Hochwertige Komponenten für jede Photovoltaikanlage verfügbar

Home |

2026-06-08 14:45:07

PW Consulting’s latest industry briefing on the Anti‑Fungal and Anti‑Bacterial Paints Market synthesizes market-scale analytics, competitive mapping and regulatory foresight into a decision-grade toolkit specifically tailored for executives planning 2026 resource allocation. Built on a base year of 2025 with historical coverage from 2020–2025 and a detailed forecast through 2032, our model shows a resilient compound annual growth rate of 7.45% across the forecast window — a trajectory that translates into meaningful expansion opportunities and distinct strategic trade‑offs for manufacturers, additives suppliers, and downstream specifiers.

Anti Fungal And Anti Bacterial Paints Market

Measured growth and scale: The market has expanded steadily over the past half‑decade, reflecting enduring demand for hygiene‑focused coatings across healthcare, food processing, residential and institutional spaces. Our topline modelling — updated to 2025 as the report’s base year — projects continued momentum through 2032 under our base case assumptions.

Anti Fungal And Anti Bacterial Paints Market

Demand pull from hygienic environments: Structural secular drivers remain robust — rising healthcare infrastructure investments in emerging and developed markets, stricter hygiene requirements in food & beverage production, and heightened consumer preference for low‑maintenance, mould‑resistant interiors are key demand levers.

Anti Fungal And Anti Bacterial Paints Market

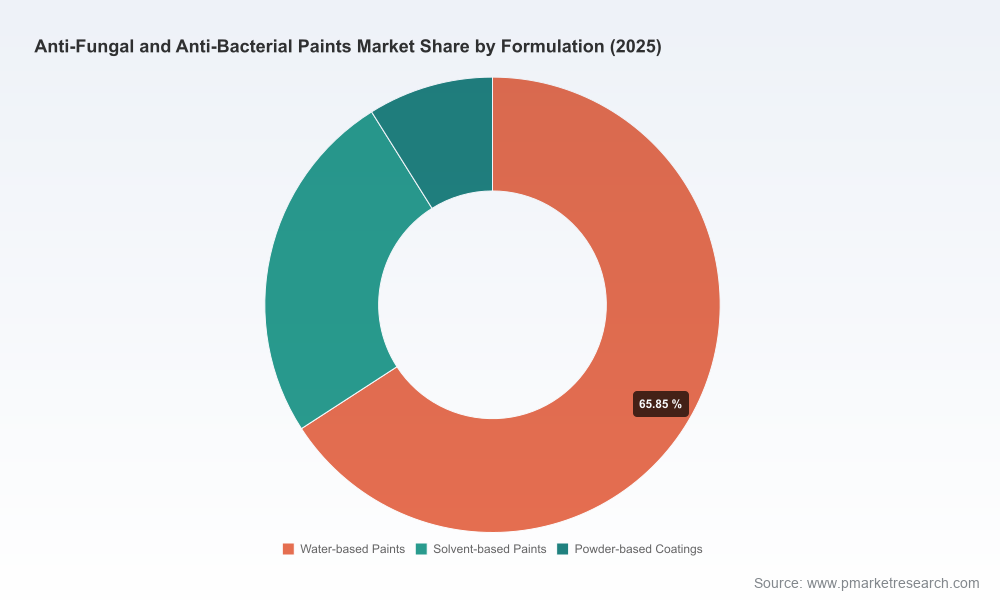

Technology and formulation shifts: Water‑based, low‑VOC formulations and hybrid additive packages are increasingly preferred by specifiers seeking compliance with environmental and health standards while maintaining antimicrobial performance.

Input and regulatory headwinds: Volatility in specialty additive pricing (notably silver‑ and copper‑based chemistries), ongoing biocide reviews, and higher bar for claims substantiation are constraining margin expansion for some players but creating an opening for differentiated, validated solutions.

Robust market sizing and scenario forecasts: Proprietary models that translate macro drivers into top‑line revenue projections under multiple demand, price and cost scenarios. (This press release highlights the overall scaling logic and headline CAGR; fine‑grained segment tables and numerical splits are reserved for the full report.)

Go‑to‑market playbooks: Product positioning matrices, channel and distributor optimization, and an MQL‑to‑PO conversion framework for hygiene‑focused coatings tailored to healthcare and food industry procurement cycles.

Regulatory risk matrix and remediation roadmap: A step‑by‑step compliance framework aligned to recent regulatory moves (EU and US) that prioritizes testing, labeling and regional registration sequencing to avoid costly market access delays.

Cost and margin stress tests: Sensitivity analyses that quantify impacts of specialty additive price shocks, formulation shifts, and carbon/packaging levies on EBITDA under alternative pricing strategies.

