Fairdeal - Online Cricket ID Destination for Exciting Cricket Betting Entertainment and Fun

Games |

2026-05-13 12:18:12

As industry leaders prepare budgets and strategic plans for 2026, the transfer glove box market presents a clear, measurable opportunity — but one that rewards selective, data‑driven decisions over broad, hardware‑only plays. Our latest PW Consulting market study finds the total market expanded from an estimated USD 205 million in 2020 to roughly USD 275.5 million in 2025, and is modeled to climb to about USD 418 million by 2032 at a compound annual growth rate (CAGR) of approximately 6.15% across the 2026–2032 forecast window. These headline figures encapsulate both steady replacement cycles in regulated pharma and healthcare settings and accelerating adoption in high‑growth end markets such as advanced battery manufacturing and electronics research.

Transfer Glove Box Market

Regulatory tightening is increasing the cost of non‑compliance. Guidance that drives critical‑zone cleanliness (FDA and EU GMP Annex 1 expectations around ISO 5 environments) and compounding/containment standards (USP <797> and USP <800>) is forcing health‑system and pharma buyers to prefer integrated isolator solutions over makeshift engineering controls.

Transfer Glove Box Market

Capital planning is under renewed scrutiny. Hospital and institutional capex dynamics—illustrated by elevated capex-to‑depreciation ratios in FY24—mean procurement committees are more sensitive to lifecycle cost, validation burden and service economics than before.

Transfer Glove Box Market

Cross‑industry demand is broadening. While pharmaceutical and biotech applications remain core drivers, transfer glove boxes are increasingly specified in battery cell manufacturing, advanced materials R&D, and specialty electronics, creating pockets of accelerated investment and product customization need.

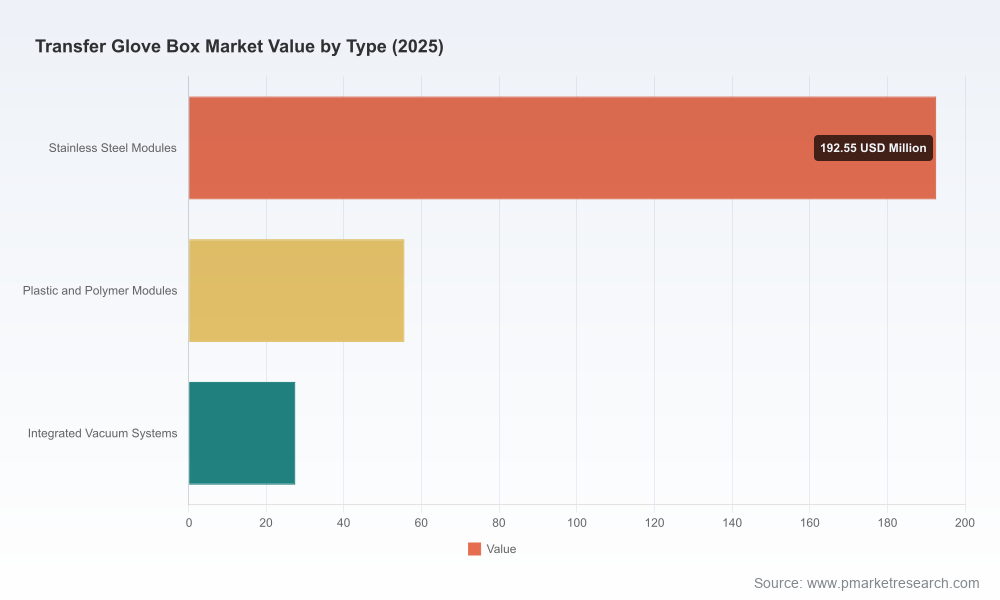

The market’s mid‑single‑digit CAGR masks heterogeneity consumers must navigate. Product families range from stainless steel containment modules and polymer/glass enclosures to integrated vacuum transfer systems; buyer priorities vary from aseptic assurance and particulate control to powder containment (OEB levels) and radiopharmacy traceability. Geographies show differing procurement rhythms — some regions continue to prioritize turnkey isolators with service contracts, while others favor modular, lower up‑front cost solutions. Finally, aftermarket and services (validation, spare parts, field calibration) are material contributors to supplier economics and should be central to any vendor selection model.

PW Consulting intentionally highlights this complexity without disclosing granular segment shares in this executive preview — the objective is to demonstrate decision‑ready insight while directing practitioners to the full report for line‑by‑line figures and model access.

The market shows moderate concentration: the top three suppliers capture a meaningful but not dominant share, and the top five increase that share further — a structure that sustains specialist opportunities for mid‑tier and regional players. Key strategic archetypes are visible:

High‑assurance European OEMs that stress stainless steel isolator engineering and integrated transfer systems. These vendors compete on durability, custom containment and regulatory pedigree (notably for radiopharmaceutical and high‑potency APIs).

US and global suppliers focused on sterile compounding and biological containment, leveraging class‑III and Class‑A portfolio depth alongside service ecosystems for health systems and compounding pharmacies.

Smaller, agile vendors offering portable enclosures and modular polymer systems that reduce lead times and capex — attractive in research labs or facilities with rapid reconfiguration needs.

