Cloud POS Market: Analyzing the Competition Landscape and Its Implications for Growth, Forecast by 2033

Networking |

2026-03-11 08:02:28

PW Consulting’s new market study on Phosphate Conversion Coating Services is designed as a decision-grade intelligence asset for executives planning capital allocation, supply-chain resilience, and technology roadmaps in 2026. Grounded in a five-year historical analysis (2020–2025) and an actionable forecast window (2026–2032), the report synthesizes market sizing, competitive structure, regulatory pressure points, and technology trajectories into practical recommendations.

Phosphate Conversion Coating Services Market

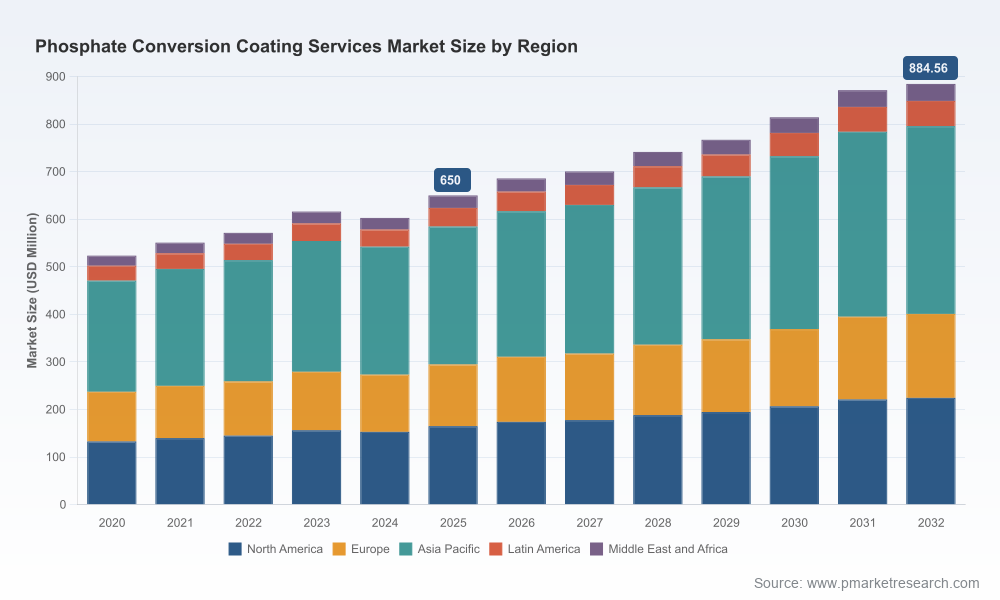

The market demonstrated resilient expansion through the 2020–2025 period, growing from roughly USD 523 million in 2020 to approximately USD 650 million in 2025. Our base-case projection anticipates continued expansion to the high hundreds of millions by 2032, representing a steady compound annual growth rate of 4.5% over the 2026–2032 forecast horizon. These macro signals—solid baseline demand plus steady growth—create an environment where targeted investments and operational improvements can deliver outsized returns for the right players.

Phosphate Conversion Coating Services Market

Actionable foresight: The combination of a validated historical series and scenario-based forecasts allows procurement, manufacturing, and corporate strategy teams to stress-test capital projects and supplier contracts against realistic demand paths through 2032.

Phosphate Conversion Coating Services Market

Operational playbooks, not just numbers: Beyond headline sizing, the study surfaces dozens of practical levers—process optimizations, specced quality controls, and vendor selection criteria—that reduce the time from insight to execution.

Regulatory and input-risk layering: The report integrates regulatory scenarios (e.g., tighter heavy-metal controls and no-rinse expectations) with raw-material exposure analysis so decision-makers can quantify and hedge margin risk in 2026 and beyond.

Competitive and consolidation signals: Fragmentation metrics and supplier capability maps identify where consolidation, partnerships, or capacity expansion will generate strategic advantage.

Comprehensive market model: A bottom-up revenue model reconciled to market activity across 2020–2025, with base, upside, and downside scenarios for 2026–2032 tied to macro and end-market demand.

Demand-driver diagnostics: Elasticity assessments for automotive, aerospace, industrial, and other end-use sectors; sensitivity matrices showing the impact of automotive production cycles, capital-spend shifts, and retrofit activity on serviceable demand.

Supplier operations intelligence: Benchmarked processing capabilities (tank sizes, rack vs. barrel throughput, pre/post treatment stacks), quality compliance profiles, and labor/capex intensity estimates to inform make-versus-buy and greenfield decisions.

Regulatory & sustainability playbook: Scenario templates for implementing low-zinc, no-rinse, and low-temperature technologies, including estimated process change timelines, compliance checkpoints, and supplier selection filters.

Commercial due-diligence modules: Valuation triangulation, potential bolt-on targets, and integration risk checklists for acquirers seeking to consolidate in a fragmented market.

Risk heatmap and mitigation plans: Supply-chain mappings for critical inputs, logistics stress tests, and contingency approaches covering short-term raw-material shocks and longer-term regulatory pivots.

End-market durability: Phosphate conversion coatings remain a core pre-treatment for corrosion protection, paint adhesion, and wear resistance across heavy-duty applications. Continued investment in automotive, aerospace, and industrial equipment underpins baseline demand.

Incremental technology adoption: Innovations that simplify or eliminate process steps—single-step cleaners, phosphate-free pretreatments, and more efficient bath chemistries—are moving from lab to line. These improvements reduce total cost of ownership for job shops and captive plants and create a product-differentiation pathway for chemical suppliers.

