Organic Follow-Up Formula Market 2026–2034: Investment Opportunities and Risk Assessment

Home |

2026-04-30 13:13:51

As healthcare systems, security operators, and industrial users accelerate their transition from analog radiography to full digital imaging chains, the flat panel X‑ray detector (FPD) market has entered a phase of steady, structurally driven growth. PW Consulting’s latest market research synthesizes five years of historical performance with a 2026–2032 forecast horizon to deliver a practical roadmap for corporate decision‑makers. Our analysis shows the global market expanding at a compound annual growth rate (CAGR) of 5.6% through 2032, reflecting durable demand for both replacement and greenfield deployments across stationary, mobile and specialized imaging platforms.

Flat Panel X Ray Detectors Market

Recovery and momentum: After a post‑pandemic rebound period, the global FPD market moved from approximately USD 2.45 billion in 2020 to about USD 3.20 billion in 2025. Under current trajectories, PW Consulting projects the market to exceed USD 4.68 billion by 2032.

Flat Panel X Ray Detectors Market

Moderate concentration: Competitive intensity is meaningful but not prohibitive — the largest three vendors account for roughly 42.5% of market revenue, while the top five capture about 58.8%. That structure creates room for both scale players and focused challengers to capture share through technology, channel specialization or cost leadership.

Flat Panel X Ray Detectors Market

Price architecture: Unit pricing remains tiered. Entry‑level tethered detectors trade at substantially lower price points than premium wireless, glassless systems; typical panel prices in the market range from roughly USD 15K–20K at the low end to USD 26K–50K for high‑end wireless models, depending on form factor and technology choices.

Capital allocation: The mid‑single digit CAGR suggests predictable top‑line expansion but increasing competitive pressure on margins. Capital investments should prioritize modular platforms and scalable manufacturing rather than single‑product, capital‑intensive bets.

Product portfolio strategy: OEMs and system integrators must balance two imperatives — continuing to offer cost‑effective tethered detectors for price‑sensitive segments, while aggressively developing wireless, glassless and IGZO/CMOS‑based options for premium clinical and interventional use cases that demand higher pixel density and workflow flexibility.

Regulatory planning as gatekeeper: FPDs used in stationary and mobile X‑ray systems are regulated in major markets under Class II pathways (e.g., product code MQB per U.S. FDA), and there is growing scrutiny around performance standards for C‑arm and mobile systems. Regulatory lead time must be a formal component of product launch timelines and partner selection.

Prioritize hybrid roadmaps: Invest in platforms that can host both a‑Si and next‑gen sensor tiles (IGZO / CMOS) on a shared electronics backbone. This hedges technology risk while enabling rapid upgrades as clinical demand shifts toward higher resolution and dose efficiency.

Differentiate on software and workflow: As module hardware commoditizes, imaging post‑processing, connectivity to RIS/PACS, and embedded AI for quality checks and dose optimization will be decisive. Companies that package detectors with compelling software value capture higher aftermarket spend and stickier customer relationships.

Optimize manufacturing footprint: Supply chain interruptions and geopolitical considerations favor diversified production and qualified second‑source suppliers for critical wafers, scintillators and glass substrates. Design for assembly and test (DFx) can materially reduce time‑to‑volume and warranty costs.

Rethink go‑to‑market: Direct sales remain important in developed healthcare markets, but channel partnerships with system OEMs, diagnostic service providers and regional integrators unlock volume in emerging and non‑clinical applications (security, NDT). Tailored financing and refurbishment programs will expand addressable markets.

Use M&A to fill white space: Given moderate market concentration, targeted acquisitions — sensor IP, specialized CMOS fabs, or cloud imaging startups — can provide fast access to capabilities that are otherwise costly and time‑consuming to develop organically.

PW Consulting’s company profiles identify a bifurcated ecosystem: established imaging incumbents with deep clinical channel access, and nimble specialists focused on sensor innovation and cost competitiveness. Leading names include Varex Imaging, Canon Medical Systems, Fujifilm, Konica Minolta and Carestream — firms with broad detector portfolios, global installed bases and integrated X‑ray system strategies. Regional specialists and component innovators — including Vieworks, Rayence, Teledyne DALSA, Hamamatsu and Detection Technology — drive sensor and pixel‑level differentiation, while new or fast‑growing firms from China and South Korea increasingly compete on price and localized OEM supply.

Varex Imaging: an independent volume manufacturer with a wide array of wireless and tethered offerings and a large installed base. Strengths: scale manufacturing and connectivity to OEM system integrators.

Canon, Fujifilm, Konica Minolta, Carestream: these incumbents integrate detector technology into broader imaging systems and leverage installed maintenance networks as a competitive moat.

Sensor and semiconductor specialists (Teledyne DALSA, Hamamatsu, Detection Technology): focus on high‑sensitivity tiles, pixel innovations and niche high‑definition applications where image performance commands a premium.

Regional challengers and OEM suppliers (iRay, DRTECH, Vieworks, Rayence): bring competitive cost structures, rapid regulatory filing cycles in export markets and aggressive channel plays in emerging regions.

Recent regulatory activity underscores how rapidly the competitive map can evolve. Multiple 510(k) clearances through 2025–2026 — spanning new panel variants and embedded detectors in mobile C‑arms — reflect ongoing product refresh cycles and expanding clinical use cases. For companies competing internationally, careful tracking of cleared indications and consensus standards is essential to avoid downstream rework.

