Electronic Flight Bag Industry Analysis: Market Size, Share & Forecast to 2035

Other |

2026-02-23 10:01:54

PW Consulting's latest market study on Dust Collectors for Mining provides a focused, decision‑ready view for executives planning capital investments, compliance programs, and supplier strategies in 2026. The research synthesizes multi‑year market sizing, regulatory shifts, cost‑pressure dynamics, and a vendor‑level competitive assessment — delivering a practical compass for organizations that must balance worker safety, operational continuity, and total cost of ownership in increasingly stringent operating environments.

Dust Collectors For Mining Market

Mining operators and their equipment suppliers face a narrow window to convert regulatory imperatives into defensible business cases. Our analysis shows the market has expanded steadily from the early 2020s and reached a substantial base by 2025, with a trajectory that takes it higher through the forecast horizon. PW Consulting projects continued expansion across 2026–2032 at a compound annual growth rate of 5.35% — a pace that signals both enduring demand and intensifying competition for retrofit opportunities, aftermarket services, and engineered solutions.

Dust Collectors For Mining Market

For 2026 specifically, three practical implications flow from our macro findings: (1) near‑term capital allocation should prioritize compliance‑critical engineering controls that materially reduce respirable crystalline silica exposures; (2) procurement teams should adopt lifecycle costing that captures service, filter media, and downtime risk; and (3) product roadmaps must emphasize modularity and digital condition monitoring to shorten lead times and lower operational risk.

Dust Collectors For Mining Market

Measured expansion: The market expanded markedly from the early 2020s, establishing a robust installed base by the 2025 reporting year. That installed base provides a growing addressable aftermarket and retrofit opportunity in the coming three years.

Regulatory impetus: The Mine Safety and Health Administration (MSHA) finalized standards that set a uniform permissible exposure limit (PEL) of 50 μg/m³ and an action level of 25 μg/m³ for respirable crystalline silica, with compliance timelines that made engineering controls the primary pathway to conformity. This regulatory posture elevates dust collectors from discretionary to mission‑critical assets in many operations.

Cost and materials environment: Volatility in inputs used for heavy‑gauge fabrication and filter media has compressed supplier margins and influenced supplier selection criteria. Procurement teams must now weigh short‑term price volatility against long‑term availability and supplier resilience when evaluating bids.

Technology and service convergence: Expect rising demand for integrated solutions — combining engineered capture (hooding, transfer point mitigation), high‑efficiency filtration, explosion protection, and predictive maintenance enabled by sensors and analytics. Buyers are rewarding suppliers who can demonstrate a measurable reduction in exposure levels and lifecycle cost.

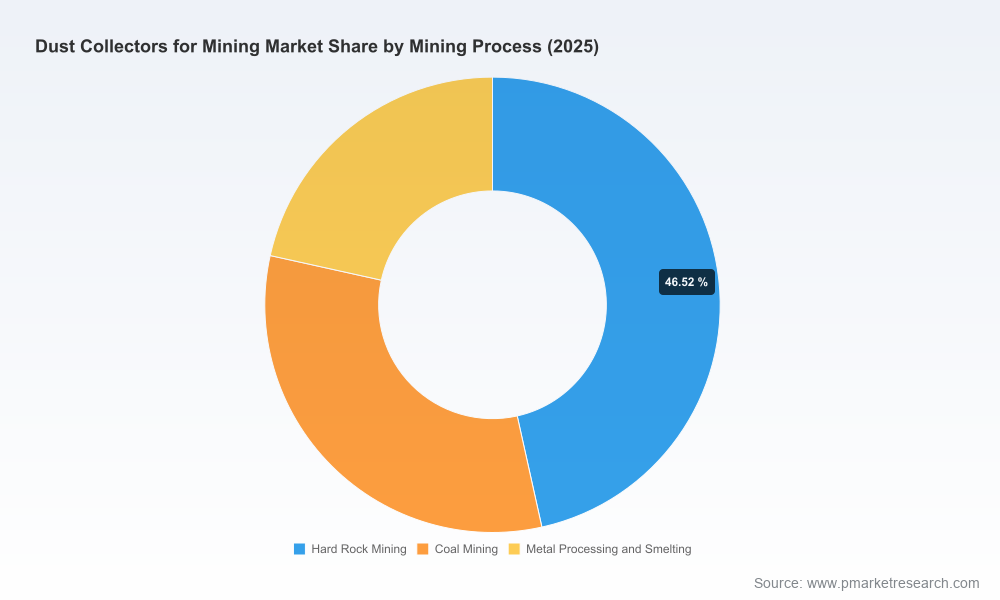

The dust collection market remains moderately fragmented: concentration levels indicate that the top three suppliers do not dominate the majority of the opportunity, and the top five capture under half the market, leaving substantial room for specialist vendors, systems integrators, and new entrants focusing on niche capabilities. This structure creates procurement leverage for large buyers and opportunities for consolidation-minded investors.

