Nepal Elderly Care Market Overview: Key Drivers and Challenges

Other |

2026-03-05 05:31:05

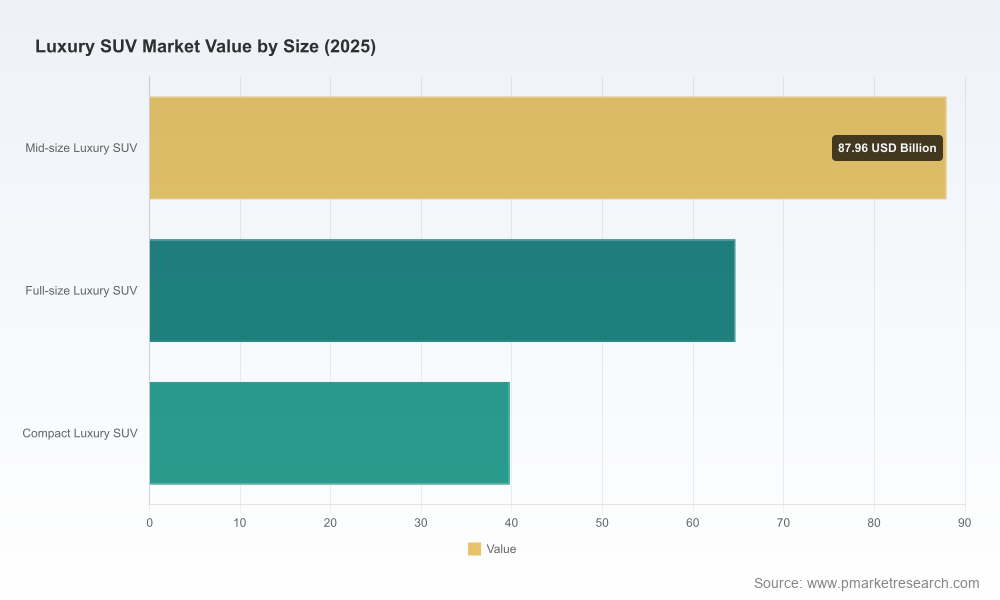

Our latest Luxury SUV Market report (base year 2025) presents a forward-looking, decision-ready framework for executives preparing strategic plans in 2026. The global luxury SUV market reached approximately USD 192.4 billion in 2025 and — at an 8.0% compound annual growth rate across the 2026–2032 forecast window — is expected to approach USD 330 billion by 2032. This trajectory underscores an inflection point: strong near-term demand coexists with structural shifts in propulsion, materials sourcing, and regulatory compliance that will determine winners and losers over the next planning cycle.

Luxury Suv Market

Actionable foresight: We translate macro momentum into concrete strategic choices — product portfolios, manufacturing footprints, and capital allocation scenarios tailored for 12–36 month execution horizons.

Luxury Suv Market

Risk-calibrated investments: With market concentration information showing a measurable advantage for leading OEMs, the report surfaces where scale matters and where focused differentiation can win.

Luxury Suv Market

Regulatory preparedness: New battery and emissions rules mean 2026 decisions must anticipate compliance cliffs through 2031 and beyond. This report maps those cliffs to product and supply-chain levers.

The luxury SUV segment combines growth momentum with complex structural change. After steady expansion through 2020–2025, the total addressable market stood at roughly USD 192.4 billion in 2025. Under our central forecast (CAGR 8.0% for 2026–2032), market value is projected to increase materially by 2032, reflecting a blend of premiumization, shifting buyer preferences toward electrified drivetrains, and continued appetite for larger, feature-rich vehicles in key demographics.

For 2026 planning, senior leaders should treat the growth forecast as directional rather than uniform: pockets of accelerated opportunity will be created by successful electrification programs, innovative ownership models, and premium services (e.g., concierge, subscription, bespoke customization). Conversely, legacy product lines that fail to adapt to tighter CO2 targets and battery regulations risk margin erosion even within an expanding nominal market.

The luxury SUV arena remains contested by legacy premium OEMs and fast-moving challengers. Our competitive analysis synthesizes capability maps for the leading groups and highlights where each is likely to compete in 2026 and beyond:

BMW Group (Munich) — Strengths: breadth of product family, performance positioning, and accelerating electrified models. Strategic imperative: convert brand loyalty into charging and software-led retention.

Mercedes‑Benz Group AG (Stuttgart) — Strengths: comfort, safety, and a premium EV roadmap. Strategic imperative: monetize software and services while optimizing platform commonality across ICE and EV architectures.

Audi AG (Ingolstadt) — Strengths: quattro heritage and design credibility. Strategic imperative: maintain volume through next‑generation compact-to-large models with clear EV differentiation.

Porsche AG (Stuttgart) — Strengths: high-performance credentials; growing EV variants. Strategic imperative: preserve margin through performance-led optionalization and limited-run halo models.

