Crosslinking Agents Market to Reach USD 4.74 Billion by 2034 Amid Rising Demand for Advanced Polymers

Networking |

2026-06-29 10:01:04

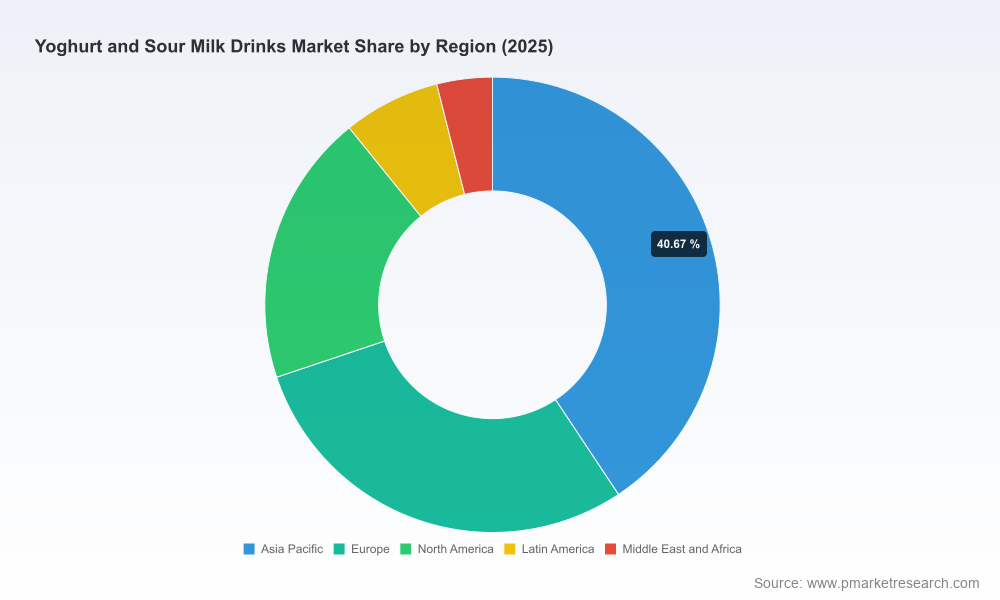

PW Consulting’s latest market intelligence on the global yoghurt and sour milk drinks sector establishes a clear strategic compass for corporate leaders planning 2026 budgets and 3–7 year roadmaps. Our analysis shows the industry expanded from roughly USD 104 billion in 2020 to an estimated USD 134.25 billion in 2025, and is projected to reach approximately USD 192.7 billion by 2032, representing a compound annual growth rate (CAGR) of 5.3% over the 2026–2032 forecast period. Market concentration is moderate: the top-three firms control about one-third of the market, and the top-five approach 42% — a dynamic that shapes both competition and consolidation opportunities.

Yoghurt And Sour Milk Drinks Market

Timing: 2026 will be a pivot year as regulatory resets, raw material volatility and changing consumer health preferences converge. Companies that align R&D, supply-chain hedging and go-to-market execution in the first half of 2026 will capture outsized share in the second half and beyond.

Yoghurt And Sour Milk Drinks Market

Clarity: our projections translate headline growth into practical implications for capacity planning, SKU portfolios and channel investment — enabling CFOs to stress-test capex and working-capital scenarios against realistic demand trajectories.

Yoghurt And Sour Milk Drinks Market

Prioritization: with a mid-single-digit CAGR at the category level, margins and topline will be driven by product mix, premiumization, and cost-to-serve improvements rather than pure volume — critical for portfolio rationalization choices in 2026.

Top-down market sizing and three scenario forecasts (baseline, upside, downside) with roll-ups to company-level implications — built for board-level stress-testing.

Commercial playbooks for 2026: SKU rationalization templates, promotional elasticity models, and channel allocation frameworks that translate forecasts into retail activation plans.

Supply-risk maps and input-cost scenarios: milk powder and other key input sensitivities linked to margin-impact matrices and recommended hedging actions.

Regulatory impact assessments and compliance roadmaps for major jurisdictions — including label, front-of-pack nutrition and safety obligations — with ready-to-use checklists for product relabeling and reformulation timelines.

M&A and JV screening frameworks: target scoring criteria, valuation sensitivities and rapid-diligence checklists tailored to both strategic acquirers and financial sponsors.

Innovation scorecards and go-to-market templates for probiotic, high-protein, low-sugar and plant-based variants — prioritized by commercial viability and execution complexity.

The market combines global incumbents, regional champions and fast-moving challengers. Major players with broad international footprints and diversified portfolios continue to set the pace for innovation and retail access. Representative profiles include:

Danone (Paris, France; https://www.danone.com) — a global leader with a deep portfolio in fermented dairy and a strong recent focus on gut-health propositions.

Lactalis (Laval, France; https://www.lactalis.fr) — a large-scale manufacturer with both branded and private-label strength across multiple markets.

Chobani (New York, USA; https://www.chobani.com) — strong in Greek-style and protein-forward drinkable formats, leveraging US retail leadership for international expansion.

