Arc Welding Equipment Market Growth: Emerging Opportunities and Market Drivers

Other |

2026-02-24 13:36:19

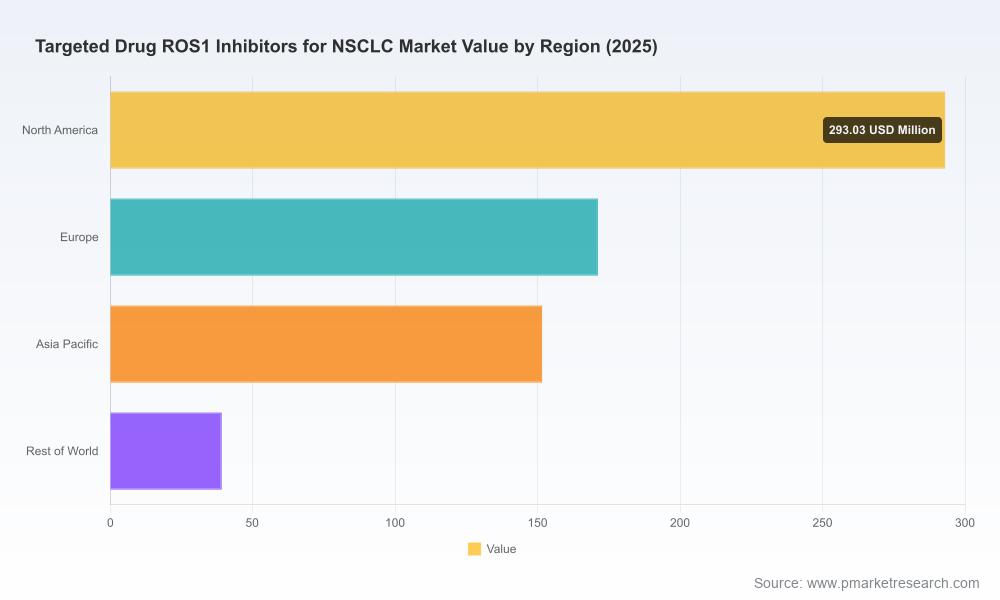

PW Consulting’s new market study on Targeted Drug ROS1 Inhibitors for non‑small cell lung cancer (NSCLC) delivers the focused, operational intelligence executives need to set strategy in 2026. Anchored to a 2025 base year and a 2026–2032 forecast horizon, the study synthesizes market dynamics, clinical trajectories, and commercial levers into pragmatic actions. The market has grown rapidly—from a modest base in 2020 to an estimated USD 655.0 million in 2025—and under our modeled scenarios we project a continued expansion to roughly USD 1,726.4 million by 2032 at a compound annual growth rate of 14.85%. These headline figures understate a more nuanced opportunity: competitive shifts, patent events, diagnostic adoption and next‑generation clinical readouts will shape winners and losers between 2026 and the early 2030s.

Targeted Drug Ros1 Inhibitors For Nsclc Market

Several converging developments make 2026 a pivotal year for corporate strategy in the ROS1 inhibitors space. The competitive footprint has changed materially over recent years: next‑generation agents targeting ROS1 resistance mechanisms have entered the clinic and, in several cases, the marketplace. Regulatory milestones through 2024 expanded first‑ and later‑line labeling and broadened pediatric indications, while companion diagnostics have become standard of care for identifying ROS1 rearrangements. At the same time, IP timelines for legacy first‑generation agents approach the late 2020s, creating a tangible patent cliff that will change pricing, access and contracting dynamics.

Targeted Drug Ros1 Inhibitors For Nsclc Market

For strategy teams, 2026 is the year to transition from defensive portfolio protection to proactive value capture. Companies that act early on lifecycle extensions, diagnostic partnerships and differentiated clinical data will secure durable positioning as the market grows at mid‑teens CAGR.

Targeted Drug Ros1 Inhibitors For Nsclc Market

Proprietary market model (2020–2032) with scenario and sensitivity modules: baseline, conservative, and accelerated uptake curves tied to alternative clinical outcomes and patent expiry assumptions.

Clinical landscape and pipeline heatmap: stage‑by‑stage analysis of ROS1‑directed programs, resistance mitigation profiles, and the likely timing of pivotal readouts.

Regulatory and reimbursement playbook: dossier requirements by major markets, payer evidence thresholds and a roadmap to secure favorable listing and reimbursement terms.

Commercial go‑to‑market framework: pricing strategies, channel optimization, diagnostic co‑promotion models and hospital tender dynamics tailored to ROS1 therapies.

M&A and partnership decision tools: valuation scenarios, deal structuring benchmarks, and a matrix for evaluating bolt‑on vs. transformational acquisitions in the ROS1 ecosystem.

