Custom Oil Packaging - Protecting Quality While Elevating Your Brand

Other |

2026-06-30 14:31:15

PW Consulting today releases a strategic preview of our forthcoming Cnf Software Market research, designed to equip enterprise leaders, telco operators, cloud service providers, and technology investors with the decision-grade context they need for 2026. Built on a rigorous base year of 2025 (and a calibrated historical series from 2020–2025), our model forecasts continued rapid expansion through 2032 at a compound annual growth rate (CAGR) of 22.4%. The market scale moves from a strong multi‑billion‑dollar base in 2025 into a multi‑ten‑billion opportunity by the end of the forecast window — a trajectory that requires purposeful strategy, not ad‑hoc procurement.

Cnf Software Market

Strategic timing: 2026 is the inflection year when CNF (Cloud‑Native Network Function) projects transition from proof‑of‑concepts to broad operational deployments across edge and core domains. The market momentum we model underpins multi‑year investment decisions — selecting the right orchestration, security, and lifecycle platforms now materially affects total cost of ownership and speed to revenue.

Cnf Software Market

Competitive differentiation: Vendors and systems integrators that demonstrate telecom‑grade integrations with Kubernetes ecosystems, DPU acceleration, and validated partner stacks will capture disproportionate value. Our analysis surfaces the capabilities that correlate with customer win rates in 2026 and beyond.

Cnf Software Market

Risk calibration: Rapid growth masks operational risks — talent scarcity, regulatory alignment, and integration complexity. Our briefing details leading mitigation strategies that enterprises must adopt to avoid costly delays and interoperability deadlocks.

Base year and scope: The study uses 2025 as the reporting base year and evaluates historic dynamics from 2020 through 2025 to inform a scenario‑driven forecast for 2026–2032.

Growth outlook: A robust CAGR of 22.4% underpins the forecast through 2032, reflecting accelerated CNF adoption across 5G, edge computing, and cloud‑native transformation programs in service providers and enterprises.

Concentration: Market concentration is meaningful but not monopolistic — the combined share of the top three vendors sits below a majority threshold, while the top five approach a clear scale effect. This structure favors both incumbent scale plays and specialist innovators.

Our aim with the full PW Consulting Cnf Software Market report is operational utility. Readers will find a suite of actionable deliverables, including:

Decision frameworks — vendor selection scorecards tailored for operator use cases, procurement negotiation levers, and an enterprise adoption checklist for CNF migrations.

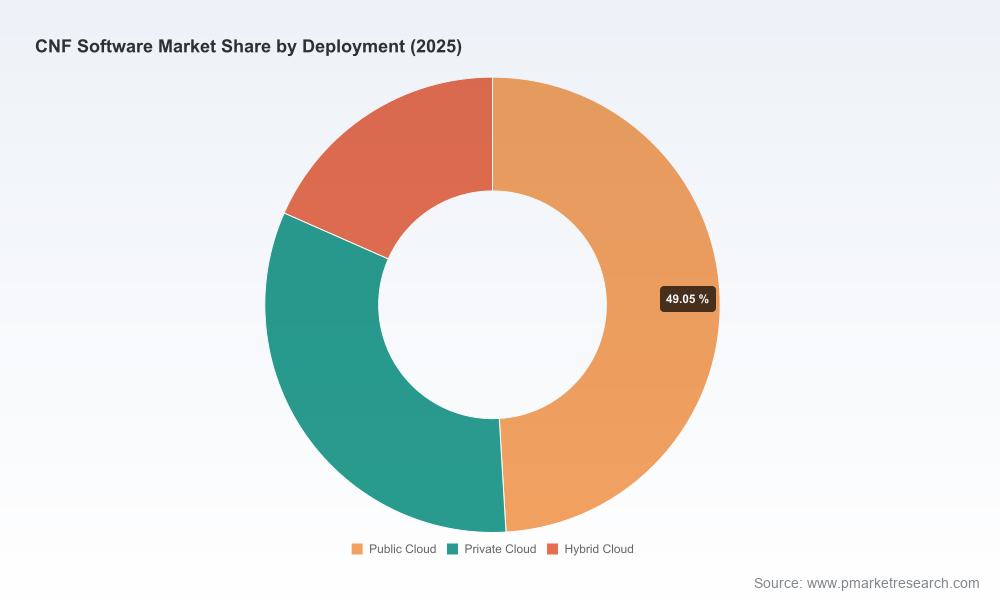

Deployment playbooks — validated runbooks for public, private, and hybrid cloud deployments that align with Kubernetes and ETSI NFV MANO patterns, including failure‑mode analysis and recovery timelines.

TCO & ROI models — configurable templates that translate vendor feature sets, orchestration choices, and operational staffing scenarios into five‑year economics.

Integration blueprints — recommended architectures for combining CNF orchestration, lifecycle management, observability, and security layers while minimizing latency and operational overhead.

Vendor benchmark dossiers — qualitative and comparative assessments of strategic position, product maturity, partner ecosystem, and roadmap alignment (note: core proprietary scoring and segment‑level allocations are reserved for subscribers).

The CNF ecosystem is dynamic. Our synthesis of vendor strategies and recent product developments highlights several patterns that will influence vendor selection and partnership decisions in 2026:

Nokia (Espoo, Finland): Continues to push disaggregated CNFs for packet core and IMS optimized for Kubernetes. Nokia’s contributions to cloud‑native toolchains and standards engagement make it a strong candidate for operators seeking vendor‑validated CNF suites with deep telecom pedigree.

