Core Texas Driving Innovation and Business Growth Forward

Other |

2026-03-18 19:53:45

As capital allocation cycles reset in 2026, senior leaders in industrial equipment, materials processing, semiconductor manufacturing, and precision medical device production must reassess technology bets. Our latest PW Consulting market study on Solid State Lasers for Laser Processing Equipment (base year 2025, historical coverage 2020–2025, forecast 2026–2032, revenues reported in USD Million) shows a continuation of strong, above‑market industrial optics demand. The market reached approximately USD 3,142.5 Million in 2025 and—under our mid‑case forecast—expands at a 7.72% CAGR to exceed USD 5,200 Million by 2032. This growth trajectory confirms that solid‑state laser platforms will remain a core enabling technology for precision processing across multiple high-value end markets.

Solid State Lasers For Laser Processing Equipment Market

Technology convergence: Ultrafast and high‑brightness fiber/disk architectures are moving from laboratory advantage to industrial reliability, prompting procurement cycles for replacement and new capacity.

Solid State Lasers For Laser Processing Equipment Market

Regulatory and export landscape: Recent tightening of dual‑use export controls for high‑power systems, combined with standardized machine safety requirements, means vendors and buyers must embed compliance into product roadmaps and supply agreements.

Solid State Lasers For Laser Processing Equipment Market

Supply volatility: Doping materials and rare‑earth feedstocks (notably neodymium and ytterbium) are showing pronounced price and availability swings, creating operational and margin risk across OEMs and integrators.

Bankable market sizing and scenario forecasts (2026–2032) calibrated to conservative, base, and upside economic paths to support capex planning and portfolio prioritization.

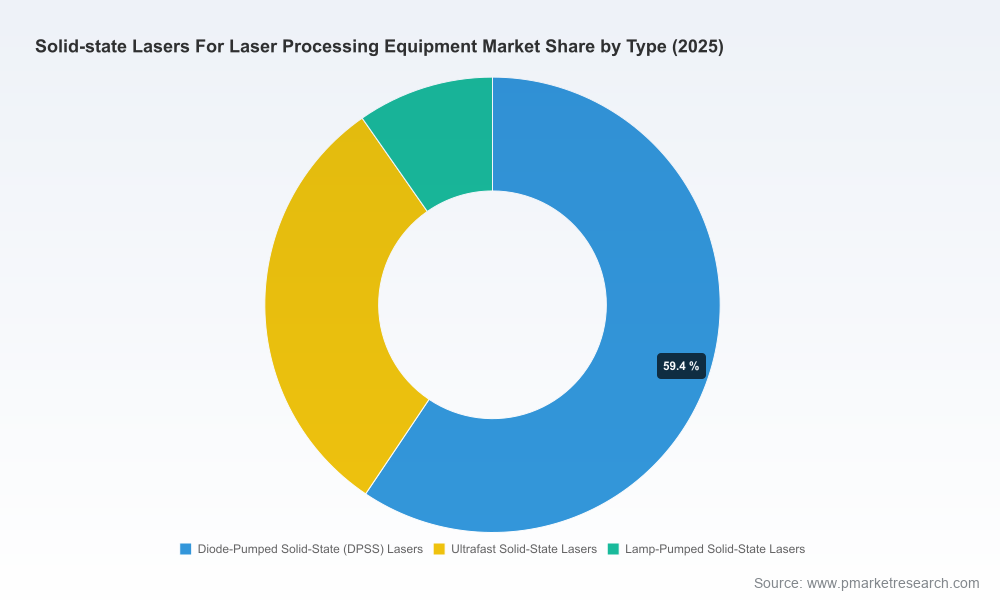

Technology deep dives that map laser architectures (e.g., diode‑pumped, ultrafast, lamp‑pumped) to specific processing outcomes, throughput envelopes, and total cost of ownership (TCO) models.

Supplier benchmarking and capability scorecards — performance, reliability, service footprint, and compliance posture — designed for procurement RFPs.

Use‑case ROI playbooks for high‑value applications (precision micromachining, semiconductor patterning, medical device manufacturing), including sensitivity analyses around cycle time, yield, and material substitution.

Supply‑chain risk matrix with geo‑dependency mapping, inventory strategies, and hedging scenarios for rare earths and critical optical components.

M&A screening tool and integration checklist that highlight target profiles, valuation levers, and integration risks specific to laser subsystems and module suppliers.

Regulatory impact modeling that quantifies potential cost and time‑to‑market implications of IEC/ISO safety rules and export control thresholds for high‑power systems.

Demand for solid‑state laser processing equipment has demonstrated resilient expansion throughout the five‑year historical window and into our forecast horizon. The market’s mid‑cycle CAGR of 7.72% reflects both steady end‑market adoption and elevated replacement cycles as manufacturers pursue higher precision, throughput and lower operating cost. Competitive dynamics are moderately consolidated: the top three players control a meaningful share of the installed base while the top five command a clear majority, underscoring a market where scale, service network, and technology IP materially affect commercial outcomes.

Standards and machine safety: Compliance with IEC 60825‑1 classification and ISO 11553 machine safety frameworks is now prerequisite for enterprise procurement. Buyers should require supplier proof points — third‑party certifications, integrated interlocks, and documented safety‑by‑design processes — as part of contract acceptance criteria.

