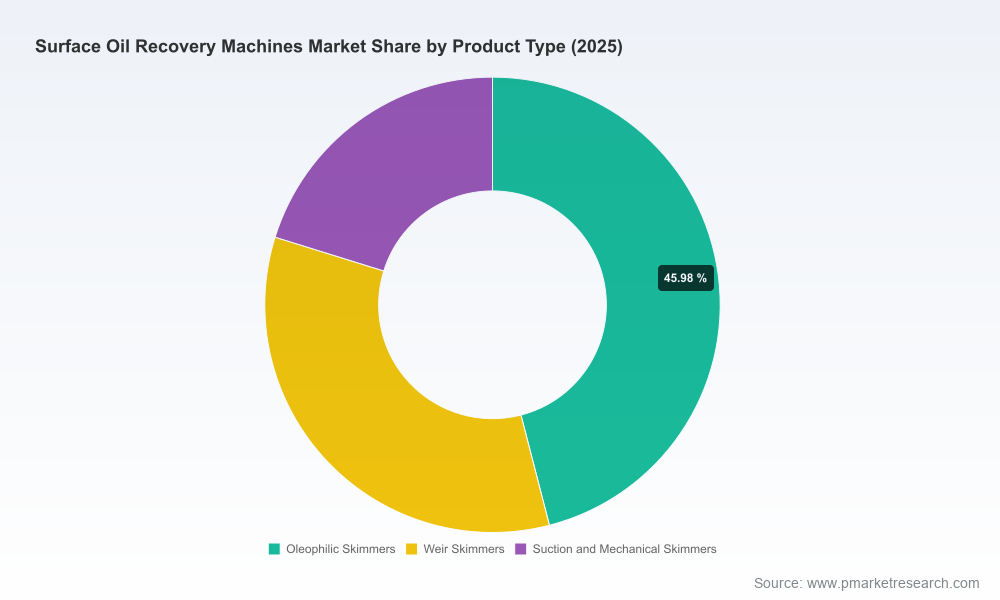

Surface Oil Recovery Machines Market: Strategic Pathways for 2026 — PW Consulting Preview

Executive preview

PW Consulting’s latest market study on Surface Oil Recovery Machines delivers an evidence-based roadmap for executive decision-making in 2026. Grounded in a six‑year historical series and a seven‑year forecast horizon, the study translates market dynamics into practical choices for product strategy, procurement, operations and M&A. This preview distills the report’s strategic value — demonstrating the analytical depth clients can expect — while preserving proprietary segment-level detail to encourage full‑report engagement.

Surface Oil Recovery Machines Market

Market snapshot: growth trajectory and macro view

The global surface oil recovery machines market has shown steady expansion from 2020 through the report’s base year of 2025, and our model projects continued growth through 2032. Using USD‑denominated revenue measures, the market expanded notably across the historical period and is projected to register a mid‑single digit compound annual growth rate (CAGR) over the forecast. Under our central case, the market moves from a strong 2025 base into a sustained upcycle driven by regulatory reinforcement, ongoing offshore and industrial activity, and a growing emphasis on environmental risk mitigation. For executives, the headline numbers validate both defensive investments (compliance, fleet readiness) and selective growth capital deployment (product innovation, aftermarket services).

Surface Oil Recovery Machines Market

Why this matters for 2026 decision cycles

- CapEx prioritization: Procurement timelines for new skimmer fleets and modular recovery systems must align with multi‑year replacement cycles. The market trajectory supports planned renewals and targeted expansion where strategic exposure to spill risk is material.

- Regulatory preparedness: Recent and ongoing regulatory activity — including extended EPA conditional listings for response products, sustained oversight under legacy oil pollution statutes, and updated interagency coordination — will shape minimum acceptable performance and procurement specs by 2026.

- Supply chain and input costs: Raw material price movements (for example, modest shifts in steel inputs) are a recurring consideration; manufacturers with flexible sourcing and alternative material strategies will preserve margins and shorten lead times.

- Service economics: Aftermarket, rapid‑deployment logistics, and performance guarantees are emerging as differentiators. Buyers should model total cost of ownership (TCO) not upfront price alone.

Report composition — what operational leaders will use

Our full report is constructed to be immediately operational for procurement teams, plant managers, and corporate strategists. Key deliverables include:

Surface Oil Recovery Machines Market

- Proprietary market model (2020–2032) with scenario and sensitivity toggles to quantify implications of oil price volatility, regulatory tightening, and incident frequency.

- Decision frameworks for CapEx vs. rental/leasing tradeoffs, incorporating recovery efficiency, deployment time, and lifecycle service costs.

- Supplier evaluation templates and a standardized RFP checklist designed specifically for surface recovery equipment procurement.

