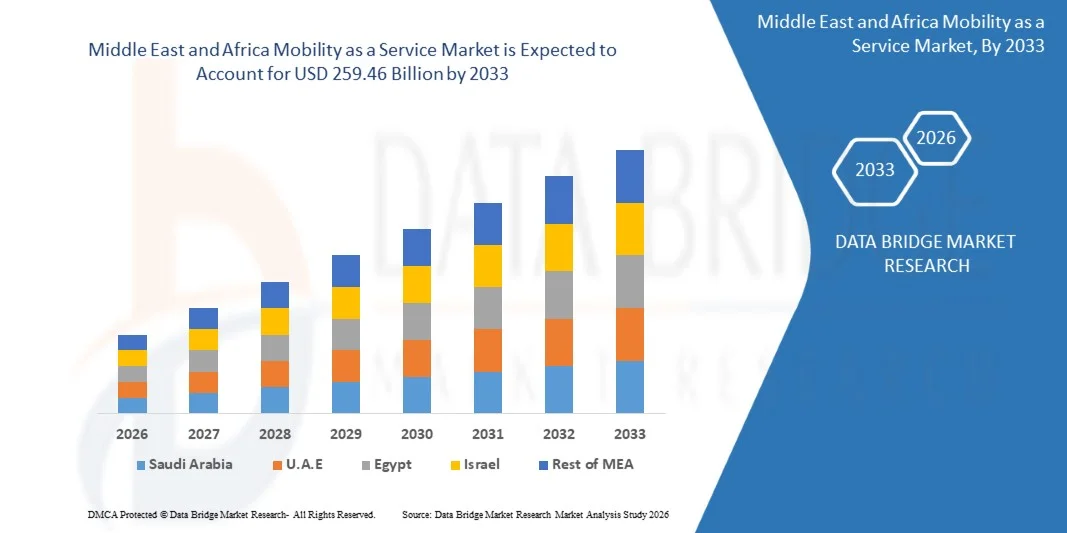

Middle East and Africa Mobility as a Service Market Industry Size, Share, and Outlook Forecast by 2033

Other |

2026-06-25 09:25:44

PW Consulting today publishes an executive preview of our new market research report, Valve Solenoids for Pneumatics Market — a pragmatic, decision-focused study designed to support corporate strategy and capital allocation through 2032. Built on rigorous historical analysis (2020–2025) and a detailed forecast horizon (2026–2032), this report translates market dynamics into actionable choices for product teams, procurement, business development, and M&A leaders preparing for 2026 and beyond.

