The 10 Sites Guide to Buying Old Yahoo Accounts

Drinks |

2026-06-14 16:54:15

PW Consulting's forthcoming market study on RNA Therapeutics and Vaccines frames the technology class as a maturing but still rapidly evolving sector that will materially reshape product portfolios, manufacturing footprints, and commercial strategies between 2026 and 2032. Our analysis combines an actionable market model, competitor diagnostics, regulatory and reimbursement mapping, and supply-chain risk scoring to help senior executives and investors make high-conviction decisions in 2026.

Rna Therapeutics And Vaccines Market

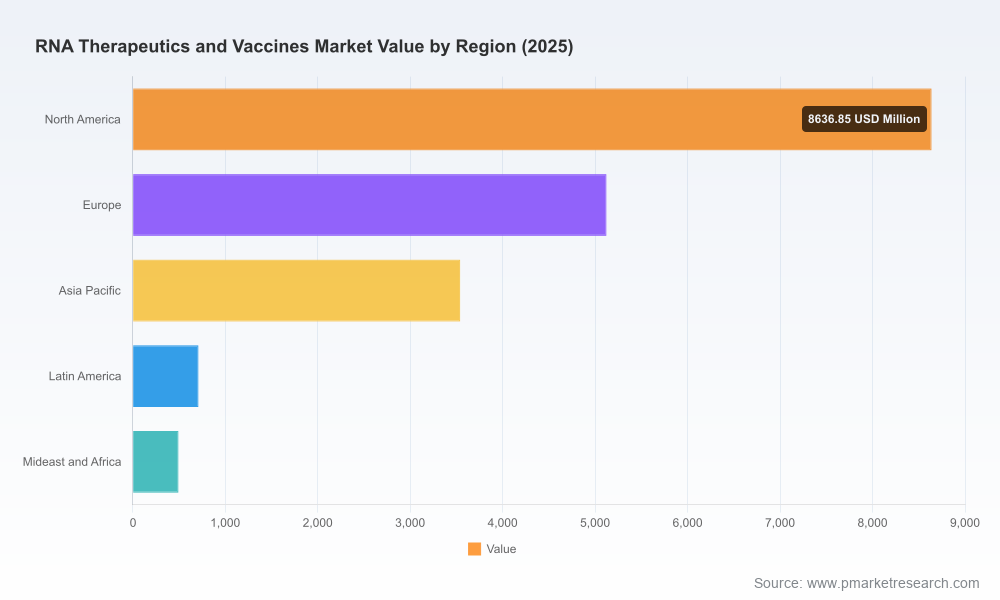

The category has moved from niche R&D programs into scaled commercialization within a five-year window. The PW Consulting market model shows the industry expanding at a compound annual growth rate (CAGR) of 12.5% across our forecast horizon (2026–2032), underpinned by accelerated approvals, platform-enabled pipeline maturation, and broader payer acceptance for selected indications. By the report's base year (2025) aggregate market revenues reached a clear inflection point, and our forecast anticipates continued acceleration through 2032 driven by both vaccine and therapeutic modalities.

Rna Therapeutics And Vaccines Market

Resource allocation: With platform investments and manufacturing capacity decisions being capital intensive and long lead, our report provides a timing-sensitive view to prioritize projects that will likely enter commercial inflection points during 2026–2028.

Rna Therapeutics And Vaccines Market

Partnering and M&A: The mid-term runway to 2032 creates asymmetric value for earlier-stage players with differentiated delivery technologies or rare-disease franchises. We highlight realistic partnership archetypes and valuation drivers that matter in negotiation windows opening in 2026.

Regulatory and payer strategy: The interplay of evolving regulatory expectations and nascent reimbursement pathways will determine the commercial viability of expanded indications. Executives need tactical roadmaps for accelerated approvals, label strategy, and payer engagement now — not later.

High-level market sizing and trend analysis are a core part of our toolkit. PW Consulting documents a sustained multi-year growth trend into the mid-2030s with a robust CAGR of 12.5%—a rate that forces strategic reorientation for incumbent vaccine and biopharma manufacturers. That said, our "trailer" approach deliberately withholds proprietary segment breakdowns and fine-grain regional revenue slices from this public preview: the full report contains the granular segmentation, scenario-based models, and downloadable datasets that clients use to build business cases and investment memoranda.

The RNA ecosystem shows concentrated but dynamic market leadership. A small set of platform-enabled companies capture a majority of commercial momentum, while an active cohort of next-generation entrants is winning scientific and clinical differentiation. Our competitive map and company playbooks in the full report analyze capability stacks, enabling technologies, and strategic positioning for the following representative firms:

Moderna, Inc. — A commercial leader with multiple authorized mRNA vaccines and an expansive infectious disease and oncology pipeline. Recent regulatory movements in 2025 and early 2026 have clarified near-term commercial pathways for seasonal and variant-targeted vaccines, impacting manufacturing cadence and demand forecasts.

