Competitive Analysis of the North America Pediatric Orthopedic Implants Market

Health |

2026-06-26 14:21:42

PW Consulting’s latest market study on Trimethylaluminum (TMA) for high-purity applications distills actionable intelligence for C-suite leaders, strategic procurement teams, and technical decision-makers preparing plans for 2026. The research synthesizes a decade of industry signals, regulatory shifts, feedstock dynamics, and supplier positioning into a compact playbook: deep enough to establish confidence in our forecast and methods, but intentionally reserved on granular subsegment figures to drive qualified readers to the full report for transaction-grade detail.

Trimethylaluminum Tma For High Purity Application Market

TMA demand for high-purity applications has moved from a niche specialty into a structurally growing market tied closely to advanced electronics and optoelectronics manufacturing. Our historical analysis shows the global market expanding from approximately USD 147 million in 2020 to USD 214 million in 2025. With a forecast horizon beginning in 2026, the market is projected to continue its growth trajectory — the 2026 market base is modestly higher than 2025, and by the end of our projection period in 2032 the market reaches a materially larger scale, reflecting a 2026–2032 compound annual growth rate of 8.2%.

Trimethylaluminum Tma For High Purity Application Market

That growth is neither uniform nor frictionless. Demand is being driven by a combination of continued scaling in semiconductor atomic layer deposition (ALD) and complementary growth in LED and photovoltaic applications. These end-markets exhibit differing cadence of investment cycles, technology refresh timelines, and purity requirements — a complexity that turns a single-figure market projection into a strategic planning challenge for buyers, producers, and investors entering 2026.

Trimethylaluminum Tma For High Purity Application Market

Timing matters for capacity and contracts. Firms planning capital investments or multi-year supply contracts in 2026 must account for a market that is both growing and concentrated. The top-tier concentration metrics indicate that an outsized share of supply sits with a small group of incumbents, which affects negotiating leverage, time-to-supply, and contingency planning.

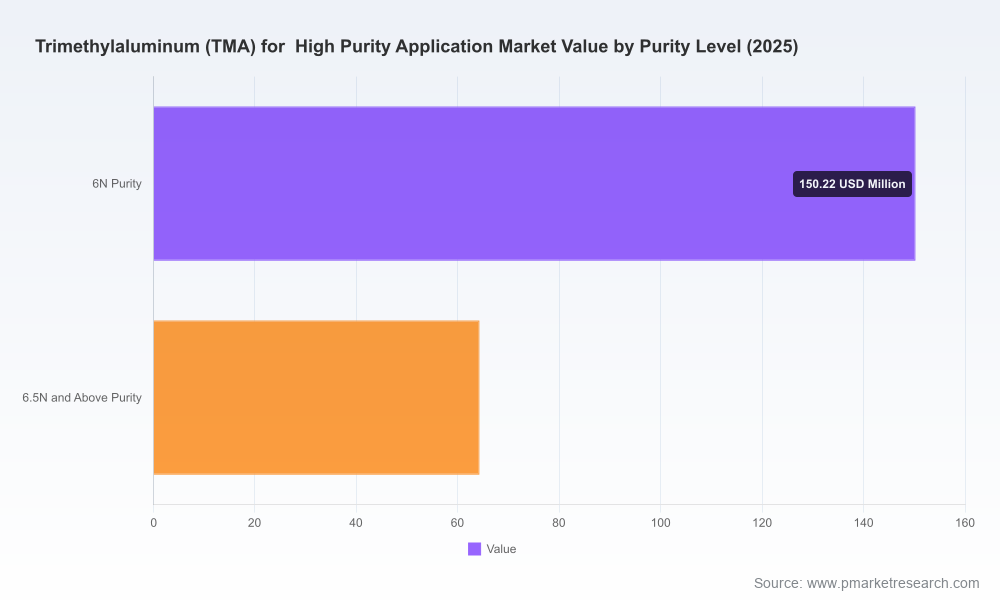

Purity laddering impacts product roadmaps. High-purity TMA is not fungible across applications. R&D and product teams must align precursor specification roadmaps to foundry/OSAT requirements, balancing incremental purity upgrades against cost and supply risk. The strategic trade-offs between in-sourced purification, long-term supply contracts, or dual-sourcing must be evaluated with granular vapor-phase and impurity-spec data — available in the full report.

Procurement must hybridize cost and risk metrics. The price of primary aluminum (a key upstream feedstock) and policy developments materially influence feedstock economics. For example, global aluminum pricing reached approximately USD 3,468.50 per tonne in early April 2026 — a reminder that precursor cost curves can pivot on metal markets, adding volatility to TMA margins. Procurement strategies that incorporate volatility buffers, indexation clauses, and strategic storage will outperform purely price-focused tactics.

