Decoding Alcohol Ingredients Label Information

Other |

2026-03-10 09:30:59

As companies calibrate capital allocation and supply chain strategies for 2026, PTFE lined dip pipes are transitioning from a specialized corrosion-control purchase to a mission-critical engineering and procurement decision. PW Consulting’s latest market study on PTFE Lined Dip Pipes synthesizes five years of market evolution (2020–2025) and a forward-looking forecast (2026–2032) to equip senior leaders with the evidence and frameworks needed to act decisively in the coming 12–18 months.

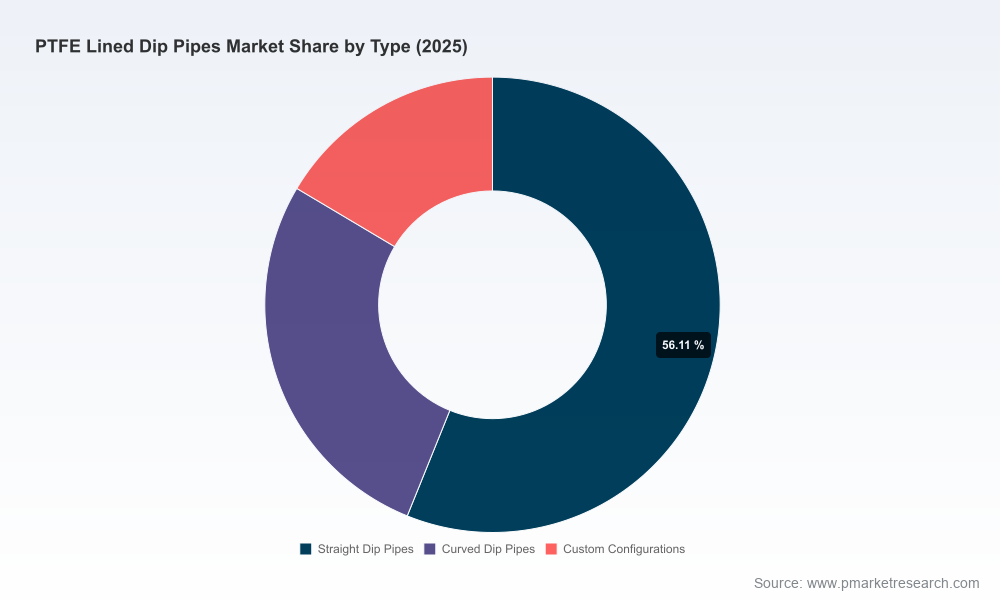

Ptfe Lined Dip Pipes Market

Actionable foresight: The report quantifies market momentum — the global market expanded materially during 2020–2025 and is projected to continue growing at a compound annual growth rate (CAGR) of 5.2% through the 2026–2032 forecast horizon. This trajectory is sufficient to change supplier economics, procurement bargaining power, and the risk profile of long‑lead capital programs.

Ptfe Lined Dip Pipes Market

Decision-ready analysis: Beyond high-level sizing, the study delivers decision templates (supplier scorecards, procurement playbooks, and capex/opex trade-off models) tailored for scenarios common to chemical, pharmaceutical, and water treatment operators.

Ptfe Lined Dip Pipes Market

Concentration and competition: The market displays moderate concentration dynamics (CR3 ~38.5%; CR5 ~51.2%). These metrics indicate meaningful market leadership but also persistent opportunities for niche specialists and new entrants to capture value through technical differentiation or go‑to‑market agility.

From 2020 to 2025 the market moved from a niche engineering commodity toward a recognized strategic component for hazardous and high‑purity fluid-handling systems. PW Consulting’s base-year analysis (2025) captures this maturation. Our forecast through 2032 shows steady expansion, reflecting a mix of replacement demand, regulatory-driven retrofits, and new-build specifications which increasingly mandate corrosion-resistant solutions. For procurement and engineering leaders, the combination of predictable growth and clustered supplier capability creates a narrow window in 2026 to renegotiate terms, resolve single‑source exposures, and embed advanced specification language into upcoming tenders.

Market sizing & methodology: Transparent approach to historical reconciliation (2020–2025) and scenario-driven forecasting (2026–2032), enabling teams to stress-test capital plans under multiple growth and raw‑material scenarios.

Supplier benchmarking: Standardized scorecards covering manufacturing techniques (continuous lining vs. bonded liners), quality certifications, delivery reliability, engineering support, and installed‑base case studies.

Cost-structure analysis: Detailed model of input drivers — notably PTFE resin exposure and labor intensity — showing how raw material pricing volatility can drive 35–45% of manufacturing costs for solid pipe variants and a larger share for lined configurations. The report converts these insights into hedging and inventory strategies tailored to procurement risk appetites.

Regulatory and specification playbook: Traceable map of how evolving environmental and safety regulations (including water‑quality and hazardous‑fluid containment standards) influence product requirements and procurement specifications. The playbook includes recommended contract clauses and inspection regimes that legal and EHS teams can adopt immediately.