Export and trade controls: Systems above certain power thresholds face dual‑use scrutiny under international arrangements. Procurement and global sales teams must assume at least a 90–120 day additional lead time for export licensing and incorporate export‑control clauses into contracts to avoid revenue leakage.

Raw‑material risk: Neodymium and ytterbium supply volatility translates into component cost swings (historic annual price variances have ranged broadly). Manufacturers should pursue multi‑sourcing, long‑term offtakes, and design choices that de‑risk dependence on single dopants where feasible.

Technology migration: The industrialization of ultrafast and diode‑pumped platforms favors suppliers that can demonstrate both process outcomes and serviceability in factory environments. Buyers must align technical KPIs (pulse control, beam quality, uptime) with application economics rather than headline power figures alone.

The market’s competitive map combines long‑established industrial OEMs and highly specialized photonics firms. Our analysis focuses on capability clusters that matter to procurement, integration partners, and strategic investors.

Trumpf (Ditzingen, Germany) — A leading industrial player with mature disk and rod designs, Trumpf’s portfolio emphasizes high‑power, high‑duty industrial systems for cutting, welding, and micromachining. Recent product introductions (notably ultrafast models with pulse‑on‑demand) demonstrate an aggressive push to capture higher‑value microprocessing and automated production cell opportunities.

Coherent (Saxonburg, PA, USA) — Broad product ranges spanning high‑power and picosecond platforms position Coherent to serve both heavy industrial and precision microfabrication segments. Their newer high‑power picosecond platforms are engineered for cycle time reduction in micromachining and additively‑enabled workflows.

IPG Photonics (Marlborough, MA, USA) — IPG’s expertise in ytterbium‑doped fiber approaches yields high brightness and modularity advantageous for integration into automation lines and additive systems. Their focus on manufacturable fiber modules aligns with customers prioritizing uptime and maintainability.

Lumibird (formerly Quantel, Lannion, France) — Known for Q‑switched Nd:YAG systems, Lumibird’s product set is attractive for marking, engraving, and certain ablation tasks. Their strengths include pulse energy control and field service in high‑mix manufacturing environments.

Spectra‑Physics (MKS Instruments, Santa Clara, CA, USA) — A leader in ultrafast platforms, their offerings target microstructuring and surface engineering where temporal control is a competitive differentiator.

ROFIN‑SINAR (Coherent subsidiary, Hamburg, Germany) — Specializes in pulsed solid‑state solutions and brings industrial robustness for drilling and precision cutting applications. As part of Coherent, integration synergies in distribution and global service expand their addressable market.

Each of these firms is actively iterating product roadmaps, as evidenced by recent product launches and trade‑show demonstrations through 2024–2025. For buyers, supplier selection should weigh not only installed performance but also service ecosystem, roadmap alignment to application needs, and exposure to raw‑material and export‑control risk.

For OEMs and system integrators: Prioritize modular architectures that allow field upgrades of key modules (pump diodes, control electronics, pulse shaping) to extend asset lifecycles and capture aftermarket revenue.

For end users (manufacturers and labs): Adopt a TCO procurement framework that factors in service cadence, mean time to repair, and energy efficiency; require transparent supply‑chain traceability for dopants and critical optics.

For investors and PE sponsors: Target bolt‑on acquisitions that deepen service networks or provide complementary module IP (e.g., beam delivery, process control software) rather than horizontal consolidation alone.

For procurement and legal teams: Embed export‑control and certification clauses into purchase orders and use letter‑of‑credit structures or escrow for higher‑risk cross‑border transactions.

For R&D teams: Balance short‑term yield gains from ultrafast adoption with medium‑term investments in materials substitution and diode efficiency to hedge raw‑material exposure.

Regulatory shocks — accelerated export control rollouts or new classification thresholds that change commercial viability for certain high‑power designs.

Material supply disruption — mine closures, geopolitical restrictions, or longer‑term substitution delays that lead to sustained price inflations.

Technology dislocation — emergence of alternative processing platforms or marked improvements in competing laser chemistries that materially change application economics.

Our report is structured as an actionable decision toolkit rather than a descriptive summary. It integrates financial modeling, supplier scoring, regulatory and export-control playbooks, and hands‑on ROI calculators to enable procurement, product, and corporate development teams to move from insight to contract language and board‑level investment recommendations within weeks.

To preserve the strategic advantage for subscribers, this briefing intentionally omits the granular regional and application level tables, supplier scorecards, and the downloadable financial model that underpins our forecasts. These proprietary deliverables — including segmented demand curves, supplier operating metrics, and scenario‑specific TCO calculators — are available in the full PW Consulting report.

If your 2026 planning cycle requires a defensible view on technology selection, supply‑chain resilience, or M&A screening in solid‑state laser processing, PW Consulting’s full study provides the detailed inputs, contract templates, and scenario tools to accelerate decisioning. Contact our advisory team to obtain the full dataset, model access, and a tailored workshop to convert insights into a 90‑day execution plan.

For detailed analysis of this topic, please visit the official page:Solid State Lasers For Laser Processing Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com