Poultry Feed Market Size, Share, Trends, Industry Analysis and Forecast by 2029

Other |

2026-05-27 11:40:49

PW Consulting today publishes an executive market brief that synthesizes our comprehensive Absorbable Cranial Clamp Market research (base year 2025, forecast 2026–2032). The report translates granular clinical, regulatory and commercial intelligence into decision-grade recommendations for medtech executives, investors and hospital system leaders who must set strategy in 2026. At a macro level, the market reached approximately USD 385.0 Million (2025) and is projected to expand to roughly USD 406.97 Million in 2026, tracking at a compound annual growth rate (CAGR) of 5.8% through our forecast window and reaching about USD 571.3 Million by 2032. These headline figures frame a market that is growing steadily but remains strategically nuanced — and highly sensitive to clinical evidence, material science advances, and regulatory trajectories.

Absorbable Cranial Clamp Market

Acceleration point for commercialization: The market’s mid-single-digit CAGR signals continued adoption, but pockets of rapid uptake are opening where new materials and clinical evidence reduce surgeon friction. Players making 2026 investment decisions must prioritize the subsegments and evidence pathways that convert early adopters into mainstream users.

Absorbable Cranial Clamp Market

Consolidation and competitive dynamics: Industry concentration is materially meaningful — our analysis shows a CR3 of 52.5% and a CR5 of 68.2% — indicating incumbent strength but ample room for well-funded challengers with differentiated clinical data or cost-to-serve advantages.

Absorbable Cranial Clamp Market

Regulatory and reimbursement inflection points: Recent device clearances and trial results are reshaping go-to-market timelines. Companies that synchronize regulatory filings, clinical trials and payer engagement in 2026 will secure durable commercial advantage.

Growth is steady but heterogeneous: While the market expands at ~5.8% CAGR, adoption is driven by a mix of clinical need (craniotomy fixation and trauma repair), material performance, and hospital procurement dynamics.

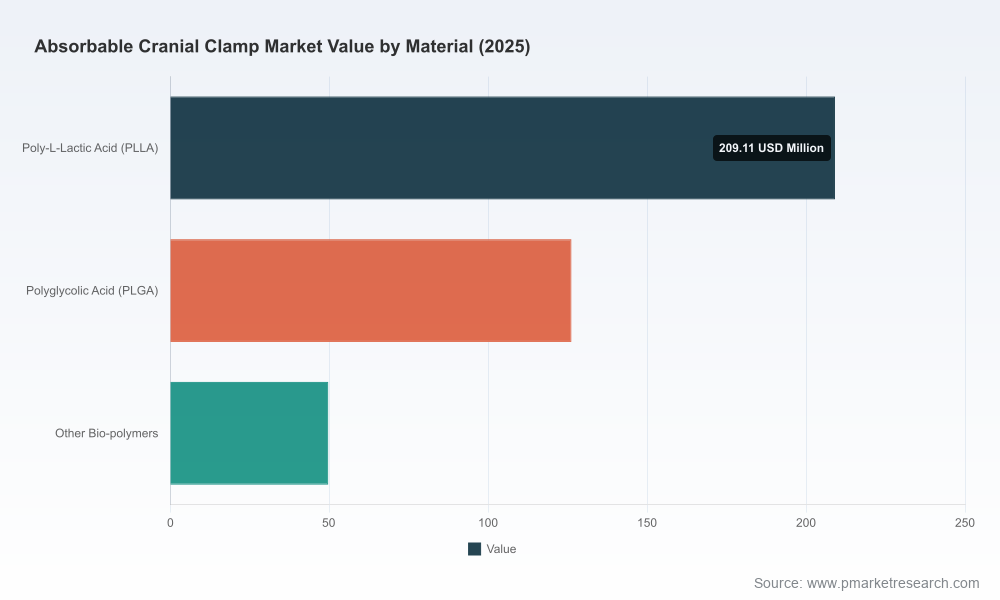

Materials matter strategically: Poly-L-lactic acid (PLLA) and poly(l-lactide-co-glycolide) (PLGA) remain the dominant chemistries in clinical use. Their differing degradation profiles and strength-retention timelines create meaningful trade-offs for product design, labeling claims and surgeon preference. For example, established absorbable systems are documented to retain the majority of initial strength through the key early healing window, with full metabolism over multiple years — an attribute that influences both clinical acceptance and product positioning.

Clinical evidence is the lever: Recent multicenter results and regulatory clearances (including 510(k) pathways) have accelerated entry for new devices. High-quality comparative trials that demonstrate parity or superiority in stability, bone healing and complication rates are proving decisive in OR adoption.

Commercial moats are being redefined: Traditional device incumbency remains valuable but is being challenged by manufacturers that combine strong clinical data, competitive cost structures, and integrated commercialization models (training, instrumentation, and O.R. workflow support).

Our report profiles the full competitive set, but several narratives merit advance mention because they will shape 2026 strategy.