Regulatory pressure: Tighter environmental rules in key markets are accelerating interest in low-sludge, low-metal, and no-rinse processes. This raises compliance costs for legacy plants but creates demand for retrofit services, licensed chemistries, and outsourced finishing solutions.

Input volatility and supply risk: Feedstock dynamics and regional cost disparities affect margin reliability for service providers. Our analysis flags where processing cost increases are likely to be absorbed versus passed through to end customers under varying contract structures.

The phosphate conversion coating services market is materially fragmented (our concentration analysis shows moderate share held by the top firms), leaving substantial room for operational excellence and M&A-driven scale. Below we synthesize the competitive posture of representative providers and the strategic moves they indicate for the market.

Nitretex (United States) — Strengths: large-tank capacity enabling full-production throughput and custom part processing; clear foothold in oil & gas, automotive, aerospace, and firearms. Strategic implication: Nitretex’s large-scale capability positions it to compete for captive outsourcing relationships and high-volume contracts where throughput and consistency matter.

Keystone Corporation (United States) — Strengths: specification-driven processing (MIL-DTL, AMS), focus on manganese phosphate for bearings and fasteners. Strategic implication: Firms with military and aerospace specification compliance can command price premiums and more sticky contracts; partnerships with defense OEMs remain a durable niche.

K&L Plating Company, Inc. (Lancaster, PA) — Strengths: service orientation toward defense and critical manufacturers, zinc phosphate specialization. Strategic implication: Localized service excellence and compliance expertise make regional plays viable for operators unable to match national scale.

Cor-Pro Systems, Inc. (Houston, TX) — Strengths: targeted protection services for refineries and petrochemical complexes. Strategic implication: Industry-specialist providers reduce client switching risk and can build multi-year maintenance and inspection contracts around finishing services.

Imagineering Finishing Technologies (United States) — Strengths: full-service finishing, rack and barrel processing, pre/post-treatment integration. Strategic implication: End-to-end offerings capture more wallet share per part and are attractive to OEMs seeking single-source finishing partners.

Valence Surface Technologies (United States) — Strengths: aerospace and defense focus with high-spec zinc phosphate finishes. Strategic implication: Ability to meet tight aerospace quality metrics serves as a high-barrier niche that supports margin resilience.

Pioneer Metal Finishing (United States) — Strengths: manganese and phosphate variants for wear-critical components. Strategic implication: A focus on wear and high-torque applications aligns with aftermarket and industrial maintenance business models that provide recurring revenue.

Recent moves by large chemicals players—examples include single-step cleaner & coater launches and exhibition showcases of phosphate-free pretreatment systems—signal a maturing of alternative chemistries that could reconfigure the supplier hierarchy over the medium term. For service providers, early testing partnerships with chemistry innovators will be a defensible way to retain relevancy without bearing full development cost.

Prioritize retrofit and compliance investments: Operators should sequence investments to meet tightening environmental requirements while optimizing throughput; target retrofits that also reduce waste handling and labor intensity to accelerate payback.

Lock in feedstock resilience: Establish multi-sourced supply arrangements for critical chemicals and consider hedging where contractual pass-through is difficult. Procurement teams must map chemical exposure across facilities to prioritize security-of-supply actions.

Differentiate through service integration: Firms that bundle inspection, pre-treatment, coating, and quality-reporting can extract higher lifetime value from OEMs—particularly in aerospace and defense markets where traceability is paramount.

Pursue targeted M&A and partnerships: With market concentration still moderate, disciplined acquisitions of regional specialists can accelerate access to new end markets and create scale for chemistry negotiation leverage.

Invest in proof-of-concept for alternative chemistries: Pilots with single-step or phosphate-free systems reduce long-term regulatory risk and create marketing differentiation, but must be run under real production conditions to validate adhesion and corrosion metrics.

Scenario-based capital allocation: Use the report’s three demand scenarios to stress-test greenfield vs. brownfield decisions and to align CAPEX with payback expectations under regulatory change.

Commercial negotiation: Deploy supplier capability scorecards and cost-to-serve benchmarks from the report to renegotiate long-term service agreements or to run a targeted RFP.

M&A diligence: Leverage the valuation triangulation and integration checklist as a short-listing tool for bolt-ons that enhance technical capability or regional reach.

Operational excellence: Adopt the process KPIs and retrofit sequencing playbook to reduce downtime and improve compliance outcomes during transitions to new chemistries or equipment.

As the phosphate conversion coating services market moves from recovery into steady expansion—anchored by a roughly mid-single-digit CAGR and a multi-hundred-million-dollar base—2026 represents a pivotal year for strategic positioning. Regulatory tightening, chemistry innovation, and persistent demand from core end markets create both risk and opportunity. PW Consulting’s report turns dispersed signals into prioritized actions: from procurement hedges and retrofit sequencing to capability-driven M&A and pilot programs for alternative treatments.

For executives preparing budgets, negotiating supplier contracts, or evaluating acquisition targets in 2026, this report functions as a practical toolkit: rigorous market sizing and scenarios, hands-on operational guidance, and a competitor intelligence set that highlights where scale, specialization, and technology will determine winners. To access the full dataset, detailed segmentation tables, and supplier scorecards that underpin these strategic recommendations, consult the PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Phosphate Conversion Coating Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com