Sensor convergence: Expect continued coexistence of amorphous silicon, IGZO and CMOS sensors — each optimized for trade‑offs in cost, pixel pitch and power. High‑definition pixel sizes (sub‑100 µm) will be concentrated in niche diagnostic and interventional segments, while larger pixel formats remain prevalent in general radiography and mobile systems.

Glassless and lightweight form factors: The premium tiers increasingly emphasize glassless construction to reduce weight and improve durability for wireless panels used in mobile radiography and veterinary applications.

Embedded intelligence and interoperability: Detectors that natively support secure, standards‑based connectivity (DICOM, IHE) and on‑device quality assurance routines will capture disproportionate value in modern hospital procurement processes.

Regulatory classification and adherence to consensus standards for image matrix size, grid compatibility and safety remain non‑negotiable preconditions for market entry in regulated healthcare systems. In many cases, system OEMs will prefer cleared detector suppliers to reduce subsystem clearance risk. On reimbursement, while detector purchase is typically capital expenditure for hospitals, the downstream economics (throughput, reduced retakes, ancillary software services) increasingly influence procurement committees. PW Consulting recommends building total cost of ownership models into sales arguments rather than competing on upfront panel price alone.

The full PW Consulting Flat Panel X‑Ray Detectors Market report contains a suite of operational and strategic assets designed to be immediately actionable for 2026 planning cycles:

Market forecast model (2020–2032) with scenario‑based sensitivity for pricing, technology adoption rates, and replacement cycles;

Vendor scorecards covering product breadth, regulatory posture, channel strength and manufacturing footprint;

Commercial playbooks for OEMs and distributors, including recommended pricing tiers, financing constructs and aftermarket services templates;

M&A target shortlist and valuation benchmarks for sensor IP, assembly capacity, and software assets;

Operational checklist for product launches covering design-for-manufacture, regulatory filing timelines, and post‑market surveillance protocols.

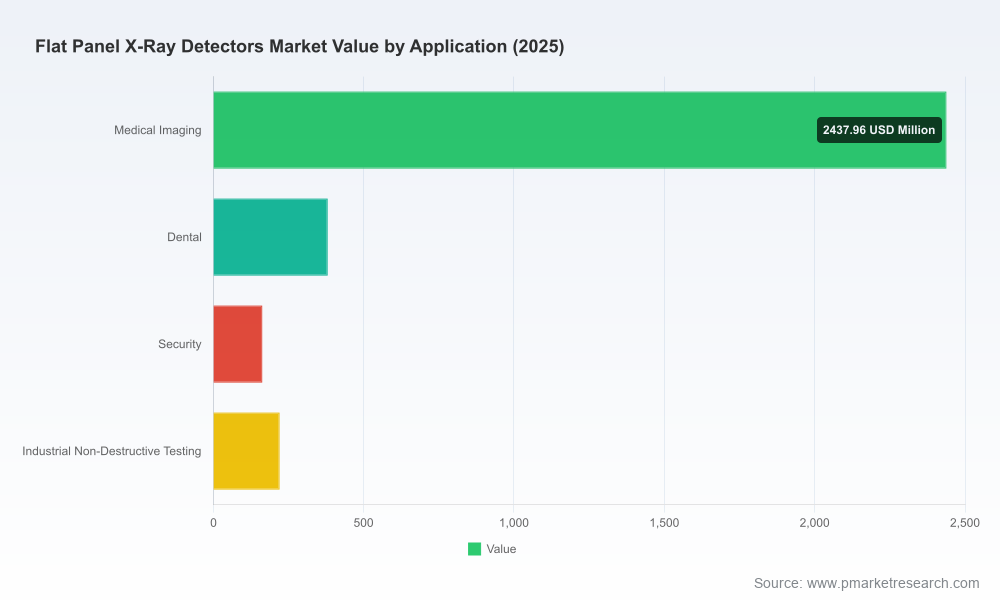

In keeping with our “preview” approach, we intentionally exclude granular segment revenue splits and regional percentage breakdowns from this bulletin. The full report includes complete segmentation detail, including regional, technology, and end‑use revenue decomposition, plus downloadable data tables and model access for in‑house scenario planning.

Boards and investors: use the market model to stress‑test investment theses for sensor fabs, software acquisitions, or distributor consolidations.

Product leaders: align roadmaps to hybrid sensor strategies, invest in embedded software and prioritize regulatory first‑to‑market plans where clinical differentiation exists.

Commercial teams: reframe conversations around lifecycle economics and AI‑enabled workflow gains rather than unit price alone; build service and refurbishment offerings to monetize installed bases.

Supply chain and operations: secure multi‑sourcing for scintillators and critical substrates, and qualify second‑tier assemblers to reduce single‑point risks.

The flat panel X‑ray detector market in 2026 is neither a runaway boom nor a static commodity space; it is a measured growth market defined by technological differentiation, regulatory rigor, and evolving buyer economics. PW Consulting’s analysis shows ample room for companies that can combine modular hardware roadmaps, compelling software value propositions and pragmatic regulatory execution. For those preparing 2026 budgets, the strategic choices made now — about manufacturing flexibility, technology bets, and go‑to‑market models — will determine who captures disproportionate value during the next growth cycle.

To access the full dataset, vendor profiles, and the interactive forecast model, contact PW Consulting or download the full Flat Panel X‑Ray Detectors Market report from our website. The downloadable report contains the granular segmentation and actionable financial models omitted from this briefing to preserve the executive preview experience.

For detailed analysis of this topic, please visit the official page:Flat Panel X Ray Detectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com