Asia-Pacific Trash Bags Market Dynamics: Key Drivers and Restraints

Other |

2026-05-21 11:07:45

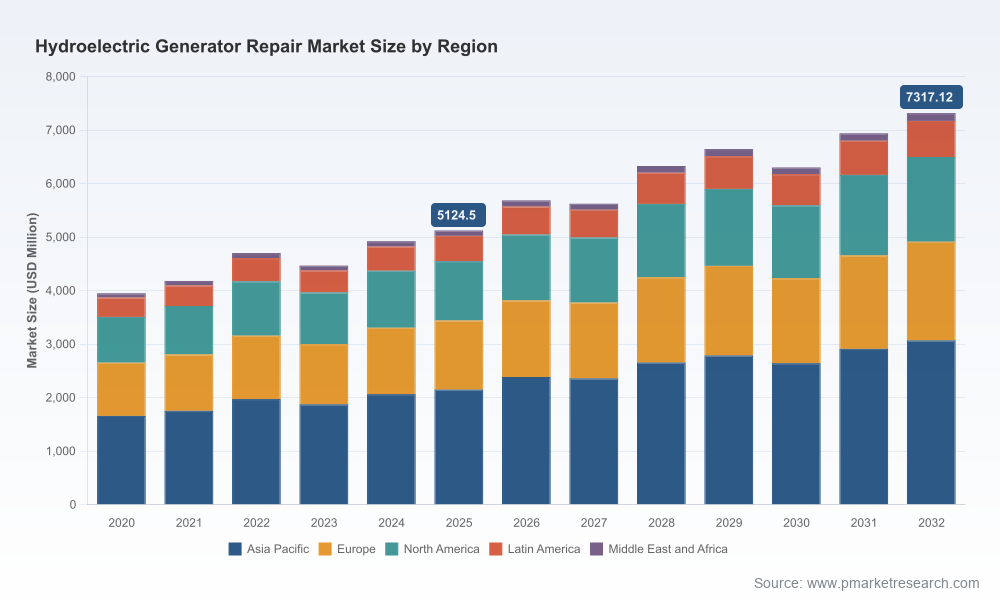

PW Consulting’s latest market study on the Hydroelectric Generator Repair Market distills five years of historical performance and a seven-year forecast into an actionable strategic playbook for 2026 decision‑makers. Built on a 2025 base year and a forecast horizon through 2032, the report projects a compound annual growth rate (CAGR) of 5.22% and models the market’s evolution from a 2025 baseline of USD 5,124.5 Million to over USD 7,300 Million by 2032. This brief highlights why these macro dynamics matter for corporate strategy in 2026, what operational and commercial levers will determine winners, and how companies should prioritize investments — while deliberately reserving proprietary segment-level metrics for the full report.

Hydroelectric Generator Repair Market

Mid-cycle capital rollouts and refurbishment programs are converging with new policy incentive windows and tightening raw-material supply chains. The result: a market that is growing at a steady mid-single-digit CAGR, but whose value capture will be strongly dependent on supply‑chain resilience and service innovation.

Hydroelectric Generator Repair Market

Public-sector activity and large project solicitations announced through early 2026 are accelerating demand for high-complexity repairs, digital retrofits, and turnkey modernization — favoring firms that can combine engineering depth with field execution agility.

Hydroelectric Generator Repair Market

Competitive intensity is moderate: market concentration metrics show a fragmented to semi-consolidated landscape. The top three players do not dominate, and the top five together capture less than half of spend, creating room for regional specialists, engineered-service providers, and asset-owners’ internal teams to influence outcomes.

Aging asset base: Nearly 40% of the global hydro fleet exceeds four decades in service. That creates persistent demand for generator rewinds, rotor refurbishments, bearing replacements, and unit-specific modernization to meet new grid services requirements.

Policy and capital incentives: Recent stimulus and infrastructure programs have unlocked meaningful co‑funding for refurbishments and efficiency upgrades. Companies that can align proposals to incentive eligibility and demonstrate measurable efficiency gains are advantaged in competitive tenders.

Raw-material volatility and lead times: Copper and steel remain critical inputs. Recent year‑over‑year producer price moves and extended lead times for specialized components materially affect repair economics, margins, and scheduling. Procurement and design choices made in 2026 will determine margin resilience through the forecast horizon.

Service model bifurcation: Operators increasingly choose between full OEM-led modernization and mixed-supply strategies that combine OEM parts with independent field-service providers. The market rewards interoperability, rigorous testing, and low‑risk mobilization capabilities.

Portfolio prioritization — Capex vs. Opex: The forecasted steady growth supports a disciplined approach: prioritize high-return uprates and refurbishment programs that lengthen asset life and enhance flexibility (e.g., frequency response capability). For marginal units, favor targeted repairs and digital upgrades that defer heavy capex while unlocking ancillary revenue streams.

