Antivirus Software Market Value Driven By Rising Global Cybersecurity Investments Worldwide

Other |

2026-06-23 05:18:32

PW Consulting’s newly completed Primary Cell Culture Market study provides a practical, strategy-focused playbook for life-science executives preparing for the next phase of commercial expansion. By the end of 2025 the primary cell culture market had reached approximately USD 6,854.2 Million. Under a set of evidence-based scenarios the market is forecast to expand at a compounded annual growth rate (CAGR) of 12.5% through the 2026–2032 horizon, with a central-case projection that takes full account of regulatory shifts, supply‑side stress and accelerating adoption of complex in vitro systems.

Primary Cell Culture Market

Regulatory normalization and explicit guidance: Recent agency guidance is shifting the evidentiary bar toward primary‑cell–based models for IND‑enabling safety, particularly in oncology. Organizations that align their preclinical pipelines to these expectations now will shorten clinical timelines and reduce late‑stage surprises.

Primary Cell Culture Market

Platform convergence: Investment programs — including significant public commitments to organ‑on‑chip technologies — are catalyzing demand for authenticated primary cells integrated into higher‑throughput and physiologically relevant platforms.

Primary Cell Culture Market

Commercial frictions and raw material shocks: Upstream inputs such as animal‑derived sera have seen price volatility and constrained availability; procurement strategies and serum‑free alternatives are therefore rising to the top of operational priorities.

Reimbursement and market access dynamics: Coverage adjustments for certain primary cell‑based assays are beginning to shift the economics of early‑stage clinical work, altering sponsor willingness to invest in higher‑fidelity in vitro models.

This study is intended as an operational guide for business and R&D leaders. It combines market sizing and scenario forecasts with tools that directly support 2026 decision cycles. Key deliverables:

Proprietary market size and scenario models (2020–2032) that can be re‑run with client inputs to stress‑test strategic options.

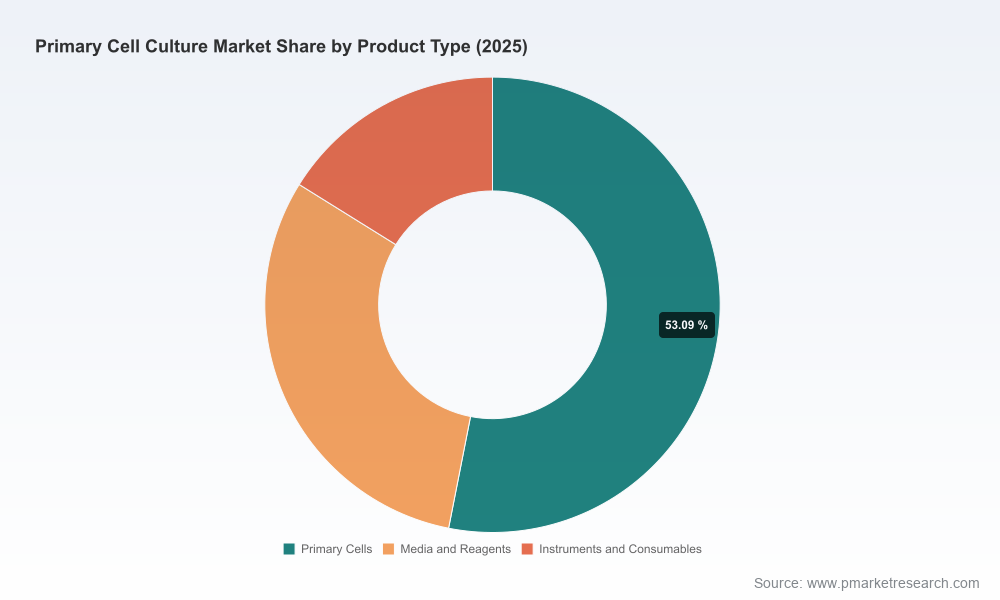

A supplier and product taxonomy aligned to buyer workflows — from cryopreserved primaries through media/reagents to instruments and consumables — enabling rapid vendor shortlisting for specific use cases.

Commercial playbooks and go‑to‑market blueprints for launching new primary cell products or expanding distribution footprints, including channel economics and sales force deployment models.

Procurement levers and cost‑to‑serve analyses that translate raw‑material shocks into hedging strategies, contract clauses and alternative sourcing pathways.

Regulatory and reimbursement impact maps that explain how recent guidance and coverage updates alter product development priorities and pricing flexibility.

M&A and partnership screening frameworks with an M&A heat‑map identifying the most attractive technology adjacencies and target archetypes.

