Solid State Transformers Market Dynamics: Key Drivers and Restraints

Other |

2026-05-14 11:53:37

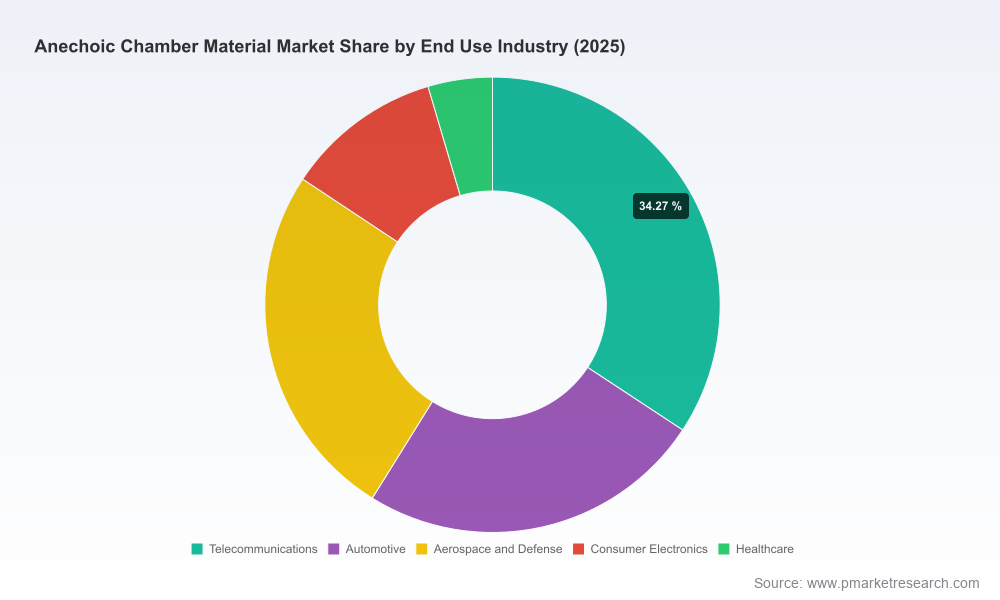

PW Consulting’s new industry brief on the Anechoic Chamber Material market positions the sector as a stable-growth, technically intensive segment of the broader EMC, RF and acoustic testing ecosystem. The market demonstrates clear expansion from the early 2020s into the mid-decade: our base-year assessment (2025) values the global market in the high hundreds of millions of USD, following a steady rise from 2020, and we forecast continued growth through the 2026–2032 horizon at a compound annual growth rate of approximately 6.5%. By 2032 the market approaches the low‑to‑mid billions threshold in nominal terms, supported by ongoing investment in telecom, automotive electrification, aerospace/defence modernization and compliant test infrastructure.

Anechoic Chamber Material Market

Demand architecture is shifting from one-off chamber projects toward recurring refurbishment, modular upgrades and materials-as-a-service considerations. This changes procurement calculus: lifetime performance, maintainability and certification stability are now as important as unit price.

Anechoic Chamber Material Market

The materials layer — pyramidal polymer absorbers, ferrite tiles, hybrid combinations and conductive shielding substrates — is where margin, risk and differentiation concentrate. Material choice impacts chamber performance across frequency bands, fire and chemical safety compliance, supply-chain exposure and total cost of ownership.

Anechoic Chamber Material Market

Macro supply dynamics are non-trivial: polyurethane-based absorbers rely on feedstocks such as TDI and specific polyols. Recent supply tightness has shown how upstream chemistry constraints transmit into absorber lead times and cost volatility. Procurement teams need hedging and qualification pathways for alternate material chemistries.

Regulatory and safety compliance is an inflection point. Fire performance standards and chemical-content regulations (e.g., those aligned with ASTM, REACH and RoHS frameworks) are now integral to specification, not optional add-ons. Certification status can be a procurement disqualifier or a market differentiator.

PW Consulting’s market study is designed as an operational playbook as much as a market map. Key practical deliverables included in the full report are:

Supplier selection framework: weighted criteria for performance, certification, lifecycle cost, retrofit capability and geographic responsiveness, with executable RFQ templates tailored to absorbers and hybrid assemblies.

Materials risk matrix: scenario-based impact assessments for TDI shortages, tariff shocks, fire-code tightening and the introduction of novel polymer or PP-based absorber formulations; mitigation levers and trigger points for action.

Specification checklists: test and acceptance protocols (electromagnetic and acoustic), documentation required for compliance sign-off, and a verification pathway for hybrid ferrite/foam systems used in high-power or low-frequency testing.

CapEx vs. OpEx decision guide: when to build new bespoke chambers, when to retrofit absorbers, and when to opt for modular, relocatable solutions; includes sensitivity tables and payback-phasing heuristics that procurement and engineering teams can apply.

