Regional Insights into the Global Consumer Packaged Goods Market

Other |

2026-03-10 10:09:38

PW Consulting’s latest market intelligence brief on Pulmonary Embolism (PE) Therapeutics synthesizes clinical, commercial, regulatory, and reimbursement dynamics into a single, actionable roadmap for executives, investors, and policy-makers preparing for 2026 and beyond. Built on a proprietary financial model with base year 2025 and a forecast horizon of 2026–2032, the analysis quantifies market momentum and translates it into practical choices you can act on. The market is expanding at a compound annual growth rate (CAGR) of 8.15%, growing from an estimated USD 2,185.4 Million in 2025 to approximately USD 3,781.9 Million by 2032 — a trajectory that demands timely strategic responses across pharma, device, and services players.

Pulmonary Embolism Therapeutics Market

Transition windows are opening. Several high-impact patent expiries and regulatory milestones converge on the 2026 timeframe, creating narrow but decisive windows for launch sequencing, lifecycle management, and competitive defense.

Pulmonary Embolism Therapeutics Market

Clinical evidence is shifting the standard of care. Recent device trial outcomes and evolving thrombolysis data are reshaping clinical pathways for intermediate and high-risk PE patients — altering hospital adoption curves and payer reimbursement judgments.

Pulmonary Embolism Therapeutics Market

Unit economics are in flux. Reimbursement updates and supply-side shocks are changing margin assumptions for both drug and device manufacturers, necessitating rapid revision of pricing, contracting, and tender strategies.

Robust market-sizing model (USD, Million): A bottom-up model calibrated to 2020–2025 historicals and stress-tested across multiple 2026–2032 scenarios. Core outputs include base-case, optimistic, and downside trajectories tied to specific regulatory and reimbursement events.

Scenario playbooks for 2026 decision points: Actionable “if/then” plans for product owners facing patent cliffs, for device OEMs evaluating market entry or scale-up, and for investors sizing opportunities in early-stage thrombectomy technologies.

Commercial launch and lifecycle roadmaps: Market-access templates, payer engagement scripts, and HTA evidence packages bespoke to PE interventions that accelerate formulary placement and hospital adoption.

Competitive heatmaps and M&A thesis builder: An agnostic assessment of incumbent strengths, disruptive entrants, partnership fit, and inorganic playbooks aimed at materially improving deal outcomes.

Operational toolkits: Excel-ready pricing/reimbursement sensitivity models, KPIs for managed care negotiations, and physician-adoption cadence matrices designed for operational teams to implement immediately.

Primary research supplements: Select KOL interviews, hospital procurement survey data, and payer decision-framework exemplars that validate model assumptions and provide qualitative context.

Patent and generic waves: Key oral anticoagulant patent expirations are scheduled around the 2026 window. These events will accelerate generic entry, compress pricing differentials, and force originators to choose between aggressive lifecycle investments (new formulations, pediatric indications, line extensions) or margin defense via contracting and value-based arrangements.

Device adoption accelerated by evidence: The latest randomized data demonstrating superiority of certain mechanical thrombectomy approaches in selected patient cohorts, together with device-specific FDA clearances, are prompting hospitals to reassess capital allocation toward PE interventional suites. For device OEMs, timing investments in training, registries, and bundle-of-care relationships with health systems is now a determinative factor for market share capture.

Reimbursement and procedure economics: Recent reimbursement policy updates have established a meaningful payment pathway for mechanical thrombectomy procedures. Those payment levels materially affect hospital willingness to deploy capital and offer new therapies — a positive signal for device utilization but one that introduces negotiation dynamics with payers over indications and coding.

Supply-chain and input-cost volatility: API supply constraints in anticoagulant manufacturing and intermittent shortages in heparin sources have increased raw material costs in recent years. These pressures are likely to persist in the short term and should be incorporated into margin and pricing models for 2026 budget cycles.

Pharmaceutical incumbents with leading oral anticoagulants retain strong clinical franchises today, but intellectual property timelines and increasing generic pressure will require differentiated strategies — from real-world evidence generation to indication expansion and bespoke patient support services.

New and established device players are moving beyond product sales to offering systems of care: From aspiration and ultrasound-facilitated systems to mechanical thrombectomy platforms, the competitive difference will increasingly be decided by clinical data, intra-procedural workflow, and post-market registries rather than basic device specs.

Market concentration is notable: the three-largest participants control a meaningful majority of today’s revenues, with the top five capturing an even larger share. This concentration underscores both barriers to entry and the potential value of targeted M&A for accelerating scale and market access.

Recent company-level developments underscore these shifts: randomized trial data supporting device superiority in defined subpopulations, new clearances aimed at procedural safety, and iterative device launches that improve operating efficiency. Each event materially alters adoption curves and payer expectations; our financial model reflects those inflection points.

Pharma (originators): Prioritize value demonstration in head-to-head and real-world settings; accelerate life-cycle innovation where feasible; pre-plan contracting strategies anticipating generic erosion.

Device OEMs: Invest in KOL partnerships and hospital implementation services; align product launches with reimbursement windows and trial readouts; use outcome-based pilots to unlock broader commercial reimbursement.