Representative competitive profiles (high‑level, directional):

Jacomex (France): A specialist in stainless steel glove boxes and isolators with integrated transfer systems, positioned strongly for pharmaceutical and containment applications where engineered stainless designs and pressure control are requisites.

ITECO Engineering (Italy): Notable for modular PMMA and custom containment solutions across pharmaceutical packaging, lyophilization interfaces and radiopharmacy; product introductions in 2025 underscore continued investment in aseptic and radiochemical containment niches.

Getinge (Sweden): Leverages established transfer system technologies for aseptic and high‑potency API transfer; win conditions include proven leak‑free transfer interfaces and pharma‑grade integration capability.

Comecer (Italy): Emphasizes advanced isolator technology for radiopharmacy and cell therapy, often positioning isolators as a superior alternative to traditional cleanroom models for certain sterile and hazardous workflows.

The Baker Company, Germfree, Labconco and Terra Universal (United States): These suppliers form a contiguous group addressing sterile compounding, biosafety and powder containment across healthcare and research labs, with differing emphasis on standardized vs. custom builds and aftermarket services.

Erlab (France): Competes on portable, lab‑scale transfer enclosures that serve research and diagnostic buyers seeking rapid deployment and lower weight/construction cost.

Recent product activity, including new aseptic isolator launches and radiopharmacy containment modules through 2025, signals supplier willingness to innovate around compliance needs (e.g., designs targeting Annex 1 and specific radiopharmaceuticals). Expect targeted product introductions and aftermarket subscription pilots as suppliers chase higher life‑time value.

For suppliers: Shift commercial conversations from capex to total cost of ownership and regulatory risk mitigation. Offer validated service tiers, digital validation artifacts and capacity to support site qualification to shorten procurement cycles.

For OEM R&D: Prioritize modular product architectures that allow chips, sensors and transfer interfaces to be field‑upgraded. Customers increasingly value retrofittable HEPA/ULPA, monitoring stacks and secure transfer locks over one‑off bespoke chambers.

For buyers (health systems, CMOs, battery and semiconductor fabs): Insist on vendor deliverables mapped to specific regulatory clauses (ISO 5 assurance, USP requirements) as part of procurement contracts. Require lifecycle service KPIs and transparent spare‑parts cost schedules to avoid hidden operating expenses.

M&A and partnerships: Expect consolidation pressures around service networks and software‑enabled validation. Strategic tuck‑ins that expand field service footprints or add digital compliance platforms will be highly accretive.

This study is designed as an operational playbook for 2026 decisions. Key deliverables include:

Modelled market sizing and scenario forecasts through 2032 with sensitivity runs for regulatory shocks, supply‑chain disruptions and accelerated end‑market adoption.

Vendor benchmarking across product, service, regulatory proof‑points, and aftermarket economics, with a supplier scorecard and likely move‑set scenarios.

Regulatory mapping and procurement clause templates tying FDA, EU GMP and USP expectations to acceptance criteria and test procedures for supplier selection and contract language.

CapEx vs. OpEx calculators and a validation time‑to‑acceptance model that show how design choices (material, transfer type, automation) influence payback and time‑to‑production.

Buyer playbooks with short‑listing criteria by application (aseptic production, high‑potency compounding, radiopharmacy, battery cell assembly), including recommended test protocols and service level agreements.

M&A and partnership pathways, including target archetypes and post‑deal integration checklists focused on field service consolidation and digital validation assets.

All of the above is built from a combination of primary interviews with procurement and plant engineering leaders, equipment OEM executives, and hands‑on technical assessments — not just desk research. To preserve the advisory value of that work, the published executive summary omits detailed segment tables and company revenue shares; subscribers get full model access and raw interview appendices.

Procurement: Run a short RFP that treats service and validation deliverables as scoring criteria at parity with price; require vendors to demonstrate Annex 1/USP mapping.

Facility planners: Use modular pilots for new workflows (e.g., battery cell prototype lines) to de‑risk full‑line capex commitments and accelerate time to data.

OEMs: Invest in retrofit kits and digital validation toolchains that convert hardware buyers into recurring revenue customers through subscription‑style assurance services.

Executives considering M&A: Prioritize targets that add field service density, spare parts logistics, or digital compliance IP rather than incremental product SKUs.

Regulatory & quality leads: Update acceptance protocols to reflect current FDA/Annex 1 language and incorporate USP <800> containment criteria where hazardous drugs are handled; require pre‑installation FAT/SAT evidence.

The transfer glove box market is neither a narrow niche nor a commoditized box‑moving exercise — it is a complex ecosystem where product engineering, regulatory proof, aftermarket service and go‑to‑market design determine who wins. The market’s mid‑single‑digit growth belies pockets of rapid adoption and bespoke demand that will define supplier success through 2032.

PW Consulting’s full Transfer Glove Box Market report contains the detailed segment models, regional and application breakouts, supplier financial proxies and interview transcripts necessary to convert these high‑level signals into executable 2026 plans. For practitioners seeking the underlying tables, scenario files and supplier scorecards, visit the PW Consulting report page to download the complete study and supporting spreadsheets.

For detailed analysis of this topic, please visit the official page:Transfer Glove Box Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com