Cerium Oxide Market — Strategic Outlook for 2026 Decision-Makers

Executive trailer

PW Consulting’s new Cerium Oxide Market report is designed as the strategic playbook for organizations making decisive investments in 2026. Building on an evidence base that traces market value from 2020 through a 2025 base year and projects forward to 2032, the study frames the commercial choices facing producers, buyers and investors against a 6.2% compound annual growth rate. The global market, which surpassed the billion‑dollar threshold in 2025, is projected to continue expanding through the 2026–2032 forecast window. This release highlights the forces that will shape supplier power, pricing cycles and product mix optimisation — while holding back detailed sub‑segment datapoints to compel decision-makers to access the full intelligence package.

Ceriumiv Oxide Market

Why this report matters for 2026

- Timing: 2026 will be the inflection year for many capacity and sourcing decisions initiated in 2023–2025; our report translates near‑term signals into executable strategies.

- Risk management: We map how geopolitical controls, quotas and trade measures alter the effective supply curve and where single‑point failures are most acute.

- Investment prioritisation: We model capex payback under realistic demand trajectories and regulatory scenarios to help boards allocate capital to purity upgrades, downstream integration or geographic diversification.

- Commercial operations: The report includes operational playbooks (contract clauses, inventory rules, and tolling vs. captive manufacturing decision trees) that procurement and operations teams can implement immediately.

Market trajectory at a glance (selected macro datapoints)

Between 2020 and 2025 the market expanded from under USD 800 million to just over USD 1 billion, reflecting sustained demand across polishing, catalytic and specialty industrial uses. Our baseline projection shows the market continuing its upward path in 2026 and beyond, reaching a materially larger scale by the end of the 2032 forecast period. The 6.2% CAGR baked into our scenarios assumes continued adoption in electronics, incremental demand from emission control technologies, and periodic inventory restocking tied to policy shocks and raw‑material availability.

Ceriumiv Oxide Market

Key demand drivers and structural dynamics

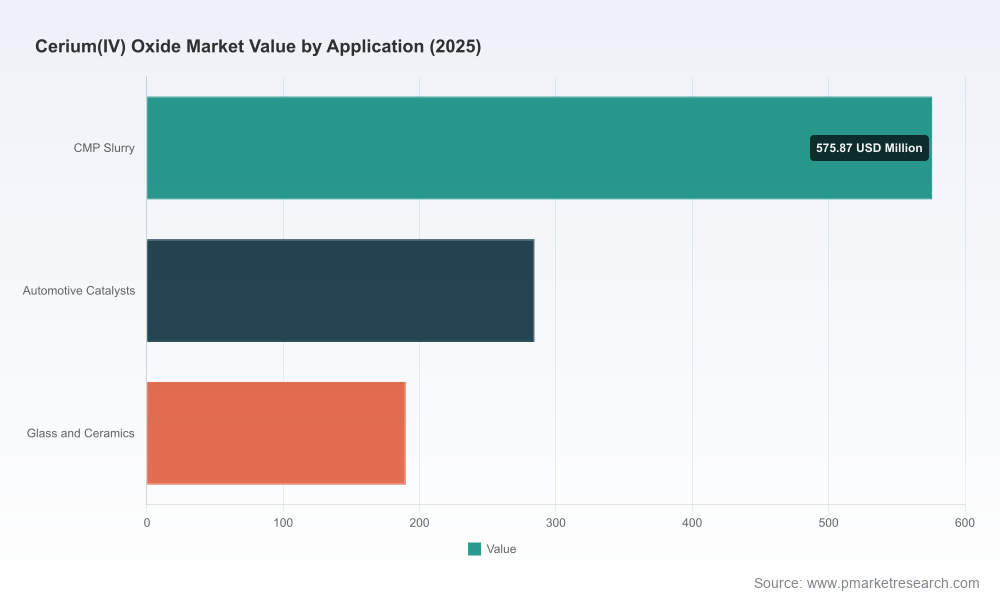

- Technology migration in semiconductors and optics. High‑precision CMP slurries and optical polishing remain primary technical applications; shifts in wafer diameters and polishing specifications materially affect high‑purity demand.

- Automotive and emissions control. Scrutineering of internal combustion engine emissions and the parallel growth of hybrid powertrains sustain a structural market for ceria‑based catalysts and washcoats.

- Industrial and glass sectors. Glass, ceramics and specialty coatings provide a resilient base demand; cyclical swings in construction and automotive glass markets introduce episodic variability.

- Product technology spectrum. The market divides between industrial‑grade powders (volume, cost‑sensitive) and high‑purity electronic/nano grades (margin‑sensitive). Our modelling isolates the impact of moving capacity along that spectrum without disclosing proprietary split values here.

Supply-side stresses, geopolitics and their commercial implications

The cerium oxide value chain is unusually sensitive to raw‑material policy and processing capability. Recent policy moves and supply events create clear tactical imperatives for 2026:

Ceriumiv Oxide Market

- Export control and quota risk: Controls on separation and purification technologies enacted by major producing states, together with production quotas, compress the available pool of processed material for export markets. These constraints propagate through to lead times and bargaining leverage with suppliers.

- Tariffs and trade policy: Existing additional duties on certain imports into the U.S. and tightening controls on transfer of refining technologies impose effective cost floors and create incentives for near‑shoring or tariff mitigation strategies (e.g., in‑region tolling or processing partnerships).