Health systems and payers: Reassess care pathways where procedural reimbursement makes thrombectomy economically viable; negotiate bundled payments and outcomes guarantees to contain downstream costs.

Investors and M&A teams: Look for platform plays that combine clinical differentiation, regulatory clarity, and commercial pathway de-risking. Targeted tuck-ins that fill distribution or clinical-evidence gaps will deliver asymmetric value.

Regulatory unpredictability: Accelerated approvals and label changes can reconfigure market access; our report highlights contingency scenarios and regulatory milestones to monitor closely through 2026.

Reimbursement reversals: CMS and private payer decisions on coding and payment levels can change procedure economics; scenarios include both more-restrictive and more-favorable outcomes and their effects on utilization.

Supply disruptions: Raw material scarcity can constrict supply and spike costs — diversify suppliers, secure long-term contracts, and quantify margin sensitivity in planning cycles.

Clinical adoption lag: Even with positive trial data, real-world uptake is conditioned on training, guideline revisions, and local practice inertia — our adoption model integrates these frictions into revenue timelines.

Lock in 2026 playbooks: Treat the mid-decade patent and regulatory calendar as a gating item for commercial and R&D resource allocation. Define contingency budgets for accelerated evidence generation if required.

Accelerate payer engagement: Develop outcome-based contracting pilots and hospital value dossiers now — payers are receptive to evidence tied to procedure economics and readmission reduction.

Design launch sequencing around clinical pivots: For device companies, align market rollout with center-of-excellence programs and registries to shorten the commercialization curve.

Consider strategic portfolio moves: For incumbents facing imminent generic pressures, explore acquisitions or alliances in complementary device or diagnostics assets that can offset margin erosion.

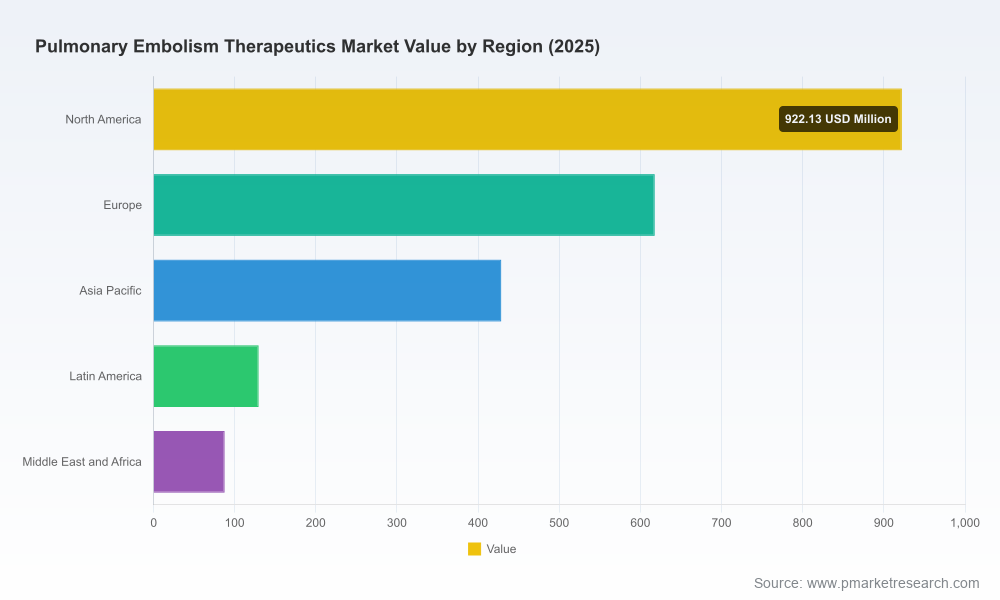

PW Consulting’s report is underpinned by an exhaustive quantitative model and primary research that map to the market’s 2020–2025 historicals and project into 2032. The report explicitly models base year 2025 and the forecast period 2026–2032 (CAGR 8.15%), with detailed revenue trajectories and sensitivity analyses. To preserve the report’s commercial value — and to respect the “trailer” principle of this release — we intentionally omit granular public disclosure of core segmentation tables and regional/application splits in this summary. Those detailed segment-level datasets, scenario-specific assumptions, and the interactive model are available exclusively in the full report package and via the PW Consulting client portal.

For teams preparing 2026 budgets, M&A pipelines, or product launch plans, access to the full PW Consulting Pulmonary Embolism Therapeutics Market report will materially shorten decision cycles and reduce execution risk. The full deliverable contains the complete modeling workbook, competitor dossiers, payer matrices, and tactical playbooks referenced here. Contact PW Consulting to request a briefing, receive a sample dashboard, or arrange a tailored workshop that maps our insights to your organization’s 2026 strategic priorities.

PW Consulting stands ready to help you translate this market momentum into defensible, value-creating actions for 2026. Visit our report page to unlock the full dataset and begin scenario planning with your executive team.

For detailed analysis of this topic, please visit the official page:Pulmonary Embolism Therapeutics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com