Ericsson (Stockholm, Sweden): The expansion of third‑party CNF certification programs signals a deliberate move toward open ecosystems. Operators prioritizing multi‑vendor flexibility and certified interoperability should weigh Ericsson’s CNIS‑centered approach.

F5 (Seattle, USA): Advances in BIG‑IP Next CNF lines — especially around DPU acceleration, MPLS/PE support, and tighter integration with Kubernetes platforms — position F5 as a performance and edge‑security leader where data‑plane efficiency matters.

Cisco (San Jose, USA): Cisco’s containerized mobile and broadband CNFs bring broad systems integration capabilities and established networking expertise, appealing to operators pursuing end‑to‑end vendor consolidation.

Ribbon Communications (Plano, USA): Specialization in session border control, policy/routing, and IMS CNFs makes Ribbon an attractive partner for communications service providers focused on session resilience and legacy interworking.

Titan.ium Platform (Canada): As a specialist CNF provider with a microservices DNA, Titan.ium’s offer targets operators seeking lightweight, developer‑friendly CNFs for signaling, routing, and subscriber management in 5G contexts.

Red Hat (Raleigh, USA): While not a pure CNF vendor, Red Hat’s OpenShift remains a critical commercial Kubernetes substrate with partner validations that materially reduce deployment risk for CNF stacks from multiple OEMs.

Recent vendor activity reinforces these trends. For example, F5’s 2026 product iterations introduce DPU accelerated dataplane options and expanded protocol support, amplifying performance claims for edge deployments. Ericsson’s programmatic certification efforts lower integration friction for third‑party CNFs. Meanwhile, CNCF ecosystem growth continues to expand the developer base that will implement and operate these systems — a structural tailwind we quantify in the report.

Standardization & regulatory alignment: CNFs are being deployed within Kubernetes and ETSI NFV MANO frameworks, with Container Infrastructure Service Management (CISM) patterns increasingly dictating interoperability requirements. Operators must balance open‑source agility with telecom‑grade reliability and compliance needs.

Talent & labor market: The cloud‑native developer community has grown significantly in recent quarters. That growth reduces some scarcity but raises demand for specialized CNF orchestration skillsets. The report offers staffing and skills‑transition models to avoid rate‑runups and project slippage.

Technology convergence: DPU/accelerator ecosystems and edge compute architectures materially change infrastructure economics. Our analysis identifies which CNF attributes benefit most from acceleration and how to prioritize investments across hardware and software stacks.

Adoption friction: Legacy VNF migration paths, stateful service decomposition, and observability gaps are the common causes of multi‑month delays. The report prescribes specific incremental approaches to minimize customer experience risk while modernizing the stack.

Prioritize open validation: Insist on third‑party or vendor certification of CNFs against your chosen cloud substrate. Certification programs materially shorten integration timelines and reduce unforeseen interoperability costs.

Adopt a two‑track migration: Combine a fast‑lane for greenfield edge services with a deliberate staged approach for core network functions that require stateful decomposition.

Invest in observability and SRE enablement early: CNF operational maturity depends on automated observability, chaos testing, and SRE practices. Budget these capabilities into initial rollouts rather than as afterthoughts.

Leverage accelerator hardware judiciously: For throughput‑sensitive functions, evaluate DPU and SmartNIC paths against soft costs (e.g., complexity) and hard benefits (e.g., packet processing offload). Our TCO models quantify breakpoints by workload class.

Design procurement for composability: Contract terms should support mix‑and‑match CNFs and portability across public, private, and hybrid clouds. We provide contract language templates in the full report to protect against vendor lock‑in.

The research combines bottom‑up market modeling, primary interviews with operator CIOs and vendor product leaders, and a granular examination of product roadmaps and validation programs. The historical series covers 2020–2025 and underpins a scenario‑based forecast for 2026–2032. We incorporate CR‑level concentration analysis and a supplier maturity framework to surface strategic supplier‑market fit. Proprietary segment allocations, vendor scoring matrices, and detailed country‑level splits are reserved for subscribers to preserve the integrity of our models and to drive verified engagement.

True to the “trailer” principle, this release emphasizes conclusions and strategic implications while withholding the detailed, proprietary tables and segment‑level allocations that make the report actionable for procurement and M&A decisioning. Specifically, the full report contains:

Granular regional and application split data tied to forecast scenarios;

Vendor ranking matrices with weighted scoring and proprietary scorecards;

Configurable TCO spreadsheets and deployment checklists;

Subscriber‑only annexes with vendor contracts and procurement templates.

These assets are gated because their commercial value is tied to client engagements and bespoke advisory work. Accessing them also enables clients to commission tailored models that reflect specific network architectures and business objectives.

For operators: Use the guidance to prioritize 2026 CNF pilots, secure certification pathways, and align capital plans with anticipated demand curves.

For cloud providers and platform vendors: Validate product roadmaps against the performance, security, and orchestration requirements outlined here — accelerate partner certifications where market pull exists.

For investors and strategics: Identify pockets of value in specialized CNF vendors, DPU‑acceleration stack providers, and orchestration tooling with a clear path to operator referenceability.

To access the complete Cnf Software Market report, including the full dataset, vendor scorecards, and deployment playbooks, please visit the PW Consulting research portal or contact your PW account lead. The full dossier contains the empirical back‑ends you need to convert the strategic implications above into executable roadmaps for 2026 and beyond.

— PW Consulting, Senior Strategic Advisor & Chief Industry Analyst

For detailed analysis of this topic, please visit the official page:Cnf Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com