- Raw feed availability: Suspension of mining or processing operations in supplier countries introduces episodic shortages of bastnäsite‑derived feedstock that disproportionately affects lower‑cost industrial volumes and forces substitution or inventory draws.

- New capacity: Private investments and commissioned facilities in light‑rare‑earth processing are beginning to alter medium‑term availability. These projects reduce systemic tail risk but introduce transitional price and utilisation volatility as new flows compete with established trade routes.

Competitive landscape — concentrated yet contestable

The cerium oxide market exhibits moderate concentration: the top three and top five producers account for meaningful portions of global supply, creating oligopolistic tendencies in specific purity tiers and product forms. That concentration is not uniform across grades or applications, which creates opportunity for nimble specialists and regional suppliers to defend or expand niches.

Notable industry players include long‑standing European and Japanese specialty producers, diversified chemical groups active in catalyst and electronic materials, US‑based nanomaterials suppliers, and vertically integrated rare‑earth processors in the Asia Pacific region. Examples include established specialist powder producers and international suppliers known for high‑purity electronic grades and catalyst feedstocks. Some firms emphasise nanopowders and sputtering targets for advanced applications; others focus on industrial volumes for glass and ceramic markets. Recent corporate moves — expansion of rare‑earth processing capacity and national export controls — are already reshaping supplier strategies.

Recent developments shaping 2026 decisions

- Capacity additions in light‑rare‑earth processing: New commissioned facilities increase processing throughput for light rare‑earth separation, widening options for downstream cerium oxide producers — but the benefit to markets is phased as assets ramp and product qualification completes.

- Regulatory and export controls: Government actions restricting purification technologies and exportable processing know‑how heighten the value of localized processing and technology partnerships. Buyers should treat access to advanced purification capability as a strategic procurement criterion.

- Raw material pricing baseline: Market benchmarks show modest unit‑price levels for standard grades in recent history, but the pass‑through to finished product prices depends on grade mix and transport/ tariff overlays.

Price, margins and what to expect in 2026

Our scenario analysis finds that margins in the industry are driven primarily by (a) grade mix (high‑purity vs industrial), (b) feedstock sourcing costs and (c) utilisation rates in finishing plants. Near‑term price sensitivity is elevated by policy shocks and inventory positioning: procurement teams should model multi‑month delivery lag, tiered pricing for purity upgrades and the cost implications of alternative logistics routes that mitigate tariff exposure.

What’s inside the PW Consulting report — practical tools (high level)

- Dynamic demand model: month‑by‑month and quarterly scenarios for 2026–2032 with switchable assumptions for technology adoption and regional policy overlays.

- Supply continuity playbook: supplier scorecards, dual‑sourcing decision trees, tolling vs captive manufacturing ROI calculators, and suggested clause language for long‑term purchase agreements.

- Valuation and M&A toolkit: a bespoke valuation module for producers and processors, and an acquisition playbook covering integration priorities (purity control, downstream channel, and intellectual property).

- Regulatory risk heatmap: mapped to plant locations, trade corridors and technology dependencies — actionable for compliance and scenario planning.

- Commercial negotiations kit: price‑index structures, escalation clauses and inventory financing models tailored to ceria’s cost drivers.

Recommended actions for 2026 (prioritised)

- Immediate: Conduct a short‑list review of alternate supply partners and secure staggered contracts with price‑adjustment mechanisms tied to transparent indices.

- Near term (6–18 months): Lock in capacity or tolling agreements for high‑purity grades if your product roadmap requires them — achieving qualification lead times is critical for semiconductor and optics suppliers.

- Strategic (18–36 months): Evaluate vertical integration or strategic stakes in upstream separation assets to insulate against technology export restrictions and quota risk.

- Operational: Institute an inventory policy that blends safety stocks with just‑in‑time replenishment for critical purity tiers and enables rapid substitution between grades where feasible.

- Finance & M&A: Use scenario stress tests from our model when valuing target assets; pay attention to technology IP that enables higher yields in purification and lower lifecycle emissions — such capabilities command premium multiples.

Who should read the report

Procurement leads, plant operations teams, corporate strategists, private equity and venture investors active in speciality chemicals, and policy advisors in trade and industrial strategy will find the report directly operational. It provides both executive briefings for boardrooms and tactical checklists for sourcing and production teams.

How to access the full intelligence

This article is a strategic preview: it demonstrates the depth of our analysis while deliberately withholding granular segment and region split values that are included in the full Cerium Oxide Market report. To unlock the complete dataset, validated models, supplier scorecards and negotiation templates, please visit PW Consulting’s report page or contact our industry practice directly. The comprehensive package contains the precise sub‑segment forecasts, regional flows and pricing matrices necessary to execute 2026 strategies with confidence.

Conclusion

Ceria markets are entering a phase where policy, technology and capacity interact to create both risk and opportunity. For organisations that move deliberately in 2026 — prioritising supply diversification, purity capability and strategic partnerships — there is a clear path to durable competitive advantage. PW Consulting’s Cerium Oxide Market report transforms market signals into executable choices and the operational tools needed to deliver them.

For detailed analysis of this topic, please visit the official page:Ceriumiv Oxide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com