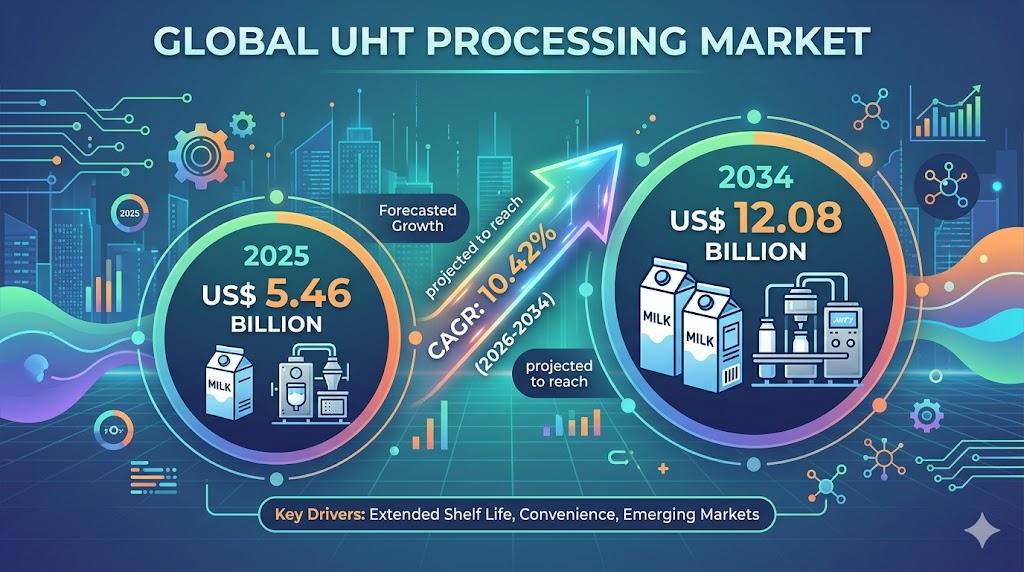

North America Accounts for the Highest Share in UHT Processing Market by 2034

Other |

2026-05-18 15:55:17

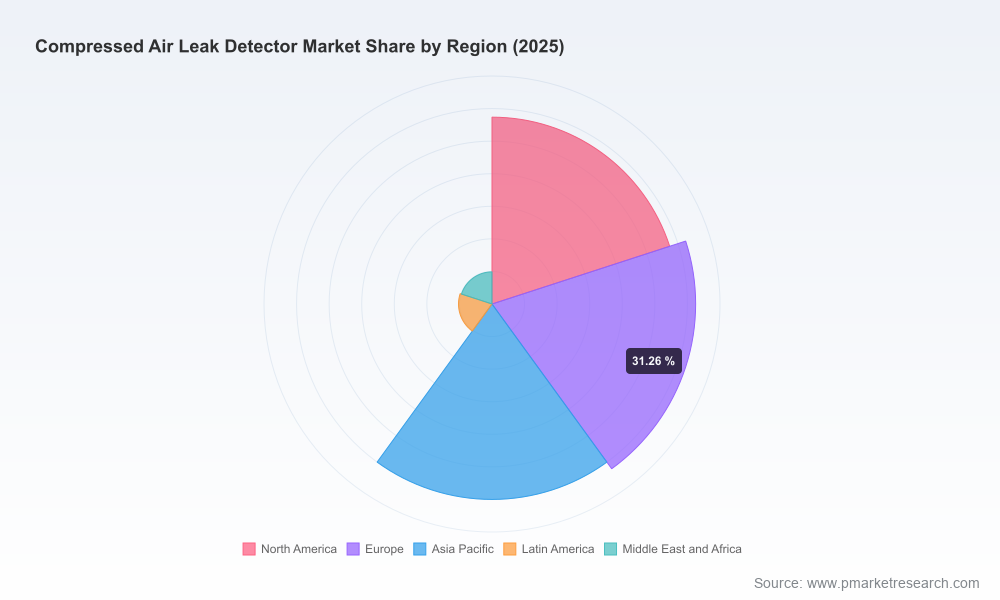

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I’m pleased to release our executive brief for the Compressed Air Leak Detector market, prepared as a companion to our full 2026 Market Research Report. Built on a five‑year historical foundation and a forward-looking 2026–2032 forecast, this brief highlights the strategic implications decision‑makers must resolve in 2026. The market has grown from USD 325.4 Million in 2020 to USD 437.48 Million in 2025 (base year), and our model projects continued expansion to USD 693.35 Million by 2032 — a compounded annual growth rate of 6.8% that underpins a broad set of commercial and operational choices for equipment manufacturers, system integrators, end users and investors.

Compressed Air Leak Detector Market

Energy and regulatory pressure are converging. Industrial energy‑management frameworks (notably ISO 50001) and air‑quality standards (ISO 8573‑1) are turning leak detection from a discretionary project into a compliance‑adjacent performance lever. Facilities that treat leak detection as part of their energy and purity governance programs are realizing measurable operational advantages.

Compressed Air Leak Detector Market

Technology is changing the economics of detection. Advances in ultrasonic sensors, MEMS microphones and acoustic imaging, coupled with improved analytics, are expanding the addressable use cases — from line‑of‑site walk‑downs to continuous, non‑intrusive monitoring architectures. These technology shifts explain much of the market momentum embedded in our 6.8% CAGR view.

Compressed Air Leak Detector Market

Service and software are replacing one‑time transactions. Buyers increasingly prioritize solutions that combine detection hardware with analytics, reporting, and ISO‑compliant documentation. This effectively enlarges lifetime value and tilts the competitive playing field toward firms that can pair detection hardware with repeatable services.

Consolidation and product innovation are accelerating. Strategic M&A and targeted product launches in 2025–2026 signal that incumbents and challengers are repositioning — not solely on device cost, but on system integration, data outputs, and downstream verification (energy savings calculations, ISO reporting).