Regulatory compliance is a non-negotiable cost center. Aluminum alkyls including TMA are subject to stringent safety and environmental frameworks (for example, OSHA and REACH). Compliance is a recurring capital and operating expense that influences supplier selection and site footprint decisions; firms launching new manufacturing lines in 2026 should budget for enhanced safety systems, training, and insurance.

TMA sits downstream of primary aluminum production; thus, geopolitical and upstream raw material considerations are central to strategic planning. Bauxite remains the principal ore for primary aluminum and has been identified by regional authorities as a critical raw material due to supply risk. Trade measures such as Section 232 tariffs and tariff-rate quotas continue to influence North American feedstock pricing and availability — effects that cascade into regional cost differentials for TMA producers. For buyers and investors alike, scenario planning that incorporates feedstock shocks, tariff shifts, and logistics disruptions is essential for 2026.

In parallel, the hazardous and pyrophoric nature of TMA increases the complexity of logistics and storage. Regulatory compliance and safety protocols add fixed and variable costs to the supply chain, favoring suppliers with scale, engineering expertise, and proven compliance records. Expect counter-parties to price these capabilities into long-term agreements.

The TMA high-purity market is characterized by a compact set of global specialists and regional challengers. Market concentration indicators show that the top three producers command a material share of global capacity, while the top five further consolidate supply — a structural feature that matters for access, lead times, and price setting.

Large integrated producers: Established players with sizable feedstock integration and multiple production sites bring scale advantages, broad product portfolios, and advanced quality control processes. Their investments in process improvements and tailored high-purity grades have sustained their leadership in high-volume segments.

Specialized high-purity suppliers: A set of European, Japanese, and Korean specialists compete on ultra-low impurity performance, certified vapor delivery, and global technical support. These suppliers are often the partner of choice for advanced ALD and MOCVD processes that demand deterministic precursor performance.

Regional challengers and new entrants: Chinese and other regional manufacturers have matured in quality and logistics capabilities, expanding options for local OEMs and EMS providers. Their presence changes negotiation dynamics, particularly for regionally focused procurement, but due diligence on quality traceability and regulatory compliance remains critical.

Recent vendor developments underscore these dynamics. Leading-volume producers have continued product refinements to better serve semiconductor and LED markets, while specialized suppliers have emphasized global availability of ultra-low impurity grades. These moves are tactical signals that incumbents aim to lock-in end-market relationships ahead of major fab ramps and LED/solar cycles — a pattern prospective buyers should anticipate when structuring 2026 procurement and partnership agreements.

Our report is expressly designed to be operational for 2026 decision-making. It includes:

Proprietary market model with historical baseline (2020–2025) and a 2026–2032 forecast, incorporating demand-by-end-market scenarios, sensitivity to feedstock price shocks, and alternate technology adoption curves.

Supplier scorecards and operational diagnostics that evaluate quality systems, logistics resilience, and regulatory posture — a practical toolset for RFP shortlists and supplier audits.

Scenario playbooks covering near-term supply disruption, rapid purity upshift, and regional tariff shocks, with recommended contract structures and hedging approaches for each scenario.

CapEx and build-vs-buy decision frameworks, including normalized NPV templates and break-even run-rate calculators tailored to high-purity TMA production investments.

Regulatory & safety compliance checklists and estimated compliance-cost ranges to embed in supplier selection and site planning.

M&A and partnership screening criteria for corporates looking to accelerate capability through acquisition or joint-ventures.

To preserve the competitiveness of this research for clients executing near-term transactions, subsegment-level figures, supplier share breakdowns, and transaction-ready appendices are available only in the full published report.

Institutionalize supply resilience: adopt multi-tiered sourcing with at least one scale supplier and one specialized ultra-purity supplier in contractual rotations.

Lock quality with process alignment: embed precursor qualification into product development cycles and negotiate vapor-phase delivery guarantees tied to performance KPIs.

Hedge against feedstock volatility: build contractual clauses that allow price pass-through or indexation to primary aluminum markets, and consider strategic inventories for critical ramp periods.

Budget for compliance as a strategic cost: include regulatory and safety CAPEX in project plans early to avoid downstream delays in commissioning and certification.

Scan the landscape for value-accretive partnerships: late-2025 and early-2026 vendor moves indicate opportunities for strategic alliances that secure capacity or co-develop tailored grades.

For executives shaping 2026 budgets, procurement strategies, or investment pipelines, this report functions as both a strategic briefing and a tactical toolkit. The PW Consulting analysis helps prioritize where to commit capital, when to execute long-term procurement agreements, and how to structure supplier relationships to reduce execution risk during aggressive semiconductor and optoelectronic buildouts.

To access the full dataset, detailed supplier share analysis, subsegment valuation tables, and transactional appendices that support contract negotiation and investment decisions, please consult the published report page. PW Consulting stands ready to support bespoke deep-dive workshops, supplier diligence, and scenario-run facilitation to translate these insights into executable plans for 2026.

For detailed analysis of this topic, please visit the official page:Trimethylaluminum Tma For High Purity Application Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com