Jaguar Land Rover (Coventry) — Strengths: off-road luxury cachet. Strategic imperative: balance legacy 4x4 capability with electrification investments to avoid softness among younger buyers.

Lexus (Toyota) (Toyota City) — Strengths: reliability and hybrid expertise. Strategic imperative: leverage hybrid strength while accelerating BEV models in portfolio markets.

Genesis (Hyundai) (Seoul) — Strengths: value proposition and modern design. Strategic imperative: scale brand awareness in premium markets via targeted model launches and service experience.

Cadillac (GM) (Detroit) — Strengths: full‑size presence; EV ambitions. Strategic imperative: convert Escalade loyalty into EV adoption with differentiated interior space and tech.

Ultra-premium marques (Rolls‑Royce, Bentley, Aston Martin, Lamborghini) — Strengths: exclusivity and craftsmanship. Strategic imperative: maintain bespoke value while exploring low-volume electrified offerings that preserve brand stories.

Volvo, Maserati, Lincoln and others — Each combines distinct propositions (safety, design, American luxury). For 2026 planning, these brands should prioritize narrow, high-margin niches rather than head-to-head scale battles.

Recent product and go‑to‑market moves underscore these dynamics: Cadillac’s preparations for new electric Escalade models in 2026, Audi’s compact SUV redesign, Lucid’s launch in the EV-premium SUV niche, and BMW’s continued SUV sales strength are examples of how incumbent and new players are shaping near-term competitive set pieces.

Two forces will dominate procurement and manufacturing decisions in 2026:

Raw material price and availability volatility: Battery-pack cost declines driven by raw material trends create opportunity for margin capture if procurement is timed and hedged appropriately. However, geopolitical concentration in critical mineral processing adds downside risk that requires diversified sourcing and strategic inventory policy.

Regulatory constraints: Emerging battery rules — including recycled-content mandates phased in toward the end of the decade — demand immediate planning. From a 2026 perspective, OEMs and suppliers must design recyclability, battery chemistry flexibility, and recycled-content traceability into mid‑term sourcing agreements.

Electrified portfolio sequencing: Prioritize high-margin models for earliest BEV conversion while retaining hybrid options in markets where charging infrastructure or regulatory timelines lag.

Supplier partnerships and vertical levers: Lock in upstream access to battery components through strategic equity, long-term offtakes, or pooled procurement to reduce exposure to short-term commodity swings.

Platform and modularization economics: Invest selectively in flexible architectures that support ICE, hybrid, and BEV variants to lower per-unit cost and shorten time-to-market.

Services and software monetization: Build subscription, personalization, and remote-service offers that can convert initial vehicle sales into recurring revenue streams.

Regulatory forward‑engineering: Embed compliance scenarios (battery recycled content, CO2 targets) into product roadmaps and capital plans now to avoid expensive retrofits later.

Key downside risks include sharper‑than-expected tightening of CO2 regulations, raw-material supply disruptions, and faster-than-anticipated price competition from new entrants. Mitigation approaches in the report include stress-tested capital allocation models, contingency manufacturing footprints, and prioritized technology investment roadmaps that allow staging of high-cost items.

Designed for C-suite and strategy teams, the report combines macro forecasts with executable tools: scenario-based P&L templates, a supplier heatmap with Tier‑1/2 segmentation, a regulatory timeline with compliance action items, go‑to‑market playbooks for electrified launches, and a scorecard framework for M&A and partnership evaluation. Importantly, detailed segmentation tables and proprietary regional / propulsion splits are presented in the full report and accompanying dashboard — deliberately withheld in this release to preserve the intelligence auctioned through our web portal.

Market concentration metrics indicate that a small group of OEMs command a material share of the segment, creating both barriers and opportunities. For acquirors and challengers, the path to scale is likely through targeted differentiation, bolt-on acquisitions in electrification or software, or highly focused geographic rollouts that avoid direct parity competition with top incumbents.

Battery ecosystem investments: cell manufacturing, recycling, and advanced chemistry startups will attract strategic capital as OEMs seek control over cost and compliance.

Software and data companies: firms enabling OTA updates, telematics monetization, and in-car experiences will be premium targets.

Aftermarket and experience providers: premium subscription models for services and personalization present attractive recurring revenue pathways that complement vehicle sales.

The analysis is underpinned by historical data (2020–2025), a base year of 2025, and a 2026–2032 forecast horizon. We synthesize OEM disclosures, dealer networks, supply‑chain intelligence, regulatory filings, and proprietary demand modeling. Market concentration metrics reflect competitive composition as of the base year and are integrated into our scenario analyses.

For leadership teams building 2026 budgets and three-year strategic plans, our Luxury SUV Market report functions as a playbook: it identifies where to commit capital, where to form alliances, and which capability gaps to close first. To access the full data tables, segmentation breakdowns, and downloadable scenario models, please visit the report landing page — the granular intelligence required to convert this strategic preview into executable action is available there.

For detailed analysis of this topic, please visit the official page:Luxury Suv Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com