Valve Solenoids For Pneumatics Market

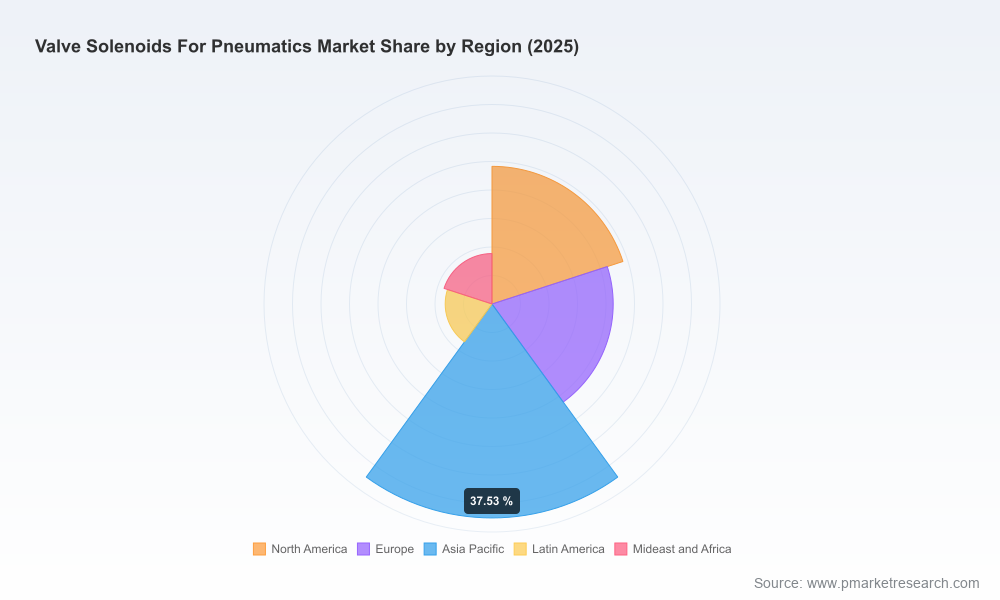

The solenoid valves market for pneumatic systems exhibited steady expansion during the historical period, reaching an estimated USD 2,345.6 Million in 2025. Our model projects continued growth through the forecast window, with the market expanding to roughly USD 3,421.95 Million by 2032 at a compound annual growth rate (CAGR) of approximately 5.45% (2026–2032). This pace reflects a convergence of secular demand drivers — ongoing automation of discrete manufacturing, renewed investment in energy- and materials-efficient designs, and safety-driven upgrades in process industries.

Valve Solenoids For Pneumatics Market

Concentration metrics indicate a market where leading vendors exert meaningful influence but do not dominate outright — a structure that creates opportunities for nimble specialists, component innovators, and regional challengers to capture pockets of value by executing targeted strategies.

Valve Solenoids For Pneumatics Market

Beyond topline sizing and trend graphics, the report is structured to support execution. Core deliverables include:

We intentionally present this preview as a strategic trailer: the report equips leaders with the models, templates, and vendor intelligence necessary to act in 2026, while core subsegment figures and granular vendor share tables are reserved for the full report to preserve competitive advantage and drive direct engagement.

The market remains populated by a mix of global industrial OEMs, specialized component manufacturers, and niche innovators. Our analysis highlights several archetypes and representative vendors, each influencing the market in distinct ways:

Representative companies profiled in the report (with objective summaries of strengths and strategic posture) include global leaders and specialist players that collectively shape product expectations and supply dynamics. Each profile summarizes headquarters, product focus, competitive differentiation and recent strategic moves that matter for 2026 planning.

These moves reflect three cross-cutting strategic themes: miniaturization without sacrifice of flow, embedded intelligence for predictive maintenance, and compliance-ready designs for safety-critical applications. Firms that align R&D and go-to-market resources along these themes materially improve their 2026 competitive position.

Standards such as IEC 61511 and ISA/IEC 62443 are increasingly influential in procurement specifications for safety instrumented systems and industrial control networks. ISO 5599/1 remains the de‑facto reference for interchangeability in directional control valves. Practically, this means that product teams must incorporate functional-safety architectures, diagnostic interfaces, and cybersecurity considerations into product roadmaps and release criteria.

On materials, stainless steel bodies and high-performance seal compounds are becoming standard for valves operating in harsh environments. Design trade-offs between cost, corrosion resistance, and manufacturability will shape supplier selection and total cost of ownership calculations.

This preview is designed to help executive teams quickly align on strategic priorities for 2026: product roadmap trade-offs, procurement risk mitigation, M&A screening criteria, and regulatory compliance sequencing. For organizations that require granular market segmentation, vendor share matrices, and downloadable forecast models (including scenario toggles and sensitivity analysis), the full PW Consulting report contains the comprehensive datasets, appendices, and implementation templates needed to operationalize strategy.

PW Consulting’s Valve Solenoids for Pneumatics Market report is tailored for executives, product managers, procurement leads, and M&A teams seeking defensible, implementable intelligence. The full report includes proprietary vendor benchmarking, a downloadable forecast model for internal use, and client workshops to translate findings into a 12–24 month action plan.

To explore the full findings, licensing options, or to schedule a briefing with our senior analysts, visit our report page or contact your PW Consulting representative. The preview above reflects the high-level conclusions and strategic implications; detailed, segment-level data and company share tables are available in the comprehensive report.

For detailed analysis of this topic, please visit the official page:Valve Solenoids For Pneumatics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com