Go-to-market and product roadmaps: For manufacturers and OEM partners, actionable guidance on where to invest (e.g., adhesion technologies, lined-jacket assemblies, and high-purity fabrication) and where to avoid commoditization traps.

M&A and partnership screening: Heat maps identifying targets and capability gaps across engineering, coating adhesion technology, and regional manufacturing footprints — designed to accelerate 100‑day integration plans post‑transaction.

Case studies and procurement templates: Real-world negotiation scripts, TCO calculators, and maintenance scheduling to extend in-service life and reduce total cost of ownership.

Our competitive assessment synthesizes technical capability, channel reach, and recent strategic moves across established and emerging players:

Corrosion Resistant Products (CRP): Known for continuously lined designs suitable for agitated services with detailed stress‑calculation capabilities. Their engineering-first approach is a model for buyers who require rigorous mechanical integrity assurances.

Micromold Products, Inc.: Offers a family of lined and jacketed solutions with standard units geared to large nozzle interfaces. Their strength lies in scalable product platforms and aftermarket support for retrofit programmes.

Andronaco Industries (Ethylene): Positions proprietary ChemTite® Ethylarmor® offerings for high‑stress injection environments. Partnerships and distribution agreements (notably recent channel expansions) make them a practical choice for complex vessel interfaces.

Edlon (GMM Pfaudler): Combines PTFE expertise with a focus on high‑purity and glass-lined applications — an option frequently specified by semiconductor and specialty chemical users.

Regional Indian specialists (Ablaze Glass Works, Hi‑Tech Applicator, Polycoat Flowchem, Glass Tef Engineering): These firms are increasingly competitive on lead time and price for standard configurations, and are worth engaging where local content and quick delivery are priorities.

Recent industry developments further color the competitive picture: manufacturers are promoting improved adhesion technologies and manufacturers/distributors are forming partnerships and releasing product guides oriented to high‑purity and semiconductor applications. These moves point to a short cycle of product innovation and rapid specification updates — a factor buyers should monitor closely in 2026 procurement cycles.

Raw material exposure: PTFE resin pricing remains the most immediate cost lever. Procurement teams will need dynamic sourcing playbooks and a clear policy on pass‑through pricing to protect margins without losing competitiveness.

Regulatory tailwinds: Stricter containment and environmental rules are converting one-off retrofit opportunities into multi‑year replacement programs — accelerating demand where operators must comply with updated wastewater and hazardous‑material standards.

Quality vs. cost trade‑offs: The market’s moderate concentration means buyers can extract technical concessions (e.g., extended warranty, third‑party testing, or onsite lining verification) from preferred suppliers — but they must be prepared to consolidate volumes to achieve those terms.

Innovation premium: Suppliers that invest in improved lining adhesion and engineered liners for agitated service command technical premiums. Capital planners should shadow product roadmaps to avoid specification obsolescence.

For procurement leaders: Consolidate spend where quality and delivery risk justifies it, but maintain dual‑source options for critical long‑lead items. Implement a 12–18 month hedging and safety‑stock model for resin exposure and negotiate cost‑variance clauses tied to recognized indices.

For engineering and R&D heads: Prioritize testing protocols that verify long‑term adhesion and stress performance in agitated applications. Specify clear acceptance criteria and require supplier traceability for liner materials.

For corporate development teams: Use our M&A heat maps to identify targets that fill capability gaps (e.g., advanced adhesion tech or regional manufacturing presence) and to run rapid synergy assessments aligned with 100‑day integration objectives.

For plant managers and EHS teams: Reassess asset plans under updated regulation scenarios and deploy the report’s inspection and maintenance templates to extend service life and reduce unplanned downtime.

True to our “trailer” approach, this brief demonstrates the analytical depth and practical orientation of the full study while withholding granular sub‑segment tables and proprietary supplier scoring matrices that are core to tactical decisions. If you are preparing a capital tender, negotiating long‑term supply agreements, or evaluating acquisitions, the full report contains the regional and application split sheets, supplier-specific performance matrices, and downloadable procurement templates you will need to execute with confidence.

Custom briefings: Rapid, confidential sessions to map our findings to your backlog and procurement calendar.

Supplier due diligence: Deep dives into specified vendors, including on‑site audits and technical validation of lining methods and adhesion claims.

M&A advisory: Transaction screening and integration playbooks tailored to PTFE lining technologies and aftermarket service economics.

For procurement, engineering, and corporate development teams preparing for 2026, the decision window is narrow: align specifications, secure supply for resin exposure, and capture technical concessions while market concentration and product innovation remain in flux. PW Consulting’s Ptfe Lined Dip Pipes Market report turns the macro trajectory and competitive reality into ready‑to‑use action plans. Contact us to access the full report and receive tailored support to convert insight into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Ptfe Lined Dip Pipes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com