Fractional Horsepower (FHP) Motors Market Outlook, Growth Trends & Forecast

Other |

2026-05-22 08:35:45

PW Consulting today publishes its latest market intelligence on Tris(trimethylsilyl)amine (TTMSA), providing senior executives, corporate strategy teams, and investment committees with a concise yet deeply practical roadmap for decision-making as 2026 begins. This brief draws from our full Tris(trimethylsilyl)amine Market report (base year 2025), which combines rigorous data modeling, primary supplier engagement, and scenario-based strategic tools designed to convert chemical market insight into executable actions.

Tristrimethylsilylamine Market

The Tris(trimethylsilyl)amine market has demonstrated steady expansion through the first half of the decade. Our historical series (2020–2025) shows growth from approximately USD 24.8 Million in 2020 to USD 32.45 Million in 2025, reflecting recovery and structural demand from electronics and specialty-chemicals end markets. Looking forward, our baseline forecast (2026–2032) projects the market to expand at a compound annual growth rate (CAGR) of 5.5%, with the total market expected to reach roughly USD 47.2 Million by 2032 under the base-case scenario.

Tristrimethylsilylamine Market

For corporate leaders, 2026 is the inflection point where strategic initiatives conceived during the post-pandemic recovery must be operationalized. That includes aligning commercial models to changing purity requirements, reconfiguring supply chains to mitigate raw-material volatility, and setting R&D and capital priorities in line with evolving end‑use demands.

Tristrimethylsilylamine Market

Market momentum and short-term volatility — The historical series registers modest year-on-year volatility driven by episodic manufacturing disruptions and inventory adjustments across fine-chemical distributors. Notably, a compression in 2023 demonstrates how inventory cycles and downstream project delays can temporarily decelerate growth even as structural demand persists.

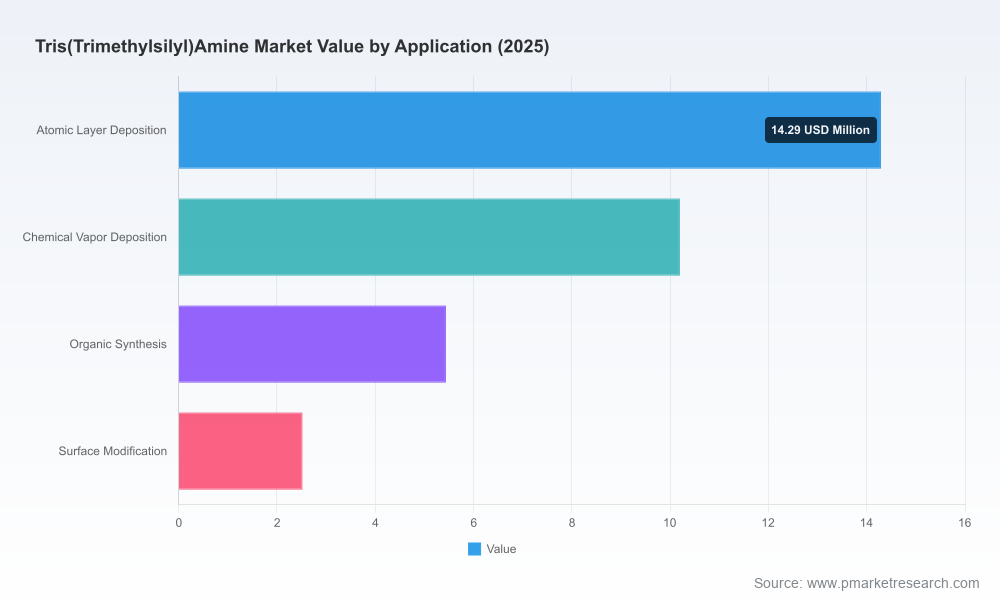

Demand composition — TTMSA’s use in semiconductor-related deposition processes and organosilicon synthesis has been a primary growth engine. Demand heterogeneity between high-purity electronic-grade reagents and industrial-grade variants creates differentiated pricing and margin dynamics that suppliers must manage.

Regulatory and labeling considerations — TTMSA is registered under the EU REACH framework, and major suppliers consistently label product offerings for research use only rather than for direct consumer or pharmaceutical use. These regulatory and labeling realities shape go‑to‑market pathways, customer qualification, and documentation controls required by procurement and compliance teams.

Market concentration — Supply remains moderately concentrated among a set of specialty chemical suppliers and distributors, which influences bargaining power, product availability, and the pace of new capacity introductions.

Our report is designed as an operational toolkit for action, not merely a descriptive document. Key deliverables include:

Proprietary market sizing and a 2026–2032 forecast model with sensitivity testing — users can stress-test demand under alternative scenarios (slower electronics capex, accelerated greenfield semiconductor fabs, feedstock price shocks) to quantify revenue and margin implications.

Supply-chain and cost-driver analysis — end-to-end mapping from key precursors through synthesis, packaging, and distribution, highlighting pinch points and cost levers that materially affect supplier margins and customer pricing.

Regulatory and compliance playbook — practical checklists to navigate REACH obligations, supplier qualification protocols, and RUO labeling constraints that impact commercial pathways for different buyer segments.

