Mesalamine Market Insights, Growth Drivers, and 4% CAGR Forecast to 2031

Other |

2026-02-19 10:15:38

PW Consulting’s latest industry study on the Hospital-Acquired Infection (HAI) Control Market delivers a practical, forward-looking playbook for executives planning 2026 actions. Against a backdrop of accelerating regulatory scrutiny, payer pressure, and rapid technology maturation, the global market — which expanded from roughly USD 22.8 billion in 2020 to about USD 31.2 billion in 2025 — is set to continue growing. PW projects the market to reach roughly USD 33.1 billion in 2026 and to approach the mid-40s (USD) by the early 2030s under a forecast compound annual growth rate of 6.45% for the 2026–2032 period. These headline dynamics frame a set of near-term strategic choices for hospital systems, device and consumable manufacturers, and investors. This release summarizes the report’s strategic value while reserving detailed subsegment and regional breakout data for the full report.

Hospital Acquired Infection Control Market

Actionable scenario planning: Our analysis translates macro growth into three operational scenarios (Conservative, Baseline, Accelerated Adoption) tied to regulatory milestones and buyer financing models, enabling CFOs and strategy teams to stress-test capital and procurement plans for the coming 12–18 months.

Hospital Acquired Infection Control Market

Regulatory and reimbursement mapping: We map how evolving FDA guidance, EU MDR post-market surveillance expectations, and persistent CMS financial penalties for elevated HAI rates jointly shape procurement priorities and adoption timetables for new technologies.

Hospital Acquired Infection Control Market

Competitive positioning intelligence: The report synthesizes product, channel and service strengths of incumbent suppliers and emerging niche players, identifying whitespace where innovators can capture share without directly confronting entrenched incumbents.

Deal and portfolio playbook: For corporates and PE sponsors, the report provides M&A and partnership playbooks that align with regulatory risk, time-to-revenue, and the fragmented nature of supply chains in sterilization, disinfectants and software-enabled monitoring.

Three structural forces are converging to accelerate spending in HAI control. First, regulatory catalysts — including recent advisory discussions at the FDA concerning germicidal UV devices and tightened EU MDR requirements — are raising the bar for clinical validation and post-market evidence. Second, payer and provider economics: persistent CMS penalties and value-based purchasing models continue to make HAI reduction a financially material item on hospital balance sheets. Third, technology convergence: advances in UV-C robotics, low-temperature sterilization, single-use consumables with antimicrobial features, and software-driven infection surveillance are shifting vendor value propositions from one-off products to outcomes-linked service models.

These pressures are not uniform across the market; they affect product categories differently. Capital-intensive devices face longer approval and procurement cycles but offer higher per-unit value and service revenue potential. Consumables and PPE drive recurring revenue and faster adoption but are sensitive to price competition and supply-chain volatility. Software and monitoring services present attractive margin and annuity models but require robust integration with hospital IT and demonstrable ROI on HAI metrics.

The HAI control market exhibits a moderate level of concentration with the top three players accounting for a meaningful but not dominant share and the top five holding a larger portion of the market. This structure supports both scale plays by large diversified firms and targeted disruption by specialized technology vendors.

3M Company — With a broad infection prevention portfolio spanning sterilization monitoring, surgical drapes, disinfectants and skin antiseptics, 3M competes on integrated product suites and deep clinical relationships. Its playbook emphasizes bundling consumables and monitoring solutions to lock-in hospital workflows.

STERIS plc — STERIS’s strength is in comprehensive sterile-processing systems, including sterilizers and washer-disinfectors, paired with services. The company benefits from long-term contracts with sterile processing departments and opportunities to upsell service and validation packages as regulatory demands rise.

Getinge AB — Focused on sterilization and washer-disinfectors, Getinge has augmented its addressable market through targeted acquisitions to strengthen consumables and distribution in the U.S. market. Its strategy demonstrates the value of combining capital equipment leadership with consumable synergies.

Ecolab Inc. — Ecolab competes on comprehensive hygiene programs and managed services for healthcare facilities. The company’s advantage lies in facility-level contracting and the ability to link cleaning chemistries to operational KPIs.

Becton, Dickinson and Company (BD) — BD’s infection-prevention differentiation stems from device-level innovations (e.g., antimicrobial catheters, preps) that mitigate infection vectors. Device-level gains translate into clinical adoption when supported by strong evidence and clinician advocacy.

Xenex Disinfection Services Inc. — As a specialist in pulsed xenon UV-C robotic systems, Xenex exemplifies the high-innovation niche: relatively capital-intensive technology with a strong infection-reduction narrative that must clear regulatory and reimbursement hurdles to scale.

Advanced Sterilization Products (ASP, Fortive) — ASP’s low-temperature sterilization systems and high-level disinfectants target heat-sensitive device sterilization use cases and remain sticky in sterile processing workflows.

Belimed AG and Sotera Health — These players emphasize sterile processing equipment and contract sterilization services, respectively, offering route-to-market advantages via outsourced sterilization and validation services.

Strategically, large diversified firms leverage bundled offerings and scale in distribution; specialists compete on clinical differentiation, rapid evidence generation, and service-led contracts. For 2026, successful vendors will align product roadmaps with emerging regulatory evidence standards and embed services that reduce buyers’ total cost of ownership.

