Combustion Control Equipment Market — Strategic Briefing for 2026 Decision‑Makers

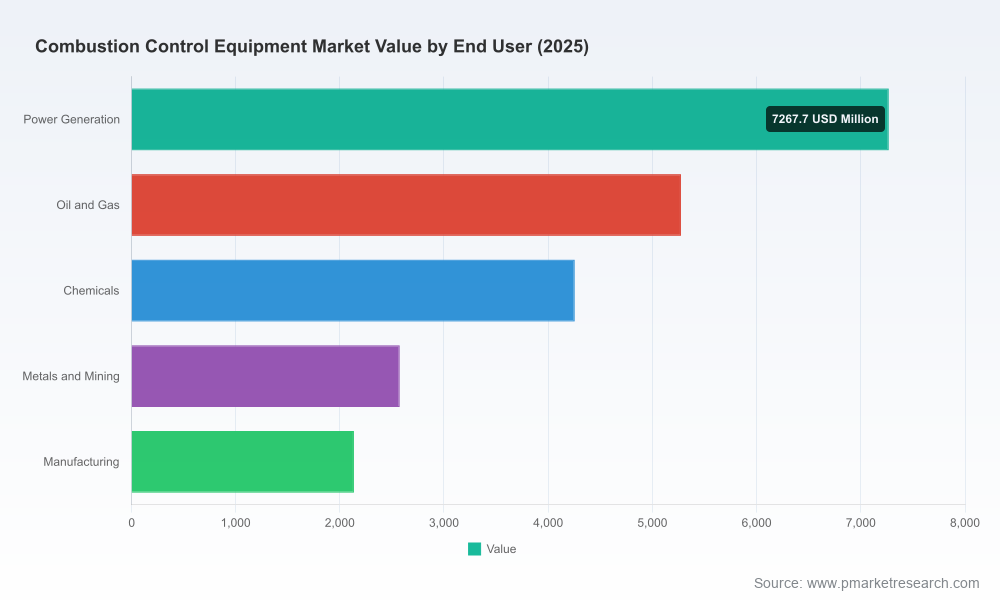

PW Consulting’s latest market research on the global Combustion Control Equipment market delivers an evidence‑based roadmap for executives planning capital allocation, product strategy, or M&A activity in 2026. Our baseline estimates place the market at approximately USD 21,505.9 Million (≈ USD 21.5 billion) in 2025, rising to an expected USD 30,260.9 Million (≈ USD 30.3 billion) by 2032 — a compound annual growth rate (CAGR) of 5.02% across the 2026–2032 forecast period. Behind these headline numbers are structural forces — regulatory tightening, energy efficiency imperatives, digitalization of assets, and supply‑chain volatility — that materially change competitive and procurement dynamics. This release summarizes the strategic implications and the specific, actionable intelligence contained in the full PW Consulting report while intentionally withholding the granular sub‑segment tables to direct readers to the source for full datasets and interactive models.

Combustion Control Equipment Market

Executive takeaways — what these macro trends mean for strategy in 2026

- Growth with selective intensity: A steady mid‑single‑digit CAGR masks pockets of accelerated demand for retrofit solutions, low‑NOx systems, and digital combustion controls; executives should prioritize high‑margin retrofit and services opportunities over undifferentiated hardware volume plays.

- Regulation and efficiency are capital allocation drivers: Meeting emissions mandates and the global efficiency targets identified by the IEA creates durable demand for control upgrades and monitoring solutions — capex planning must internalize compliance timetables.

- Supply‑chain and cost pressure require modular sourcing: Raw material inflation and higher skilled labor costs are compressing margins; procurement strategies that emphasize modularity, local service footprints, and supply diversification will outperform.

- Consolidation window for strategic buyers: Market concentration is moderate (top three and five firms account for a meaningful share), creating room for both bolt‑on acquisition and technology partnership playbooks to accelerate product roadmaps.

What the PW Consulting report delivers — practical content for immediate execution

- Proprietary market sizing and forecasting model with base year 2025 and a rigorously tested 2026–2032 scenario suite (base, accelerated adoption, and regulatory shock scenarios).

- Actionable buyer’s playbook — procurement timelines, RFP templates, supplier due‑diligence checklists, and TCO models calibrated to current material and labor cost trends.

- Vendor assessment framework — vendor positioning maps, capability heatmaps, and a repeatable vendor scorecard that helps sourcing teams short‑list partners quickly.

- Technology and product roadmaps — feature‑level demand forecasts (controls, burners, monitoring systems, boilers), retrofit vs. new‑build adoption timing, and integration considerations for DCS/PCS environments.

- Regulatory impact analysis — jurisdictional compliance timelines, retrofitting triggers, and a compliance cost estimator for CFOs and plant managers.

- M&A and partnership playbooks — valuation sensitivities, synergies model, and an prioritized list of archetypal targets by capability gap (technology, service footprint, OEM relationships).

- Field economics and service model templates — installation labor estimates, spare parts velocity models, remote monitoring go‑to‑market strategies, and margin enhancement levers.

