shows how incumbents can convert a commodity into a higher‑value, branded input.

Collectively, these actors explain the observed CR3 and CR5 dynamics: market leadership is meaningful but not monopolistic, ensuring strategic options for buyers that combine multiple regional suppliers with premium domestic sources.

Industry noise that matters for 2026 planning

- Raw material price spikes and regional supply constraints have already led to sharp short‑term price moves at specific ports and origin points; these remain the principal near‑term volatility vector.

- Feedstock co‑product economics (notably gum rosin and pine oleoresin) continue to shape turpentine availability and margins; fluctuations in those markets will cascade through the value chain.

- Policy and labeling requirements are active risks that should be embedded in product launch risk registers — delays in registration or mis‑labeling can interrupt access to large consumer markets.

Actionable strategic pathways for 2026

Based on our analysis, senior leaders should prioritize a small set of concrete moves in 2026:

- Secure diversified offtake commitments. Sign near‑term contracts with a mix of regional suppliers and premium‑grade producers to balance cost and reliability.

- Invest selectively in upgrading capability. If margin expansion or market entry into pharma and fine chemicals is a priority, target rectification and fractionation either through capex or joint ventures.

- Hedge feedstock exposure. Implement contract structures that share the pain and gain of raw‑material swings, and maintain buffer inventories calibrated to price‑tolerance tests in the PW forecast model.

- Operationalize regulatory readiness. Build registration timelines into product roadmaps today, not tomorrow — lead times for dossiers and analytical validation can be eight to twelve months or more.

- Differentiate on sustainability and traceability. Buyers increasingly reward verified origin and lower carbon intensity; pursue certification and chain‑of‑custody pilots with upstream partners.

- Prepare M&A playbooks. Use the report’s target archetypes and integration risk matrix to accelerate any acquisition due diligence and shorten decision cycles.

How to use this research in your 2026 planning cycle

Boards, procurement committees, and corporate development teams can use the PW Consulting deliverable in three immediate ways:

- Run scenario workshops using the included forecast model to stress‑test pricing, margin, and inventory strategies under alternative raw‑material and regulatory outcomes;

- Shortlist suppliers for commercial audits using our scoring matrix and request targeted samples for technical qualification against your formulation needs;

- Integrate the regulatory playbook with legal and product teams to ensure that any planned product introductions meet regional requirements without last‑minute reformulation.

Our research is intentionally prescriptive: it converts market observation into a prioritized set of commercial actions. The executive summary above highlights the directional insights you need to act in 2026; the full PW Consulting report contains the granular segment tables, supplier matrices, and downloadable financial models required to execute these recommendations.

For the full dataset, including regional and application breakdowns, supplier volumes, and customizable forecasting tools, please visit our report page. PW Consulting clients can also commission a tailored briefing to map these findings into company‑specific scenarios and implementation roadmaps.

For detailed analysis of this topic, please visit the official page:Distilled Gum Turpentine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com