Commercial negotiation playbook: contracting language for long-lead absorbers, warrantee & replacement clauses for absorber panels, and shared-risk constructs for large multi-site programs.

The anechoic absorber market is populated by established specialty manufacturers and systems integrators whose differentiation is rooted in materials science, manufacturing scale, testing know-how and installation services. Leading names have built recognizable capability bundles:

Companies with deep absorber R&D and foam-formulation expertise deliver broadband pyramidal and convoluted absorbers optimized for EMC and antenna testing. Their value proposition centers on RF performance tuning and product family depth.

Systems integrators combine absorber technologies with turnkey chamber engineering, offering clients single-vendor responsibility for shielded rooms, absorbers, and on-site commissioning — a compelling model for defense, aerospace and large OEMs seeking certainty of outcome.

Manufacturers specializing in ferrite-based absorbers or hybrid solutions compete on immunity and low-frequency performance, and on durability in high-power test rigs where polymer-only solutions struggle.

Representative players profiled in our analysis include long-standing absorber specialists, RF and EMC systems integrators, acoustic chamber manufacturers and electronics materials firms. Each profile evaluates manufacturing footprint, product portfolio (polymer pyramids, ferrite tiles, hybrid assemblies), recent strategic moves and client-facing capabilities such as installation and aftercare. The full report provides a comparative matrix and supplier-fit map that helps buyers align supplier strengths to project archetypes.

We track several developments with immediate buyer/supplier implications:

Trade-show and technology showcases continue to be an R&D conduit. Companies using high‑visibility forums to highlight absorber innovations are accelerating partner engagement and specification cycles.

New material introductions — for example, polypropylene-based RF absorbers entering the market — illustrate how material substitution can be used to manage raw-material exposure or to meet specific fire or environmental profiles.

Fire-safety certifications and lab-tested classifications are becoming procurement thresholds rather than optional endorsements. Where suppliers can demonstrate harmonized performance across ASTM/EN/RoHS, they shorten customer validation timelines.

Demand-side capacity expansions by major OEMs and defense primes (new radar production lines and test facilities) directly drive absorber demand in the near term and should be tracked as procurement cycle signals.

For executives preparing budgets and sourcing strategies in 2026, we present three concise scenarios — each translated into actionable recommendations:

Base case (aligned with our market CAGR): expect steady ordering patterns for absorbers and predictable refurbishment cycles. Actions: prioritize multi-year supply agreements with performance SLAs; invest in in-house testing capacity for rapid acceptance; reserve capital for modular expansions rather than large bespoke builds.

Upside (accelerated telecom deployments or defense procurements): secure capacity by qualifying second-source suppliers, prepaying critical volumes where contractually prudent, and accelerating installation scheduling to capture earlier market windows.

Downside (raw-material disruption or regulatory tightening): enact rapid substitution playbooks that include prequalified PP or alternative foam chemistries, accelerate ferrite tile qualification where appropriate, and adopt procurement clauses that allocate price and lead-time risk.

Cross-cutting recommendations for 2026:

Implement a material dual-sourcing strategy targeted at reducing dependency on single-feedstock polyurethane formulations; pursue technical partnerships that accelerate alternate-material validation.

Elevate certification acquisition as a competitive moat—prioritize ASTM E84 Class A and harmonized REACH/RoHS documentation for absorbers intended for multi-jurisdictional installations.

Factor in service-led revenue models (refurbishment, absorber recycling/reconditioning) as a way to spread capital intensity and create recurring relationships with testing facilities and OEMs.

Use the report’s supplier-fit matrix to pinpoint M&A or JV prospects: look for niche absorber innovators with IP in foam formulations or ferrite composites that complement existing systems-integration strengths.

This press brief is a strategic trailer. The complete market study provides the granular inputs that procurement, engineering and corporate development teams need to act decisively in 2026, including:

A full quantitative forecast model across 2020–2032, with scenario toggles and sensitivity analysis for raw-material and regulatory shocks.

Detailed supplier profiles and a competitive-comparison matrix with capability scoring.

Buyer-targeted tools: RFQ templates, acceptance-test protocols, and a retrofit vs. replacement calculator calibrated to chamber types and testing regimes.

Regulatory and standards appendix showing test methods, certification pathways and recommended timelines for labs and OEMs pursuing international compliance.

As the anechoic chamber materials market matures, leadership will be defined less by singular product advantage and more by integrated value chains that combine materials science, consistent certification, agile sourcing and service continuity. For 2026 planning cycles, organizations that align procurement, engineering and compliance strategies around the dynamics highlighted here will materially reduce programme risk and accelerate time-to-test for new products.

PW Consulting invites procurement leaders, test-lab operators and systems integrators to consult the full report for the proprietary segmentation data, supplier scorecards and the forecast model that underpin these strategic recommendations. The full analysis is the working toolkit your team needs to convert market visibility into executable 2026 strategies.

For detailed analysis of this topic, please visit the official page:Anechoic Chamber Material Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com