Supply-chain strategy: Locking long‑lead items and qualifying multiple sources for copper-intensive subassemblies should be a priority. Consider hedging strategies for critical materials and adapt procurement contracts to include price‑adjustment clauses tied to recognized indices.

M&A and partnership focus: Given the market’s moderate concentration and the reliance on specialized field capabilities (in‑situ machining, bearing line boring, complex rewind), strategically targeted acquisitions or alliances can rapidly scale geographic reach and technical capability at lower organic cost.

Digitization and aftermarket services: Investing in diagnostic tools, condition-monitoring, and predictive‑maintenance services generates recurring revenue and differentiated service contracts. These capabilities also shorten outage windows and improve bid competitiveness on major refurbishments.

Competitive tendering playbook: Proposals that bundle engineering, local execution, and financeable performance guarantees (availability, efficiency gain, outage duration) will win in government and utility procurements announced in early 2026.

The repair market is served by a mix of global OEMs, specialized engineering houses, and regional service providers. Each cohort brings distinct advantages — but also execution tradeoffs:

Global OEMs (e.g., ANDRITZ HYDRO, Voith Hydro, GE Vernova): Offer full electromechanical solutions, deep engineering bench strength, and name‑plate credibility on large upgrades. Their strengths lie in turnkey modernizations and integration of new-generation generator designs. However, they face challenges on price flexibility and rapid local deployment.

Independent specialists (e.g., Goltens, RESA Power, Jenkins Electric, HECO): Excel at in-situ repairs, rapid field mobilization, and cost-competitive rewinds / overhauls. These providers often compete effectively on short-notice outages and smaller unit refurbishments where logistics and speed trump large-scale project integration.

Industrial integrators and emerging players (e.g., Nidec ASI, Ansaldo Energia, Metalock Engineering): Bridge OEM capabilities with flexible service delivery models. Their positioning is attractive for asset owners seeking upgrades without full OEM lock-in.

Recent market activity underscores these dynamics. Examples from early 2026 include large public-sector overhauls and solicitations for turbine and generator work that signal increased procurement activity and an appetite for digital modernization. These developments favor suppliers who present clear risk mitigation, proven field records, and financing-aligned commercial terms.

Standardize modular retrofit packages: Define repeatable productized offerings for common repair scopes (stator rewinds, rotor machining, bearing upgrades) that reduce engineering hours and accelerate mobilization.

Implement predictive maintenance pilots: Deploy sensors and analytics on a subset of units to demonstrate reduction in unplanned outages and to create data-led case studies that support premium service contracts.

Strengthen local execution capacity: Invest in mobile machining assets, certified field crews, and regional spare pools to shorten lead times and improve tender hit rates.

Refine cost‑plus and performance-based contracts: Offer hybrid models that share upside from efficiency gains while protecting margins against raw-material inflation.

Our full study is structured to be immediately practical for teams executing 2026 programs. It contains:

Market sizing and validated forecast model (base year 2025) with scenario analytics to stress-test investment cases.

Value-chain mapping and supplier cost drivers, including materials, machining, and testing bottlenecks.

Procurement templates, RFP language examples tailored to public and private owners, and a bid/no-bid decision framework.

Commercial models contrasting capex-heavy upgrades vs. service-led modernization pathways and indicative project-level IRR sensitivities.

Vendor benchmarking and capability matrices covering engineering competence, field capacity, digital offerings, and geographic reach for all major providers.

Case studies and playbooks: end‑to‑end mobilization, outage reduction strategies, and lessons from recent large public projects and utility programs.

Risk registers and mitigation checklists focused on raw-material volatility, long-lead times, regulatory compliance, and environmental permitting.

Public-sector procurement calendars and the release of incentive tranches under infrastructure programs — these will drive line-of-sight demand and affect pricing dynamics.

Raw-material pricing indexes for copper and brass mill shapes: sharp movements will necessitate rapid contract re-pricing or design substitution strategies.

Mobilization success on high-visibility projects: early wins by service integrators on complex overhauls will catalyze further market share gains.

For executives evaluating capital plans and service strategies in 2026, the choice is clear: act now to lock supply, productize repeatable repair scopes, and build the digital and field capabilities that transform one-off projects into recurring revenue streams. The Hydroelectric Generator Repair Market is growing steadily — the edge will go to organizations that combine engineering credibility with agile delivery and procurement savvy.

PW Consulting’s full report contains the proprietary segment-level insights, supplier scorecards, and executable templates that boards and operational leaders need to translate the 2026 opportunity into durable competitive advantage. To access the complete intelligence suite and the detailed models that underlie our forecasts, please visit our report page.

For detailed analysis of this topic, please visit the official page:Hydroelectric Generator Repair Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com