Operational readiness checklists: launch sequencing, manufacturing scale‑up triggers, and supply chain contingency plans to insulate revenue against sudden demand shifts.

Risk and mitigation matrix: patent expiries, generics entry, clinical failure scenarios and regulatory setbacks quantified by financial exposure and time to recovery.

Note: this summary intentionally highlights the actionable deliverables while preserving the proprietary granularity of sub‑segment and regional figures contained in the full report. Organizations that require the detailed breakouts and raw model access will find those in the comprehensive subscription package and downloadable dataset.

The ROS1 inhibitor market is concentrated—our CR3 and CR5 concentration metrics are 82.4% and 94.15% respectively—indicating a small group of firms currently dominate commercial supply and influence treatment standards. Key players have distinct strategic positions:

Roche (Basel) and its U.S. affiliate Genentech compete with both legacy and label‑expanded assets and benefit from established diagnostic partnerships and hospital networks.

Pfizer retains strategic value as the originator of the first broadly adopted ROS1 inhibitor, with an incumbent advantage in clinical familiarity and guideline inclusion.

AstraZeneca has positioned its ROS1‑active agent with broad histology labeling, enhancing utility across tumor types and patient subgroups.

Turning Point Therapeutics—now integrated into Bristol Myers Squibb—represents the archetype of a next‑generation entrant: repotrectinib’s approvals have shifted the competitive set by addressing patients who progress on earlier inhibitors.

Strategically, incumbent firms must decide how to defend front‑line franchise value against superior next‑generation molecules, while entrants must convert differential clinical efficacy into durable payor and prescriber preference. The full report drills into win‑loss scenarios by molecular profile and line of therapy to help commercial teams prioritize investment.

Patent expiries and generic risk: the impending loss of exclusivity for a first‑generation agent in the near term makes lifecycle management and patent‑surfacing tactics critical to maintain revenue flow.

Diagnostic adoption: validated companion diagnostics are a gating factor for patient identification. Integration with diagnostic vendors and reimbursement alignment is a high‑ROI activity.

Clinical differentiation: next‑generation inhibitors that demonstrate improved control of CNS disease and resistance mutations will command premium pricing and faster uptake.

Reimbursement pathways: inclusion in clinical guidelines and robust real‑world evidence will accelerate payor contracting; companies should prioritize post‑launch evidence generation.

Accelerate diagnostic partnerships: co‑develop or co‑commercialize companion testing to secure the patient funnel and create switching friction for competitors.

Pursue targeted lifecycle extensions: invest selectively in label expansions and pediatric programs where clinical and commercial return exceeds the marginal cost.

Model generic entry scenarios now: build pricing flexibility and tender strategies to blunt near‑term erosion post‑patent expiry.

Prioritize evidence that matters to payors: CNS progression metrics, durability of response and quality‑of‑life endpoints are decisive for reimbursement in many markets.

Consider M&A to acquire pipeline diversity: for companies lacking a differentiated ROS1 program, bolt‑on deals may be faster and more predictable than internal R&D to claim share in an accelerating market.

Global and regional pharma strategy teams: align portfolio investment decisions, R&D prioritization and launch sequencing against robust uptake scenarios and patent timelines.

Business development and corporate development: screen targets, structure deals and build integration plans using our valuation levers and sensitivity runs.

Market access and patient access leads: design evidence plans and contracting propositions rooted in the payer playbook and guideline dynamics.

CROs, diagnostics and CDMOs: identify service demand curves and capacity planning signals to position for cohort expansion and companion test deployment.

Our model uses a mix of primary interviews, public filings, regulatory announcements and proprietary adoption curves. Forecast scenarios factor in alternative clinical outcomes and timing of pivotal readouts. Users should layer organizational risk tolerances and regional operational constraints onto our baseline to derive executable plans. For example, the market prevalence of ROS1 rearrangements (reported in literature at roughly 1–2% of NSCLC cases) and the regulatory environment—companion diagnostic approvals and guideline inclusions—are embedded into patient‑flow assumptions that drive our modeled uptake. The report also includes a transparent appendix with model assumptions and a reproducible workbook for bespoke adjustments.

By 2026, the ROS1 inhibitor landscape will reward decisive strategy: companies that align clinical differentiation, diagnostic integration and payer evidence generation will capture disproportionate share as the overall market expands at approximately a mid‑teens CAGR through 2032. PW Consulting’s report is structured to guide that strategic pivot—delivering the market model, competitive playbook and operational checklists needed to convert hypotheses into measurable outcomes.

For access to the full dataset, segment breakouts, interactive forecast model and the complete competitive profiles including financial and regional granularity, visit the report landing page. PW Consulting clients can request a tailored briefing to map these insights into a company‑specific 90‑day action plan.

For detailed analysis of this topic, please visit the official page:Targeted Drug Ros1 Inhibitors For Nsclc Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com