Healthcare and Laboratory Labels Market Registering a CAGR of 2.7% Through 2036 | Expansion of Healthcare and Diagnostic Services Supports Market Development

Networking |

2026-06-16 14:52:26

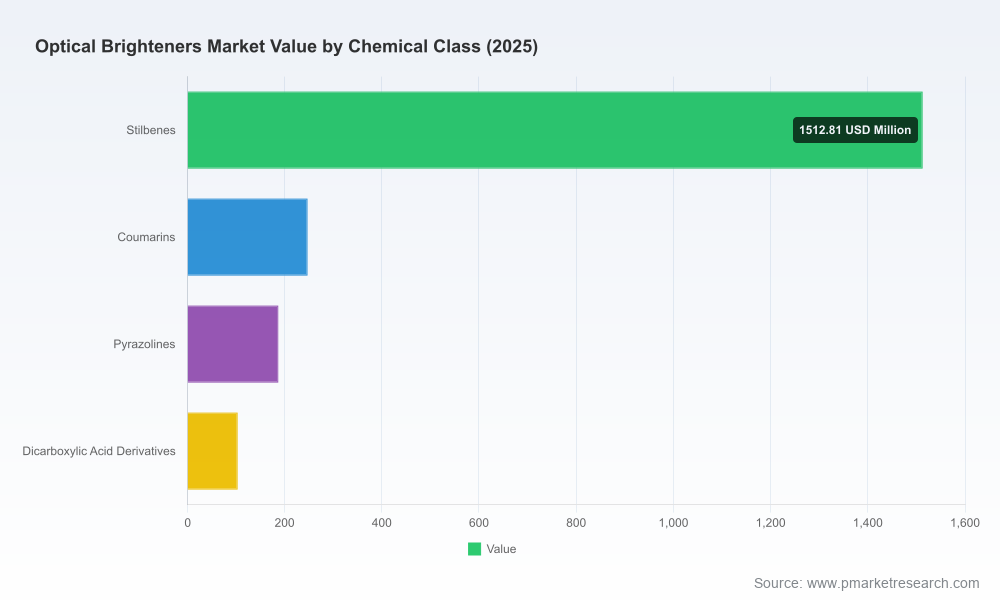

PW Consulting’s latest market study on Optical Brighteners delivers a forensic view of an industry at the intersection of commodity volatility, regulatory tightening and product premiumization. Our base-year analysis (2025) shows the global optical brighteners market surpassed USD 2.05 billion (USD Million basis), and under our central forecast the sector expands at a compound annual growth rate (CAGR) of 5.12% over 2026–2032, reaching a market size approaching USD 2.92 billion by the end of the forecast horizon. For executives planning 2026 resource allocation, sourcing strategies, or M&A activity, this report translates headline numbers into operational choices with immediate commercial impact.

Optical Brighteners Market

Actionable foresight, not just numbers: We convert macro trajectories into three prioritized decision streams—supply chain reconfiguration, product portfolio repositioning, and regulatory-proofing—so leadership teams can sequence investments across CapEx, R&D and commercial initiatives.

Optical Brighteners Market

Risk-to-return calibrated recommendations: Using scenario-driven sensitivity analysis, the report quantifies how feedstock price swings, tariff measures and regulatory shifts affect margins and payback timelines for typical brightener grades.

Optical Brighteners Market

Competitive playbook: The analysis synthesizes recent industry moves—capacity additions, asset transfers and product launches—into competitor positioning maps and negotiation levers for procurement and business development.

Regulation is now a primary demand shaper. European REACH amendments and ZDHC MRSL updates are accelerating reformulation away from legacy stilbene derivatives toward modified chemistries and alternative classes that balance performance with aquatic toxicity and persistence constraints. Companies that can demonstrate compliance via third-party eco-labels, and that maintain product dossiers to expedite approvals, will have a structural advantage.

Trade policy and antidumping measures are re-ordering competitive dynamics. Recent antidumping actions and tariff measures have increased the total landed cost profile for imports from certain sourcing geographies, prompting downstream formulators and major producers to re-evaluate supplier concentration and near-shore capacity.

Feedstock cost sensitivity. Optical brightener manufacture remains linked to petrochemical intermediates; crude oil and intermediate pricing cycles materially affect unit economics. Our cost-pass-through models show that volatility in key intermediates can compress margins within a single pricing cycle unless mitigated by contractual hedges or vertical integration.

Premiumization and sustainability-driven segmentation. End-users in home care, textiles and premium paper grades increasingly value functional performance combined with environmental credentials. This trend supports higher-margin specialty grades, but requires validated claims and consistent supply chains.

