PW Consulting: Strategic Preview — Green Geopolymer Concrete Market Report (2026 Outlook)

PW Consulting today publishes a strategic preview of our forthcoming Green Geopolymer Concrete Market Report, designed to equip executive teams, investment committees, and project leaders with the decision-frameworks they need as they plan for 2026. Our analysis shows the market reaching approximately USD 8.62 billion in 2025 and accelerating to roughly USD 41.11 billion by 2032, reflecting a compound annual growth rate of 25.01% through the 2026–2032 forecast period. This preview highlights the report’s operational value while purposely reserving detailed segment tables and proprietary models for the full report.

Green Geopolymer Concrete Market

Why this matters for 2026 decision‑makers

- Strategic timing: Organizations that establish procurement, certification, and pilot frameworks in 2026 will materially shorten time‑to‑market as construction owners and regulators increase preference for low‑carbon concretes.

- Capital allocation: High growth and supply‑chain dynamics require a reassessment of capex/opex tradeoffs — from localized precursors storage to on‑site batching versus centralized production.

- Regulatory arbitrage: Carbon pricing, EU mechanisms and national building approvals are already differentiating commercial winners from laggards; 2026 is the year to operationalize compliance pathways.

- Partnerships over poaching: Early movers will prioritize feedstock offtake agreements, activator supply contracts, and licensing relationships rather than one‑off procurement.

What the PW Consulting report delivers — practical, executable content

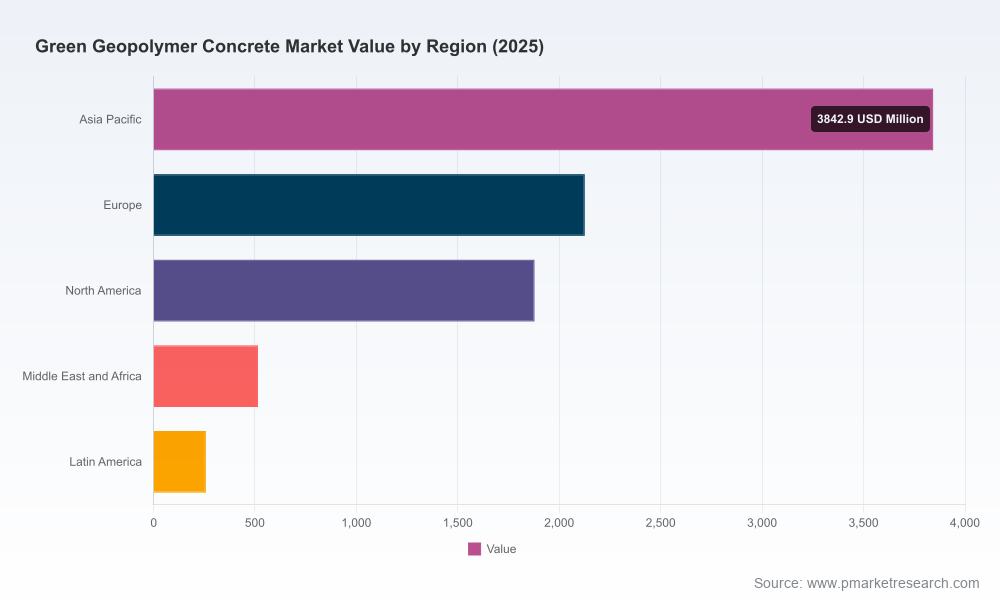

- Actionable market sizing and growth drivers: A clear narrative tying macro demand (policy-driven infrastructure and climate targets) to price and availability of precursor materials, and to construction cycles. (Note: detailed split tables by region, source material and end‑use are available only in the full report.)

- Commercialization roadmaps: Step‑by‑step templates that translate a lab‑validated geopolymer formulation into a commercially viable product — covering pilot design, QA/QC checklists, and scale‑up constraints for plant and mobile batching.

- Procurement & supply playbook: Supplier qualification criteria, contract structures for long‑term precursor supply, logistics optimization for heavy low‑value materials, and LCA‑aligned procurement clauses to secure low‑carbon credits.

- Technical toolkits: Standardized test matrices (strength, durability, fire and chemical resistance), recommended specification language for tender documents, and sample mix‑design variations to support common construction use cases.

- Risk and scenario models: Sensitivity analyses on precursor price shocks, activator availability, and regulatory policy shifts — with ready‑to‑run dashboards for CFOs and risk teams.

- Regulatory and certification matrix: A decision guide showing what approvals and third‑party certifications matter most by application (e.g., structural, fireproofing, shotcrete) and the typical timelines to secure them.

Supply‑chain dynamics — what to watch in early 2026

Raw material flows and pricing are the most immediate levers for cost and feasibility in geopolymer adoption. Recent market intelligence points to divergent regional dynamics: U.S. fly ash prices saw upward pressure in late‑2025 with continued firming into early‑2026; China continues to supply abundant fly ash at much lower delivered price points; India’s policy measures have materially increased utilization and, in many cases, reduced precursor unit costs year‑on‑year. These regional imbalances create both opportunities (arbitrage and export of precursors) and risks (local shortages and price spikes where demand concentrates).