We designed the full report as an operator’s manual for 2026 decisions. Key practical deliverables include:

Proprietary market model (2020–2032) with transparent assumptions and scenario toggles for energy prices, industrial production indices, and regulatory tightening.

TCO and ROI calculators calibrated to common industrial profiles; templates permit quick assessment of payback thresholds for handheld, imaging and embedded sensor approaches.

Go‑to‑market playbooks for product managers: product positioning, channel economics, pricing strategies and feature prioritization for ISO‑centric buyers.

Operational deployment blueprints: pilot design, measurement protocols, acceptance criteria and verification templates suitable for ISO 50001 reporting.

Technology roadmap and supply‑chain risk register focused on MEMS microphone and ultrasonic sensor availability, part obsolescence mitigation, and manufacturing scale considerations.

Competitive benchmark and capability matrix that maps vendor strengths across detection range, imaging vs. point measurement, analytics maturity and service delivery models (note: aggregated segment splits and detailed vendor revenue shares are available only in the full report).

The market exhibits moderate concentration: the top three players account for a meaningful share of revenue, and the top five consolidate an even larger portion. This structure creates two simultaneous dynamics — room for differentiated challengers and meaningful barriers for late movers. Our CR3 and CR5 analysis indicates incumbent advantages in channel reach and enterprise procurement relationships, but also leaves windows for technology or service‑led disruption.

Representative vendor profiles and strategic positions we analyze in depth include:

Teledyne FLIR — Known for acoustic imaging cameras that combine long‑range ultrasonic sensing with visual overlays, positioning the company for high‑value, asset‑intensive accounts that require rapid localization and documentation.

UE Systems — A specialist in ultrasonic detection with a broad handheld and imaging portfolio, focused on practical leak quantification and on‑site energy savings calculations favored by maintenance teams.

EXAIR Corporation — Offers lower‑distance handheld ultrasonic tools optimized for plant technicians, emphasizing straightforward operation and cost efficiency for routine walk‑downs.