Regulatory clarifications in 2025 established precedent for how germicidal UV devices will be evaluated; several whole-room UV platforms received FDA clearances or De Novo authorizations in 2025, creating a regulatory pathway for similar technologies.

M&A activity—such as strategic acquisitions to broaden consumables portfolios and U.S. distribution—highlights consolidation opportunities where scale and channel breadth accelerate adoption.

New device-level approvals for novel applications (for example, a De Novo authorization for a UV device targeting connectors) indicate that incremental innovations with clear contamination-reduction claims can achieve regulatory traction if backed by rigorous clinical data.

Hospital systems: Prioritize investments that deliver measurable HAI reductions tied to reimbursement risk. Favor solutions that combine robust clinical evidence, integration with electronic health records, and service guarantees that reduce operational burden.

Manufacturers: Accelerate clinical validation programs to satisfy evolving regulatory expectations. Consider hybrid commercial models that pair capital sales with recurring service and consumable revenue to stabilize top-line growth.

Investors and M&A teams: Target companies that offer either clear clinical differentiation or pathway-to-scale via distribution partnerships. Due diligence should stress regulatory defenseability and the cost-to-prove-efficacy for HAI outcomes.

Policy-makers and procurement bodies: Design procurement frameworks that reward verifiable outcomes and lifecycle cost efficiencies rather than lowest upfront price, which will incentivize investments in higher-efficacy technologies.

Five-year scenario financial models (conservative/baseline/accelerated) that convert market-level CAGR into P&L and balance-sheet impacts for suppliers and providers.

Go-to-market playbooks and channel-mix strategies tailored to product archetypes (capital equipment, consumables, software/services), including recommended pricing and contracting approaches.

Regulatory and clinical evidence checklist for each technology class, with recommended study designs and endpoints aligned to recent FDA guidance and EU MDR expectations.

Deal-screening scorecards and integration templates for M&A activity, preserving focus on time-to-revenue, evidence generation cost, and distribution synergies.

An interactive competitive matrix profiling incumbent advantage vectors and white-space opportunities where innovators can pursue clinical and commercial differentiation.

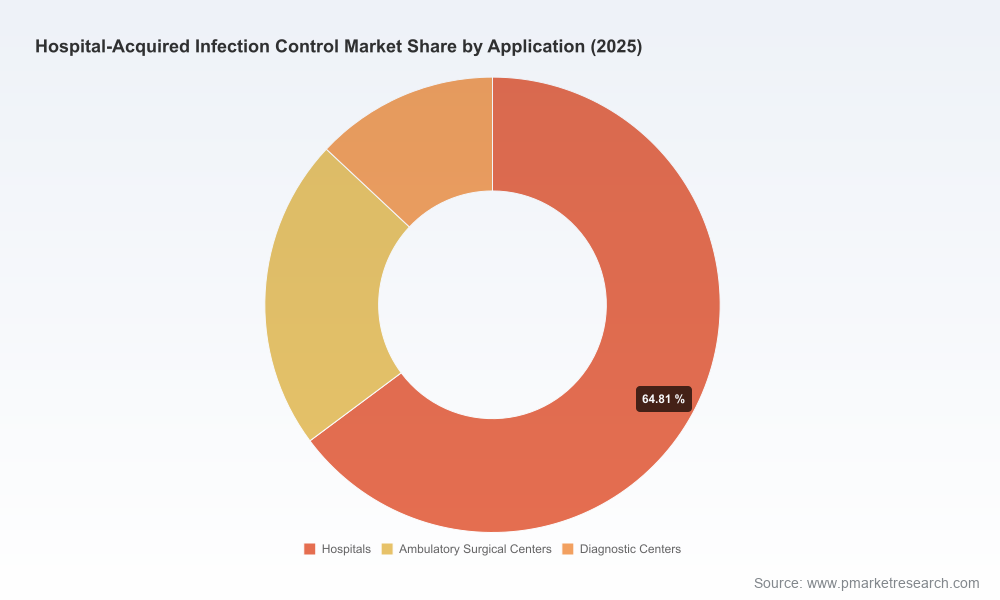

Note: To preserve the “trailer” nature of this communication and to direct stakeholders to the full intelligence set, we have omitted detailed regional, application and product-segment numeric breakouts from this summary. The complete report contains granular revenue split tables, region- and application-level forecasts, and vendor share estimates necessary for execution-level planning.

As the HAI control market progresses through 2026, executives face a classic strategic inflection: choose rapid deployment of proven, integrated solutions that deliver measurable reductions in infection metrics, or risk downstream financial exposure from payers and regulatory scrutiny. PW Consulting’s report translates headline growth — from roughly USD 22.8 billion in 2020 to USD 31.2 billion in 2025 and onward under a 6.45% CAGR through 2032 — into executable moves across procurement, product development, and M&A. For leaders who need to convert market momentum into defensible, near-term wins, the full PW Consulting HAI Control Market report provides the necessary playbook, models, and evidence roadmaps.

Access the full report and the complete dataset, including detailed subsegment and regional forecasts, evidence checklists, and executable templates, via the PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Hospital Acquired Infection Control Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com