B. Braun Melsungen AG (Aesculap): As an established player, their CranioFix Absorbable system exemplifies an instrument-free, polyester-based approach that balances intraoperative ease and a multi-month strength retention profile. Incumbency, channel relationships, and a well-known brand give them pricing and distribution advantages in many hospital systems.

Johnson & Johnson (DePuy Synthes): DePuy’s RAPIDSORB line leverages a PLGA copolymer formulation designed to provide predictable stability through the critical early healing window. Their global orthopedics and neuro portfolios enable cross-selling and strong KOL networks — a commercial asset that challengers must neutralize if they seek share.

MedArt Technology Co., Ltd.: A fast-moving challenger from China, MedArt has combined material selection and focused clinical programs to accelerate market access. Notably, a multicenter trial reported non-inferior mechanical stability and favorable bone-healing endpoints versus an established competitor, and MedArt’s device secured 510(k) clearance as a Class II device in recent years — milestones that materially alter their go-to-market calculus.

Taken together, these trajectories highlight a market where product differentiation is achieved not only by incremental device improvements but through orchestration of evidence generation, regulatory sequencing and distribution execution.

The PW Consulting report is crafted as a working tool for leadership teams. Key practical deliverables include:

Top-down and bottom-up market sizing with transparent methodology and sensitivity ranges (historical 2020–2025 and forward 2026–2032).

Scenario-based revenue models (base, upside, downside) with downloadable Excel modules to run custom assumptions.

Detailed competitor profiles and strategic maps that include technology positioning, distribution channels, and near-term pipeline events.

Regulatory and reimbursement playbooks tailored to major markets and common device classifications, including 510(k) strategies and clinical evidence thresholds.

Commercial go-to-market templates (KOL engagement, hospital contracting, training programs, instrument bundles) and pricing sensitivity analyses.

M&A and partnership scorecards that identify target archetypes, valuation frameworks, and integration risks.

Clinical evidence blueprints — trial designs, endpoints, and timelines that unlock adoption in neurosurgery and trauma centers.

We deliberately withhold granular regional and application-level splits from this press release to preserve the strategic exclusivity of the full report. Those detailed breakdowns (by region, material type, and clinical application) are included in the report and in the downloadable models.

Prioritize evidence that changes behavior: Invest in at least one multicenter comparative study that targets both mechanical stability and bone-healing endpoints — trials that show superiority or clear non-inferiority with secondary benefits (e.g., better bone consolidation) shorten the adoption curve.

Choose material strategy by value proposition: If your go-to-market is surgeon convenience and long-term biointegration, optimize for PLLA-like profiles; if rapid early stability and quicker resorption are your message, consider PLGA blends. Each choice alters labeling, manufacturing and follow-on claims.

Sequence regulatory filings to unlock commercial partnerships: Stagger submissions to prioritize markets where reimbursement and hospital purchasing pathways are fastest to convert.

Build surgeon-facing services: Training, simulation-based onboarding and instrument simplification reduce friction for OR adoption and increase switching costs.

Adopt a targeted geographic rollout: Use a data-driven approach to prioritize health systems and regions with high neurosurgical procedure volumes and receptive procurement practices. (Detailed regional prioritization maps are included in the report.)

Prepare for consolidation: With CR5 near 70% territory, be ready with an M&A playbook — both as an acquirer to access technology and channels or as a defendable target to monetize IP and evidence assets.

Stress-test pricing and margin scenarios across manufacturing scale curves: Absorbable devices are sensitive to raw material costs and yield; manufacturing investments and supplier contracts executed in 2026 will materially affect margin in 2027–2028.

Boardrooms and investment committees will face trade-offs between accelerating clinical programs and allocating capital to commercial scale-up. Use our report to:

Build a three- to five-year roadmap that links product claims to clinical trial milestones and reimbursement timelines.

Create an investment decision gate in 2026 tied to predefined evidence and regulatory triggers — safeguarding capital while preserving optionality.

Design integration checklists for M&A targets that focus on regulatory history, clinical datasets, and manufacturing quality systems.

PW Consulting combines primary interviews with surgeons, procurement officers and regulatory specialists, quantitative demand modeling and a proprietary deal and trial-tracking engine. Our approach balances transparency (we document assumptions and sensitivities) with practical actionability (downloadable tools and playbooks you can use inside 60 days).

This release is a high-value preview designed to enable rapid executive discussion. The full Absorbable Cranial Clamp Market report contains the detailed regional and application-level splits, company revenue estimates, full financial models and the complete set of strategic templates referenced above. For teams preparing 2026 budgets and strategic plans, that level of granularity is often a decisive differentiator.

To obtain the full report and the accompanying Excel models, visit the PW Consulting research portal or contact your account lead. Our team stands ready to run customized scenario workshops and to help translate findings into a 90-day implementation plan tailored to your organization.

For detailed analysis of this topic, please visit the official page:Absorbable Cranial Clamp Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com