Yakult Honsha (Tokyo, Japan; https://www.yakult.co.jp) — specialized probiotic sour milk drinks with an asset-light, distribution-focused model in many Asian markets.

Fage, Nestlé, Mondelez, Arla Foods, General Mills, Stonyfield, Siggi’s, Forager Project — each brings differentiated strengths (authenticity, scale, branding, regional reach, organic credentials, skyr expertise, plant-based innovation) that define effective competitive plays in specific channels and consumer segments.

Recent corporate moves illustrate the intensifying focus areas: Danone’s 2025 probiotic launch, Chobani’s protein-enriched drinkable range, Yakult’s capacity expansion in South Asia, Arla’s push into plant-based fermented drinks, and Lactalis’ low-sugar line-up. These tactical bets highlight two simultaneous trends: product health premiumization and diversification of formulation platforms.

Raw material and input cost pressure: milk powder volatility is an active margin risk. Procurement teams must adopt multi-supplier strategies and scenario-based pricing clauses. Our report includes an input-cost sensitivity model that maps raw-material moves to gross-margin outcomes and suggests hedging and cost-recovery thresholds.

Regulatory resets: newer front-of-pack nutrition regimes and updated nutrition labeling in major markets are forcing reformulation, pack redesign and marketing recalibration. These changes create both compliance costs and a market opportunity: reformulated, transparently labeled products can win shelf space and premium positioning.

Trade and tariff frictions: evolving tariffs and trade policy shifts alter routing and sourcing economics. Companies with flexible production footprints and regional co-packing arrangements will have a competitive edge in 2026.

Quality and recall risk: recent recalls underscore the need for faster quality-traceability systems and crisis response playbooks — not just as compliance, but as brand-protection investments.

Channel and convenience shifts: e-commerce and convenience-led formats continue to change cost-to-serve dynamics. The report quantifies break-even points for channel investments and offers retailer-negotiation levers for promotional ROI improvements.

Prioritize margin-led assortment: With category growth moderate, resource allocation should favor high-margin, low-complexity SKUs that support premium pricing or subscription models.

Invest selectively in health-led innovation: Probiotic and protein-forward offers are where the top-line leverages brand strength. However, new SKUs should pass a commercial viability gate that includes retailer acceptance probabilities and production scalability tests (templates included in the report).

Hedge and regionalize supply chains: Adopt modular sourcing and near-shore co-manufacturing to mitigate input-price shocks and tariff exposure. The report’s supplier-risk heat-map helps prioritize vendor diversification.

Comply proactively with labeling reforms: Rework packaging and marketing calendars to align with front-of-pack and nutrition-label deadlines, using our relabeling checklist to avoid lost shelf windows.

Strengthen quality-as-differentiator: Digital traceability, faster testing protocols, and transparent consumer communications can turn compliance investments into trust assets.

Optimize channel economics: Rebalance promotions away from deep discounting toward value-adds (bundles, subscriptions, targeted sampling) to protect margins while sustaining velocity.

Use M&A as an accelerant: With mid-tier consolidation and differentiated regional brands available, bolt-ons that add technical capability (for example, probiotic strains) or direct-to-consumer channels should be prioritized over scale-for-scale deals.

Risk: A persistent spike in input costs could compress margins materially in a low-price-elasticity segment. Our downside scenario models the impact and identifies trigger points for price recovery or promotional cutbacks.

Opportunity: Reformulation to meet new nutrition labeling can unlock premium shelf positioning — early movers typically secure superior in-store facings and higher consumer trust scores.

Operational leverage: Companies that reduce SKU complexity while investing in a few high-potential SKUs see disproportionately higher increases in fill-rate and on-shelf availability — a tactical lever with immediate 2026 impact.

Feed the baseline and scenario forecasts into your 2026 demand-planning models to set capex and working-capital limits under different input-cost paths.

Run the PW Consulting SKU rationalization template with commercial and manufacturing leads to identify the top 20% of SKUs driving 80% of margin risk and prioritize delistings or reformulations accordingly.

Use the regulatory checklists to set a 90-day timeline for label and ingredient compliance in high-impact markets.

Initiate supplier contingency contracts and test co-manufacturer agreements to cut lead times and reduce single-source exposure before the next seasonal surge.

The yoghurt and sour milk drinks sector is neither a low-margin commodity race nor a fast-scaling frontier market — it is a mid-growth arena where execution discipline, targeted innovation and regulatory-savvy commercialization determine winners. Our 2026-focused guidance transforms high-level forecasts into board-ready actions: invest where structural growth and margin expansion align, de-risk supply and labeling exposures, and use M&A and channel plays to accelerate capability gaps.

PW Consulting’s full market study contains the granular matrices, worksheets and scenario models referenced here — the practical instruments corporate teams need to translate the projected USD-level growth and 5.3% CAGR into measurable improvements in revenue, margin and risk posture. For access to the full dossier and the proprietary Excel models, visit the PW Consulting report page or contact our industry practice to schedule a bespoke briefing.

For detailed analysis of this topic, please visit the official page:Yoghurt And Sour Milk Drinks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com