Ready‑to‑use dashboards and Excel models that support board‑level briefings and investment committee decisions — intentionally delivered without the underlying proprietary granular splits in this public summary.

The primary cell market is neither fragmented nor monopolistic: market concentration metrics indicate a meaningful presence of large legacy suppliers combined with a broad field of specialist providers and niche innovators. That dynamic creates both consolidation opportunities and fertile ground for differentiated, application‑specific offerings.

Thermo Fisher Scientific — a scale leader that brings a deep commercial funnel and extensive reagent and instrument integration. Recent product expansion into new tissue types underscores a play to bundle primary cells with complementary Gibco media and consumables, increasing customer switching costs.

Lonza — leverages manufacturing scale and regulatory experience to serve clinical and industrial customers. Catalog updates focused on donor‑matched solutions reflect an emphasis on higher‑value, differentiated primary cell products for translational pipelines.

Merck KGaA (Sigma‑Aldrich) — strong in reagent ecosystems and with a broad portfolio of primary cell types; the firm’s strategy is to pair cells with validated workflows and assay kits for reproducibility in regulated settings.

ATCC — a quality and authentication anchor for the market. Its authenticated cell lines and demonstration presence at immunotherapy conferences position it as a trusted partner for regulated and high‑value applications.

Sartorius (PromoCell) — specialized with an emphasis on serum‑free systems and regulated quality (recent ISO certification). Its focus is on enabling adoption by labs that require stronger quality management across the supply chain.

ScienCell, Celprogen, AcceGen and BioIVT — collectively represent agile, product‑focused competitors. Their differentiators include deep catalogs of niche cell types, 3D scaffold integration, extensive cryopreserved offerings and liver‑specific ADME competence respectively.

Recent commercial moves — from product rollouts to certification announcements and trade‑show debuts — reflect two clear tactics across incumbents and challengers: (1) broaden application coverage through new tissue types and matched media; (2) raise the regulatory and quality bar to capture clinical and contract research demand.

Raw material exposure: Price and availability volatility of animal‑derived inputs necessitates active scenario planning. In 2024 several firms faced material cost increases that compressed margins for commodity reagents; hedging and synthetic/serum‑free conversions are now a commercial priority.

Export and trade controls: New controls on human primary cell exports in key jurisdictions create logistical and legal constraints. Businesses must map product flows and establish compliant supply pathways or local manufacturing partnerships.

Regulatory expectations: Regulators are increasingly explicit about acceptable in vitro model evidence for specific therapeutic areas. Firms that can demonstrate validated, reproducible primary‑cell workflows for IND support gain a competitive advantage.

Reimbursement and commercial adoption: Coverage updates for certain primary‑cell assays change the sponsor calculus for investing in higher fidelity models. This influences both demand timing and willingness to pay for premium product bundles.

R&D prioritization: Use the report’s scenario analyses to decide which primary cell types and integrated platforms to prioritize for internal development vs. outsourced partnerships.

Commercial expansion: Apply the go‑to‑market playbooks to test market entries, channel partnerships, and distributor selection in priority geographies while accounting for export controls and local regulatory requirements.

Cost and procurement strategy: Implement the procurement levers and supplier segmentation tools to mitigate raw‑material disruption and optimize cost structures for reagents and consumables.

M&A and alliance screening: Use the M&A heat‑map to identify targets that deliver rapid capability uplift — for example, firms with 3D scaffold IP, verticalized cryopreservation capability, or validated ADME primary hepatocyte workflows.

Operational risk management: Adopt the risk matrix to set mitigation priorities for supply‑chain, quality, and regulatory changes — translating those into specific actions (dual sourcing, local production investments, quality certifications).

In keeping with the “trailer” approach, this public overview highlights the strategic conclusions and actionable frameworks that senior decision‑makers require, while intentionally withholding the granular, segment‑level numerical tables and raw data that are included in the full report. Those detailed splits — by region, application and product sub‑type — are essential for transaction diligence and vendor selection and are available in the full deliverable through PW Consulting’s research portal or upon client engagement.

For executive teams planning 2026 budgets, R&D roadmaps or M&A pipelines, this study provides a timely evidence base coupled with immediate, operational guidance. PW Consulting is offering tailored briefings and scenario workshops in Q3–Q4 2026 to translate the report into actionable corporate plans. To arrange a briefing or receive the complete dataset and model files, contact PW Consulting’s Life Sciences practice — our consultants will help you convert the market’s projected growth trajectory into a concrete competitive plan.

For detailed analysis of this topic, please visit the official page:Primary Cell Culture Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com