Market dynamics to watch in 2026

- Regulatory tightening: Continued enforcement and evolution of emissions and combustion safeguards (for example, low‑NOx requirements under EU frameworks and updated NFPA standards) make phased retrofits a practical compliance necessity for large boiler operators.

- Efficiency imperatives: The International Energy Agency’s drive toward significant combustion efficiency gains through 2030 elevates efficiency upgrades from nice‑to‑have to mission‑critical investments for energy‑intensive industries.

- Input cost volatility: Stainless steel and other input price swings have lifted hardware costs (notably an ~8% YoY increase reported for stainless steel housing materials), pressuring OEM margins and accelerating the case for lighter or alternative materials and service‑based pricing.

- Labor and skills constraints: Skilled technician wages are increasing in key markets (with reported mid‑single‑digit wage rises), intensifying the need for remote diagnostics, plug‑and‑play systems, and vendor training programs to control lifecycle costs.

- Standards and safety: The active updates to combustion safeguards and oven/furnace standards require product re‑certification and design changes; firms that secure safety certifications earlier win first‑mover retrofit opportunities.

Competitive landscape — positioning and strategic moves

The competitive set is composed of global automation leaders, specialist burner and valve manufacturers, and control‑system incumbents. Each archetype offers a distinct route to capture growth: platform leadership, specialized OEM relationships, or service‑led expansion. Our report includes in‑depth profiles of the leading players, with comparative insight into their product portfolios, go‑to‑market models, and near‑term strategic initiatives.

Combustion Control Equipment Market

- Automation and systems integrators: Honeywell and Emerson lead with integrated burner management systems and distributed control platforms, respectively; Emerson’s 2025 Movimentum controller launch signals a push on boiler efficiency and retrofit simplicity.

- Industrial automation giants: ABB and Siemens combine broad automation suites with combustion safety and frequency conversion capabilities; ABB’s recent SIL 3 certification for its combustion safety modules strengthens its position in high‑integrity applications, while Siemens showcased next‑generation integration at Hannover Messe 2025.

- Engine and turbine controls: Woodward remains the reference for electronic controls and actuators in rotating equipment, anchoring competitive advantage in gas‑turbine and engine‑driven combustion management.

- Specialist burner OEMs: Firms such as Eclipse (Sterling), Fives/Maxon, Weishaupt, Oilon, and Baltur retain strong relationships with heat‑processing customers and are advancing electronic control boxes, flame detection, and dual‑fuel solutions that favor retrofit and OEM replacement cycles.

For executives, the competitive implications are clear: automation incumbents can leverage integrated software/hardware bundles to sell higher‑value service contracts; specialist OEMs can win retrofit share through installation economics and local service networks. Our report’s vendor scorecards and scenario simulations help buyers and investors quantify those tradeoffs without relying on generic headline metrics.

Combustion Control Equipment Market

Three actionable scenarios for 2026 planning

- Compliance‑Driven Retrofit: Prioritize projects for installations facing immediate emissions or safety compliance deadlines. Actions: run a compliance triage across your asset base, allocate a defined retrofit capex pool, and negotiate multi‑year service contracts with performance SLAs.

- Efficiency & Digitalization Push: Target plants with high fuel intensity for digital controls and monitoring upgrades to capture efficiency gains and remote service economies. Actions: pilot integrated controls + monitoring at two representative sites, measure fuel savings within 12 months, and scale if ROI targets are met.

- Service‑Led Consolidation Play: For OEMs and private investors, pursue bolt‑on acquisitions of regional service providers or burner specialists to expand installed‑base monetization and shorten payback timelines. Actions: use our M&A synergies model to size EBITDA uplift and define integration milestones.

How to use the full PW Consulting report

This briefing intentionally highlights strategic insights and practical next steps while withholding the underlying tabular sub‑segment data that many commercial and operational teams require for execution. The full report includes downloadable datasets, interactive dashboards, supplier scorecards, and editable financial models that allow you to:

- Run your own sensitivity tests (price shocks, policy acceleration, adoption curves).

- Populate capital‑planning templates with site‑level inputs for precise ROI and payback calculations.

- Short‑list vendors using the same scoring rubric our consulting teams use in vendor selection engagements.

Conclusion — where to focus in 2026

2026 will be a year of pragmatic investments: targeted retrofits to meet regulatory deadlines, measured digital investments to secure efficiency gains, and tactical vendor partnerships to mitigate supply and labor pressures. With the market expanding on a 5.02% CAGR through 2032 and clear regulatory and efficiency drivers in play, firms that align procurement, product roadmaps, and service models to these dynamics will capture disproportionate value. PW Consulting’s full Combustion Control Equipment Market report converts these macro signals into executable roadmaps and financial templates that senior leaders can deploy immediately.

To access the complete set of models, vendor scorecards, and interactive dashboards referenced in this briefing, visit PW Consulting’s Combustion Control Equipment Market report page. The full intelligence package contains the granular regional, product, and end‑user splits omitted here for confidentiality and to ensure commercial control of the primary datasets.

For detailed analysis of this topic, please visit the official page:Combustion Control Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com