BioNTech SE — A platform player balancing large-scale vaccine commercialization with personalized oncology ambitions. Its strategic alliances and IP portfolio make it a pivotal counterparty for companies seeking co-development or co-commercialization structures.

Pfizer Inc. — As a commercialization partner and technology integrator, Pfizer brings broad global reach and commercialization experience that can accelerate adoption of platform innovations when combined with technology-focused partners.

CureVac N.V., Arcturus Therapeutics, Ethris GmbH — These companies represent differentiated technical approaches (sequence design, self-amplifying constructs, mucosal delivery) that could reframe clinical differentiation in respiratory and other indications if their clinical programs read out positively.

Alnylam, Ionis, Arrowhead — Leaders in RNAi and antisense spaces whose regulatory precedents and commercialization experience in genetic and rare diseases provide playbooks that mRNA-focused teams can adapt for therapeutics beyond vaccines.

Regulatory momentum in late 2025/early 2026 around updated seasonal and variant-targeted mRNA vaccines signals an operational shift from emergency-use dynamics to routine, label-driven product cycles. This changes supply planning, demand forecasting, and lifecycle management priorities.

Clinical advancement and public-funded collaborations—such as awards and consortiums supporting pandemic influenza vaccine platforms—underscore a bifurcated innovation model in which public-sector risk-sharing accelerates platform de-risking for private partners.

Company-level clinical milestones for intranasal or mucosal delivery candidates demonstrate an increasing emphasis on alternative routes of administration that may substantially alter cold chain and distribution economics if they reach the clinic successfully.

Three structural inputs require immediate attention in any 2026 operations plan:

Cold chain logistics: RNA products' cold chain needs remain a cost and execution constraint in geographies with unstable power or limited logistics capacity. Thermostable formulations and next-gen lipid carriers could materially reduce distribution friction, but their commercial availability and adoption timelines must be factored into go-to-market sequences.

Raw material cost volatility: Critical reagents used in in vitro transcription (IVT) and lipid manufacturing have experienced meaningful price pressure and intermittency. Buyers should evaluate strategic procurement, dual-sourcing, and backward-integration scenarios to protect gross margins.

Regulatory and reimbursement environment: Regulators are actively refining standards for platform technologies while payers are establishing precedent-based pathways for reimbursement. Early payer engagement and value-creation evidence generation will be decisive for commercialization success.

Prioritize platform scalability over single-asset optimization. Capital allocation favoring flexible, modular manufacturing footprints will preserve optionality as platform applications expand.

Design partnership playbooks now. Whether pursuing licensing, co-development, or M&A, firms should align governance, data-sharing, and milestone structures to reflect platform risk profiles and expected regulatory timelines.

Invest in supply-chain resilience. Scenario planning for reagent shortages, tariff impacts, and cold-chain failures should be translated into concrete contingency investments and contractual terms.

Refine regulatory evidence packages for payers. Adopt adaptive clinical designs and real-world-evidence plans that demonstrate comparative value within the first 12–24 months post-approval.

Explore differentiated delivery routes as strategic hedges. Mucosal and thermostable approaches carry potential to unlock new markets or materially reduce distribution costs; their strategic value depends on clinical timelines that should be monitored closely.

The full PW Consulting report is designed as an operational playbook, not an academic compendium. Core deliverables include:

Dynamic market model (downloadable) with base, upside, and downside scenarios through 2032, enabling users to run sensitivity analyses tied to approval timing, pricing, and uptake assumptions.

Executive playbooks for manufacturing scale-up, partnership structures, and regulatory engagement—each with prioritized checklists, timeline templates, and budgetary heuristics.

Competitive profiles and capability matrices for key platform and therapeutic players, including risk/opportunity diagnostics and likely moves for the next 18–36 months.

Supply-chain risk heatmap and procurement stress tests that quantify the P&L impact of reagent price shocks and cold-chain failures under multiple scenarios.

Reimbursement and market access roadmaps by indication class, with recommended evidence generation pathways and payer-engagement milestones.

Early access users—biotech executives, corporate strategy teams at pharma companies, and private equity investors—are applying our forecasts and playbooks to prioritize capital deployment, structure option-value preserving partnerships, and accelerate regulatory submissions timed for 2026 advisory meetings. The study is particularly useful for teams that need to reconcile short-term operational constraints with medium-term platform upside.

RNA therapeutics and vaccines will remain a top strategic bet for life-science executives in 2026, but success will hinge on hard choices: where to invest in capacity, which partnerships to pursue, and how aggressively to pursue differentiated delivery technologies. PW Consulting's report equips decision-makers with the market sizing, scenarios, and executable playbooks needed to convert platform promise into commercial reality.

To access the full segmentation, downloadable financial model, and the complete set of operational playbooks and company profiles, visit our report page. The preview you have read is intentionally selective—our detailed segment-level analytics and client-ready tools are available exclusively through the full report subscription.

For detailed analysis of this topic, please visit the official page:Rna Therapeutics And Vaccines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com