From our benchmarking of incumbent and specialist vendors, several strategic patterns emerge:

Vertical specialization — Established manufacturers with product families tailored to mining environments retain an advantage on turnkey installs and warranty risk. Their propositional strengths include validated baghouse/cartridge architectures, explosion‑mitigated skids, and service networks that reduce downtime risk.

Modular and heavy‑duty offerings — Vendors offering modular, field‑serviceable units and ruggedized construction are favored in operations exposed to abrasive dusts and harsh climates. This reduces mobilization time for retrofits and simplifies spares strategies.

Specialist engineering houses — Firms focused on application engineering (hood design, pneumatic conveying integration, scrubber solutions) win where performance guarantees and measurable dust capture rates are contractually required for compliance.

Service and consumables — The aftermarket (filters, seals, pulse systems, repairs) is an increasingly decisive profit pool; suppliers offering bundled service agreements and remote condition monitoring lock in recurring revenue and improve customer switching costs.

Notable vendor behaviors observed in 2025–2026 include refreshed trade show engagement with mining audiences, product promotions targeting transfer points and conveyor dust control, and heightened marketing of solutions designed to meet the newly enforced silica PEL. These activities signal suppliers are repositioning portfolios toward compliance‑oriented offerings and rapid turnkey deployment.

Compliance triage: Conduct a prioritized exposure audit tied to MSHA thresholds. Rank facilities by exposure risk and retrofit urgency to sequence capital projects for 2026. Engineering controls must be first in the pyramid of mitigation measures.

Lifecycle economic modeling: Replace capex‑only comparisons with total cost of ownership models that include filter replacement cadence, energy consumption, downtime, and compliance risk. Use scenario analysis to stress test procurement outcomes against steel and filter media price swings.

Specification discipline: Standardize technical specifications across sites for modular units and ensure explosion protection, access for maintenance, and digital I/O for condition monitoring are non‑negotiable clauses.

Supplier governance: Create multi‑year service contracts with KPIs that tie payments to performance (exposure reductions, uptime). Where possible, structure deals with options for incremental modular expansion to preserve capex flexibility.

Innovation scouting: Invest in pilot programs for novel media or compact filtration systems that promise energy or footprint reductions; these pilots can be fast pathways to differentiated supplier agreements.

PW Consulting’s study goes beyond high‑level commentary. The report is designed as an executable toolkit for 2026 planning cycles and includes:

Proprietary market sizing and a transparent forecast model covering the base year and the full 2026–2032 horizon, enabling sensitivity testing against regulatory and input‑cost scenarios.

Supplier benchmarking that assesses technical coverage, service footprint, modular capabilities, and commercial models — enabling RFP shortlists aligned to buyer priorities.

Procurement playbooks and specification templates that accelerate bid processes while preserving compliance and lifecycle economics discipline.

Operational case studies and retrofit decision matrices that highlight when to pursue targeted containment, when to invest in centralized baghouse systems, and how to prioritize conveyors, crushers, and transfer points.

Regulatory compliance toolkit including checklists and a mapping of engineering controls to MSHA obligations, plus a health surveillance and documentation playbook for operations that must demonstrate compliance.

Scenario and sensitivity analyses that quantify the impact of input‑cost shifts and regulatory enforcement timing on project NPV and payback windows.

M&A and partnership screening criteria for investors seeking targets in manufacturing, filtration media, or aftermarket servicing that can be consolidated to capture scale economies.

Operators should treat this study as the starting point for a three‑tier program: immediate compliance triage, medium‑term capex and service contracting, and long‑term modernization tied to digital and energy objectives. For investors and strategic buyers, the report identifies pockets where scale, proprietary media, and service footprints create defensible margins — and where fragmented supply gives room for bolt‑on consolidation.

Critically, decisions in 2026 will be made under compressed timelines: compliance drivers shorten procurement cycles, while the economics of retrofit versus replacement demand fast, defensible modeling. This study equips decision‑makers with the templates, benchmarks, and scenario tools required to move from assessment to execution without sacrificing rigor.

PW Consulting’s Dust Collectors for Mining Market report is intentionally structured to demonstrate analytical depth while preserving the detailed segment tables, vendor revenue shares, and granular regional splits for authorized report access. For procurement leads, operations managers, and M&A teams preparing 2026 plans, the full dataset and vendor scorecards are indispensable to convert strategic intent into executable projects.

Contact PW Consulting to access the complete report, request a briefing, or commission a tailored workshop that applies the findings directly to your asset portfolio and compliance roadmap.

For detailed analysis of this topic, please visit the official page:Dust Collectors For Mining Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com