CS Instruments — European developer with comprehensive features for ISO reporting and cost calculations, appealing to facilities integrating leak programs into formal energy management systems.

Superior Signal Company — A value‑oriented U.S. manufacturer promoting high performance at lower price points, focused on cost‑conscious buyers.

SUTO iTEC — Active in product showcases and imaging solutions, building momentum in markets receptive to combined ultrasonic and acoustic imaging systems.

LeakMaster — Offers both detection hardware and automated leak‑test systems, with relevance for OEMs and automated test lines.

OptiNav — Provides acoustic cameras suitable for mobile and static workflows; differentiation rests in non‑intrusive visualization and user ergonomics.

SDT Ultrasound — Focused on robust ultrasound solutions tailored for noisy industrial environments where classic detection approaches underperform.

Recent industry moves underscore our market thesis. Strategic acquisitions by larger industrial players, targeted product launches of next‑generation leak testers, and aggressive promotion of acoustic imagers by established test‑and‑measurement brands show simultaneous consolidation and feature competition. These actions validate the shift toward integrated detection + reporting solutions and raise the bar for entrants without robust after‑sales or analytics capabilities.

Energy management compliance (ISO 50001) is increasingly framed around documented interventions — leak detection programs that can show demonstrable reductions are more likely to receive CAPEX approval.

Air purity concerns (ISO 8573‑1) make leak management a cross‑functional responsibility in process‑sensitive industries (e.g., food, pharmaceuticals, semiconductors), accelerating demand for documented detection and remediation workflows.

Operational targets: many facilities still aim to reduce leaks to the 5–10% range of total system flow; this simple operational KPI continues to be the dominant economic argument for detection investments.

Component supply stability (MEMS microphones, ultrasonic transducers) is currently supportive but requires active management; product roadmaps should include alternate BOMs and multi‑sourcing strategies.

Shift to system value: vendors should bundle detection hardware with analytics, reporting and verification services to drive recurring revenue and stickiness.

Design for standards: prioritize features and reporting flows aligned to ISO 50001 and ISO 8573‑1 to reduce procurement friction for critical buyers.

Operationalize pilots: use our report’s pilot templates to demonstrate short payback periods and create repeatable case studies that accelerate scaling inside multi‑site accounts.

Protect supply chains: implement part‑substitution and dual‑sourcing strategies for MEMS and ultrasonic transducers to maintain product cadence.

Explore adjacencies: service providers and integrators should pair leak detection with compressed‑air system optimization services to expand contract value.

Screen M&A targets pragmatically: investors should prioritize targets with embedded services, strong channel relationships and data‑enablement features that can be scaled across industrial accounts.

For executives preparing 2026 plans, the report serves four immediate functions:

Capital allocation: prioritize spending into product features and go‑to‑market motions that maximize recurring revenue and reduce procurement friction.

M&A screening: focus on targets that fill gaps in analytics, channel access or compliance reporting rather than purely hardware‑only businesses.

Procurement and piloting: use our TCO/ROI templates to accelerate internal approvals by translating detection projects into verified energy and cost savings.

Channel strategy: align distribution and service partners to offer bundled hardware + managed detection services, capturing larger portions of the total addressable revenue.

This brief highlights the strategic threads that will matter in 2026: regulatory alignment, technology‑driven economics, service‑oriented business models and selective consolidation. The full PW Consulting Compressed Air Leak Detector Market Report contains the granular segmentation, regional and application splits, vendor revenue shares, and downloadable modeling spreadsheets you need to execute with conviction. We intentionally withhold the detailed segment tables and vendor revenue line items from this public summary to ensure you receive the complete, source‑level datasets and implementation assets available through the report.

To access the full report, model files, and our ready‑to‑use pilot templates, please visit the PW Consulting research portal. Our team is available to provide tailored briefings and to workshop a 90‑day action plan based on your role — whether you are a product leader, operations executive, systems integrator or investor targeting the compressed‑air efficiency value chain.

For detailed analysis of this topic, please visit the official page:Compressed Air Leak Detector Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com