Green Geopolymer Concrete Market

For procurement and operations teams, practical responses include: modeling multi‑precursor blended formulations to reduce exposure to a single feedstock; negotiating indexed long‑term offtake contracts to stabilize margins; investing in on‑site pre‑treatment and quality control to accommodate variable precursor chemistry; and exploring vertical integration where scale economics justify it.

Green Geopolymer Concrete Market

Competitive landscape — who’s setting technical and commercial benchmarks

The market remains fragmented: our concentration metrics show a low combined share for the largest suppliers, underscoring open whitespace for scale players and regional champions. Key companies and their strategic positions as identified in our research include:

- Geopolymer Solutions, LLC (United States) — notable for Cold Fusion Concrete® (a zero‑Portland‑cement geopolymer) and recent third‑party fireproofing certifications issued in March 2025. Its product family (acid‑resistant, self‑leveling, stucco, wastewater variants) sets a benchmark in specification breadth for demanding environments.

- Wagners (Australia) — commercializes Earth Friendly Concrete (EFC®), a cement‑free geopolymer used in structural and infrastructure projects. Recent launches include a zero‑cement shotcrete product for tunnels and pools, demonstrating extension into specialized application engineering.

- Zeobond Pty Ltd (Australia) — focuses on E‑Crete™, emphasizing performance parity with OPC in chemical and fire resistance while delivering material carbon reductions, representing a pragmatic entry point for mainstream contractors.

- MC‑Bauchemie (Germany) — a materials and admixture specialist supplying activators and superplasticizers; alliance activity with project developers has unlocked use in climate‑certified residential schemes.

- Regional and technology specialists — Banah UK, Alchemy Geopolymer Solutions, Ultra High Materials, Kuttuva Silicates (India), Boral, Betolar PLC — together illustrate a mix of niche innovators and incumbents experimenting with productization, paving, and industrial applications.

Strategic implications: certification momentum (e.g., UL/ASTM and national approvals), supply partnerships for precursors and activators, and demonstration projects remain the primary vectors for commercial conversion. Companies with certification wins, robust QA systems, and integrated supply playbooks will command pricing and gain specification preference from major contractors.

Regulatory tailwinds — and the compliance worklist for 2026

Policy and standards are accelerating adoption. Existing approvals and model projects (for example, early national approvals enabling CO₂ savings in residential construction) have already demonstrated feasibility within conservative building codes. Meanwhile, carbon pricing mechanisms and import disciplines on embedded emissions are creating a commercial incentive for owners to demand low‑carbon concrete options. The practical checklist for 2026 includes mapping applicable local approvals; planning for certification timelines; engaging with standards bodies to fast‑track test methods where gaps exist; and structuring procurement to capture carbon‑value benefits under ETS or border mechanisms.

Scenario planning — three actionable paths for 2026

- Conservative adoption: Prioritize niche and non‑structural uses (shotcrete, paving, fireproofing). Focus investments on pilot projects and specification wins; defer large plant build‑outs until precursor supply is proven.

- Base case (our central forecast): Scale regional production hubs with hybrid models (central batching + mobile mixing) and secure long‑term precursor contracts. Invest in certification and supply partnerships; pursue public‑sector infrastructure tenders where lifecycle advantages are valued.

- Aggressive expansion: Vertical integration of precursor sourcing, build multiple regional plants, and pursue licensing of proven formulations to accelerate market coverage. This path suits players with balance‑sheet capacity and access to stable precursor streams.

How to convert this preview into action within 90 days

- Week 1–2: Executive briefing and gap analysis — validate internal targets against our market model and identify immediate procurement risks.

- Week 3–6: Supplier due‑diligence and pilot scoping — issue tailored RFIs using PW Consulting checklists; select 1–2 pilot sites with realistic permitting paths.

- Week 7–10: Certification and QA roadmapping — engage third‑party labs and begin parallel testing for structural, fire and durability performance to align tender specifications.

- Week 11–12: Commercial launch plan — finalize offtake agreements, pricing strategies, and a 12‑ to 24‑month rollout schedule linked to key regulatory milestones.

Next steps — where to get the full intelligence

This strategic preview demonstrates how our Green Geopolymer Concrete Market Report is built to move teams from concept to procurement to project execution. The full report contains the granular segmentation tables, interactive revenue dashboards, company scorecards, full scenario model inputs, and downloadable procurement templates that firms will need to finalize 2026 budgets and vendor strategies. To access the complete study and our proprietary financial model, please visit PW Consulting’s report page or contact our industry practice for a tailored briefing.

PW Consulting’s analytics and field teams continue to monitor precursor markets, certification milestones and large‑scale deployments. For decision‑makers preparing capital allocations or entering supplier alliances in 2026, our report is structured as a working playbook — not a desk study — designed to shorten implementation timelines and de‑risk early commercial programs.

For detailed analysis of this topic, please visit the official page:Green Geopolymer Concrete Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com