Technology and validation protocols: Benchmarked lab screening methodologies and third‑party verification pathways that reduce time‑to‑claim and protect against post‑launch remediation costs.

Market concentration is moderate: the top three and top five firms together capture meaningful but not dominant shares of the market, indicating both the presence of scale advantages and room for niche specialists. For strategic planners, that implies dual pressures: scale economies matter for national and global contracts, while differentiated technical capability or local service can win specialized and higher‑margin business.

Integrated global coatings leaders: Firms with broad decorative and performance coatings portfolios are leveraging scale, distribution and brand trust to push antimicrobial offerings into mainstream specifiers. They benefit from cross‑sell opportunities across architectural and industrial channels and are well‑placed to absorb incremental compliance and testing costs.

Specialist formulators and additive suppliers: Technology‑focused players — including those supplying silver, plant‑based or proprietary biocidal additives — remain essential partners in product differentiation. Their ability to advance durable, validated antimicrobial performance is a key determinant of downstream claims and price premiums.

Emerging consolidation dynamics: Recent announced combinations among major players are poised to reconfigure competitive positioning, creating both integration opportunities and short‑term uncertainty. Executives must evaluate how scale‑seeking M&A will affect pricing, R&D prioritization and product rationalisation in 2026 and beyond.

Representative company profiles we review in the full analysis include leading global coatings multinationals and high‑specialty firms, capturing the spectrum from large integrated manufacturers to focused antimicrobial technology providers. Each profile assesses product portfolios, R&D pipelines, go‑to‑market footprints and regulatory readiness — and highlights where partnerships, licensing or bolt‑on acquisitions could be accretive.

Regulatory tightening and harmonization: Recent policy updates in major jurisdictions have raised the bar for data protection, labeling and active‑substance review timelines. These changes increase the importance of a proactive regulatory strategy that sequences registrations, secures data rights and plans for compliance costs.

Biocide review cycles: Continued routine reviews by major regulators (including multi‑year reassessments of widely used preservatives) create potential for reformulation cycles and staggered market access — a timing risk that can affect product roadmaps and inventory management.

Specialty additive volatility: Price swings in silver and other metal‑based additives materially affect COGS for premium antimicrobial systems. Hedging strategies, supplier diversification and investment in alternative chemistries are practical mitigation levers we quantify in the report.

Prioritize validated claims: Invest in third‑party testing and durable performance data to pre‑empt regulatory pushback and defend premium pricing. Rapid, reproducible lab screening can reduce time‑to‑market and litigation risk.

Diversify additive sourcing and consider hybrid chemistries: Maintain negotiating leverage and reduce supply shock exposure by qualifying multiple additive suppliers and exploring lower‑cost, performance‑equivalent alternatives.

Adopt flexible pricing and contracting models: Build clauses to account for input cost pass‑throughs, and structure long‑term supply agreements for large institutional customers to protect margins.

Pursue targeted M&A and alliances: Look for bolt‑on acquisitions that add validated antimicrobial technologies, certified testing capability, or regional manufacturing and distribution to accelerate market coverage without protracted organic R&D timelines.

Scenario planning and stress testing: Use scenario models built around the 7.45% CAGR baseline and alternative stress cases (regulatory tightening, additive price shock, slower construction activity) to prioritize capital allocation and inventory strategy.

Differentiate with sustainability and stewardship narratives: Certifications, low‑VOC claims and transparent stewardship of biocidal chemistries can close sales in sensitive end markets while precluding reputational risk.

Executives who must reconcile growth ambitions with regulatory complexity and input volatility need actionable analytics — not just descriptive charts. PW Consulting’s Anti‑Fungal and Anti‑Bacterial Paints Market report combines a firm‑level competitive scorecard, regulator‑by‑regulator compliance timelines, scenario‑driven financial models and a playbook for commercialization that together create a single source of truth for 2026 planning. Our deliverables include customisable spreadsheets, a prioritized list of tactical initiatives for commercial teams, and a short‑list of strategic acquisition targets based on capability and cultural fit.

Consistent with the “trailer” principle of this release, we have purposefully limited the public disclosure of granular segment splits and specific regional/application dollar breakdowns: these detailed matrices and tables are embedded in the full report to ensure an integrated strategic view and protect commercially sensitive modelling assumptions. For procurement teams, R&D leaders and corporate strategists ready to convert insight into action, the full report provides the detailed numerical maps, supplier scorecards and regulatory checklists necessary to implement a confident 2026 plan.

To access the complete analysis, proprietary datasets and the interactive scenario toolkit, please consult the full PW Consulting Anti‑Fungal and Anti‑Bacterial Paints Market report. Our team stands ready to support bespoke workshops, due diligence on potential targets, and tailored scenario modelling to operationalize these findings.

For detailed analysis of this topic, please visit the official page:Anti Fungal And Anti Bacterial Paints Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com