The competitive field blends global specialty chemical majors, regional commodity producers and niche formulators. Recent developments highlight strategic directions that will define winners and laggards in 2026:

Catexel’s acquisition of BASF’s optical brightening agent business, including the Monthey production site (closed in early 2026), signals consolidation at the premium detergent ingredient end of the market and underscores the strategic value of integrated manufacturing footprints and experienced technical teams.

Archroma’s market-facing activity—showcasing ULTRAPHOR® and Leucophor® offerings—illustrates a deliberate expansion from textile and paper heritage into home and personal care, leveraging sustainability-compliant R&D as a market-entry vector.

Huntsman’s commissioning of an E-GRADE purification and packaging unit underscores the premium placed on high-purity grades for regulated applications; investments in downstream purification are a durable differentiator for suppliers targeting quality-sensitive end-markets.

Regional supply players—from established European specialties to large-scale Asian exporters and Indian cost-competitive manufacturers—continue to occupy distinct strategic niches. Buyers should treat supplier selection as a capability match: high-purity, eco-labeled finishes for regulated markets versus cost-competitive grades for price-sensitive volume channels.

Procurement: Rebalance supplier portfolios to reduce country-concentration risk and secure access to ZDHC-compliant grades. Short-term tactical actions include layering staggered contracts, index-linked pricing clauses tied to key intermediates, and conversion of spot exposure into strategic tolling or capacity reservation agreements.

R&D and product strategy: Prioritize modified stilbenes and alternative chemistries (such as select coumarins and pyrazoline derivatives) that meet both performance and regulatory criteria. Equally important is investment in formulation science that demonstrates equivalence or improvement in whiteness, durability and wash-fastness under constraints imposed by new regulatory lists.

M&A and partnerships: Asset plays—whether acquiring production sites, purification units, or specialty portfolios—remain attractive for firms seeking control over key grades. The recent Monthey transaction provides a template: acquiring a focused asset plus experienced personnel can accelerate market entry while preserving technical continuity.

Perform a two-tier supplier stress test: 1) capability and compliance audit for all preferred suppliers; 2) live scenario test for substitution and logistics disruption to validate switchability within 60–90 days.

Implement a raw-material volatility hedge program tailored to intermediate exposure, combining financial hedges with operational levers (e.g., buffer inventory of critical intermediates, alternate chemistries with different feedstock mixes).

Re-scope product portfolios into three buckets—regulated premium, sustainable mainstream, cost-competitive basic—and align manufacturing/marketing KPIs to those buckets to avoid margin dilution from one-size-fits-all strategies.

Invest in compliance intelligence: maintain live regulatory trackers for REACH, MRSL and key tariff regimes; integrate alerts into commercial contract negotiation workflows to accelerate re-pricing or reformulation when lists change.

Design a rapid commercialization pathway for eco-labelled grades that bundles technical validation data, pilot batches, and market pilot agreements with top customers—this reduces time-to-revenue and creates defensible switch costs.

Our Optical Brighteners Market report is intentionally practical. Beyond top-line forecasting, the deliverables include:

A multi-scenario market model with sensitivity levers for feedstock, tariff and regulatory trajectories to quantify upside/downside impacts on revenue and margins;

Supplier benchmarking templates that score capabilities across quality, compliance, capacity, and logistical resilience;

Regulatory impact matrices and reformulation decision trees that link chemical classes to likely compliance timelines and commercial implications;

M&A playbooks and due-diligence checklists tailored to brightener assets, including technical audit templates for purification units and environmental compliance risk assessments;

Commercial negotiation toolkits with sample contract clauses addressing price adjustment, force majeure for regulatory change, and performance warranties tied to eco-label claims.

Calendar 2026 is a pivot year. The intersecting pressures of regulatory tightening, trade policy shifts, and selective capacity investments will create asymmetric opportunities: firms that move early to secure compliant supply lines, invest in high-purity manufacturing capabilities, and differentiate through verified sustainability credentials will capture premium segments and insulate margins. Conversely, firms that postpone strategic responses risk margin compression and loss of customer access as formulators increasingly substitute to compliant alternatives.

Our study is designed as a decision-ready asset for boards, commercial leaders, and corporate development teams. It combines the high-level market trajectory—including the 2025 base, the 5.12% CAGR through 2032 and projected end-horizon sizing—with the operational granularity required to act in 2026. For organizations that need bespoke scenario runs, supplier scorecards, or a workshop to convert these insights into a 100-day plan, PW Consulting offers tailored briefings and implementation support.

To access the full dataset, segmented analysis, and proprietary supplier scorecards (including the granular regional and application-level metrics omitted here), please consult PW Consulting’s Optical Brighteners Market report landing page or contact our industry team for a briefing and tailored executive summary.

For detailed analysis of this topic, please visit the official page:Optical Brighteners Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com