Commercial and procurement playbooks — play-by-play guidance on negotiation priorities, volume commitments, contract structuring, and inventory policies tailored to specialty reagents where lead times and purity specs matter.

M&A and partnership framework — criteria and valuation heuristics for investors and corporate development teams seeking bolt-on acquisitions, toll‑manufacturing partnerships, or distribution alliances in the specialty silicon-chemicals space.

Supplier scorecards and capability benchmarking — practical templates and scored profiles that help buyers and strategic teams rapidly assess fit on dimensions such as purity ranges, packaging sizes, technical support, and scale-up capability.

Our competitive analysis synthesizes supplier positioning, product portfolios, and channel strategies observed in the market. Core suppliers identified through primary research include both global life-science supply houses and specialty silicon-chemicals firms. Representative profiles include:

Merck KGaA (MilliporeSigma), Darmstadt, Germany — operates as a major laboratory and specialty‑chemicals merchant supplying TTMSA at research quantities and defined purities for organic synthesis, often leveraging broad distribution through laboratory channels.

Thermo Fisher Scientific (Alfa Aesar), Waltham, MA, USA — provides high-purity formulations targeted at organosilicon chemistry and fine‑chemical synthesis; strong in catalog distribution and technical service to R&D teams.

Tokyo Chemical Industry (TCI), Tokyo, Japan — focuses on research and process-development markets with a stable of silylating agents and technical application notes for laboratory workflows.

Gelest, Inc., Morrisville, PA, USA — a niche specialist in silicon-based reagents and advanced materials applications; positioned to serve surface-modification and materials R&D with technical depth.

ABCR GmbH & Co. KG, Karlsruhe, Germany — strong regional distributor channel with capabilities in supporting organometallic and specialized organic-chemistry research demand.

Apollo Scientific Ltd., Stockport, UK — supplies building blocks and trial-scale quantities for pharmaceutical and agrochemical intermediates, emphasizing adaptability to customer-specified pack sizes and purity grades.

Across these providers, competitive differentiation rests on (1) ability to supply higher-purity electronic-grade material versus broader industrial-grade offerings; (2) scale and reliability of supply; (3) technical support and documentation for regulated applications; and (4) channel reach into fabs, CROs, and custom-synthesis partners. Our full supplier scorecards — included in the report — enable side-by-side comparisons but are shared only in the full report to preserve commercial sensitivity and encourage direct engagement with supplier data.

Corporate strategy: Use the forecast scenarios to calibrate capital-allocation choices. The mid-single-digit CAGR in our baseline calls for selective capacity expansion tied to confirmed offtake or toll-manufacturing agreements rather than broad greenfield investments.

Procurement and operations: Implement a supplier segmentation that separates strategic suppliers (long-term, high-purity needs) from tactical spot-supply sources. Our procurement playbook provides contract templates and inventory-safety heuristics customized for specialty reagents.

R&D and product management: Align synthesis roadmaps with the two primary demand vectors — advanced materials deposition processes and organosilicon synthesis — to prioritize formulations and batch-release criteria that will command premium pricing.

M&A and corporate development: Prioritize targets with technical scale-up capability and documented compliance frameworks; our valuation model flags synergies based on purity differentiation and distribution footprint.

Risk and compliance: Incorporate our regulatory checklist into supplier onboarding and change-control processes to avoid downstream disruptions related to documentation gaps or regulatory reclassification.

PW Consulting’s analysis combines bottom-up shipment modeling, primary interviews with suppliers and buyers, and cross-validation against import/export flows and trade datasets. The report’s base year is 2025; historical coverage extends 2020–2025 and a 2026–2032 forecast horizon. We provide transparent assumptions and an interactive forecast model with sensitivity levers so clients can adapt scenarios to their internal planning assumptions.

We recognize the importance of usable outputs: alongside narrative analysis, clients receive excel-ready datasets, model logic notes, and an executive slide deck for board-level briefing. To protect commercial confidentiality and to preserve the utility of the report for strategic negotiation, certain granular segmentation tables and supplier market-share tables are accessible only in the full report delivery.

Lock in supply for high-purity grades through multi-year agreements if your roadmap includes advanced-deposition or semiconductor-related applications; the market’s projected mid-single-digit growth does not eliminate episodic tightness.

Adopt a staged-capex approach for any planned scale-up: validate demand through firm offtakes and pilot volumes before committing to dedicated production lines.

Invest in documentation and regulatory readiness now — REACH registration and RUO labeling remain central to market access, especially for cross-border shipments into stringent regulatory jurisdictions.

Use supplier scorecards to prioritize partners who combine scale with application support; the ability to co-develop specs and provide technical backing materially reduces cycle times for new process adoption.

This release is intended as a strategic teaser: it demonstrates the analytical depth and practical orientation of PW Consulting’s Tris(trimethylsilyl)amine Market report while reserving detailed segmentation tables, supplier market shares, and downloadable forecast models for report subscribers. Senior decision-makers and procurement leaders who require the full dataset, interactive models, and supplier scorecards are invited to contact PW Consulting to request access to the full report and a tailored briefing.

For organizations preparing budgets, negotiating supplier agreements, or evaluating M&A targets in 2026, the report provides a defensible, data-driven foundation to move from strategy to execution with confidence.

For detailed analysis of this topic, please visit the official page:Tristrimethylsilylamine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com