- Field performance benchmarks linked to test protocols and real‑world trial data, enabling side‑by‑side comparisons across technology types without exposing proprietary market share data.

- Playbooks for aftermarket commercial models (spare parts, field service, remote diagnostics) and for structuring regional inventory footprints to reduce response times.

Competitive landscape: strategic positioning of leading providers

The market structure is best characterized as fragmented with scope for selective consolidation. The five largest suppliers account for under one‑third of market revenue, leaving substantial whitespace for differentiated players to scale through innovation, service excellence, or focused partnerships.

Key industry participants covered in the study demonstrate differentiated go‑to‑market approaches:

- Elastec (USA) — Recognized for a broad portfolio of skimmers and surface recovery systems, Elastec emphasizes compliance and quality systems that appeal to response agencies and large operators seeking ASTM/ISO aligned equipment.

- DESMI (Denmark) — A global OEM with strong offshore and nearshore credentials; its position is reinforced by proven deployments in major response operations and a service network that supports long‑range mobilization.

- Vikoma (UK) — Notable for rapid‑deployment units and recent product introductions that expand adaptability across oil types. Vikoma’s roadmap signals a focus on modularity and quicker field readiness.

- Lamor (Finland) — Differentiates on high‑end environmental performance, including systems designed for harsh and Arctic conditions — a strategic edge for polar and high‑latitude operators.

- Abanaki and other industrial specialists (USA) — These firms concentrate on belt, tube and industrial skimmers for process and wastewater applications, where integration into facility control systems and low TCO matter most.

Across the competitive set, recent tactical moves underscore two clear themes: product refinement for broader oil compatibility (including low‑sulfur fuel oils) and an emphasis on lightweight, higher‑throughput skimmers optimized for rapid response. Notable announcements and developments are summarized in the full report and include product launches and industry test protocol advances that will recalibrate buyer expectations.

Industry signals and near‑term disruptors

- Protocol standardization: The adoption of advanced skimmer test protocols by industry and regulators will raise the bar for performance claims and influence procurement specifications. Expect buyers to require lab and field validation aligned with recognized protocols.

- Product innovation: Emergent models emphasize higher recovery rates, modularity, and lower logistics weight. Vendors introducing universally deployable skimmers that handle a range of viscosities will gain share in multi‑use fleets.

- Regulatory tightening: Continued enforcement under legacy oil pollution statutes and facility response planning requirements means operators must demonstrate both capability and compliance — not just plan documents.

- Material and input cost trends: Mild volatility in steel and other raw materials calls for flexible bill‑of‑materials strategies; vertically integrated manufacturers will have an edge if they can smooth procurement cycles.

Strategic recommendations for 2026

Decision makers should synthesize market signals into a coherent set of actions for the coming planning cycle. PW Consulting recommends a three‑pronged approach:

- Portfolio rationalization: For OEMs, prioritize development of adaptable platforms that reduce SKU complexity while expanding cross‑segment applicability (marine, industrial, wastewater). Costly niche product lines with limited TAM should be divested or licensed.

- Service and logistics as competitive moat: Build rapid‑response hubs, standardized spares kits, and digital monitoring to deliver guaranteed time‑to‑containment metrics. For operators, specify these service SLAs in procurement contracts.

- Regulatory‑led product alignment: Align R&D and certification roadmaps with emerging test protocols and compliance requirements. Early movers who certify equipment against recognized test standards will shorten sales cycles with institutional buyers.

M&A and partnership implications

The fragmented market profile creates attractive conditions for bolt‑on acquisitions and strategic alliances. Buyers should evaluate targets that provide:

- Complementary channel access (regional service networks, coastal vs. inland presence).

- Proprietary test‑validated technologies or lightweight high‑throughput skimmers that broaden an acquirer’s use cases.

- Aftermarket platforms or digital telemetry solutions that can be cross‑sold to existing equipment bases.

How to use the full PW Consulting report in 2026 planning

The full report is structured to be a working tool in boardrooms and procurement committees: downloadable financial models, procurement checklists, validated vendor profiles and scenario playbooks are all included. Stakeholders can run bespoke sensitivity analyses — for example, testing the impact of faster regulatory adoption of new skimmer protocols, or a spike in incident frequency — to quantify capex timing and service network requirements.

Closing note and next steps

PW Consulting’s Surface Oil Recovery Machines Market report converts observed trends and regulatory signals into actionable strategy. For leaders setting budgets and defining procurement strategy in 2026, the study clarifies where to invest for resilience and where to pursue growth. To access the full dataset, vendor benchmarking, and the interactive market model that underpins our conclusions, please refer to the full report available from PW Consulting — the only way to unlock the proprietary segment detail and granular scenario outputs referenced in this preview.

For detailed analysis of this topic, please visit the official page:Surface Oil Recovery Machines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com