Extended Detection And Response Market Insights in Threat Hunting

Other |

2026-04-09 07:43:34

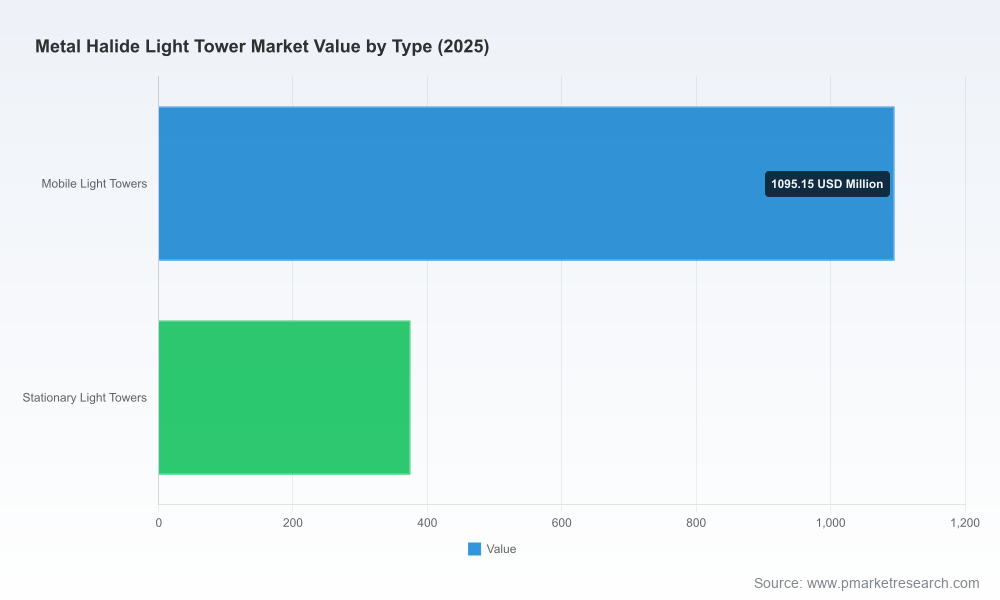

Our latest market intelligence on metal halide light towers synthesizes proprietary modeling with a deep primary research program covering manufacturers, rental fleets, OEM suppliers and end-users across construction, mining, oil & gas and emergency services. Using 2025 as the analytical base year, the global market is valued at approximately USD 1,470 Million and is forecast across a 2026–2032 horizon at a compound annual growth rate (CAGR) of 2.81%, reaching just under USD 1.8 Billion by 2032. This brief highlights the report’s strategic value for decisions to be taken in 2026 — capital allocation, fleet strategy, procurement design, regulatory compliance and M&A — while intentionally withholding granular segment-level datapoints to encourage direct engagement with the full report for transaction-grade detail.

Metal Halide Light Tower Market

Operational intensity and asset longevity. Metal halide light towers remain the technology of choice where very high lumen output and large-area coverage are non‑negotiable (notably heavy civil works, large-scale mining and critical turnaround projects). That technical advantage is preserving demand even as alternative lighting technologies mature.

Metal Halide Light Tower Market

Regulatory and emissions pressure. Diesel-driven light towers are increasingly subject to emissions standards in major markets — in the U.S., Tier 4 Final compliance for construction and industrial equipment is now table-stakes for deployed fleets. This regulatory overlay affects lifecycle cost, secondary-market value and retrofit requirements.

Metal Halide Light Tower Market

Supply-side dynamics. Metal halide lamps rely on specialized components — metal halide compounds and quartz arc tubes — embedded in a broader lamp supply chain that itself is substantial (lamp market estimates reached roughly USD 2.32 Billion in 2025). Raw material availability and component lead times are therefore important risk factors for procurement planning.

PW Consulting’s full report is structured to be a practitioner’s toolkit rather than an academic exercise. Highlights include:

Clear market sizing and scenario forecasts (historical run 2020–2025; base year 2025; forecast 2026–2032), presented in USD Million and stress-tested across demand and regulatory scenarios.

Cost-of-ownership models and payback calculators tailored for ownership versus rental strategies, accounting for fuel, maintenance, lamp replacement cycles and emissions compliance costs.

Procurement frameworks and RFP templates designed for fleet buyers and rental companies — including vendor scorecards, total cost of service (TCOS) metrics and spare-parts inventory guidance.

Risk matrices covering supply chain concentrations, critical component lead times, and mitigation playbooks for sourcing continuity.

Regulatory checklists and retrofit pathways to map compliance investments (e.g., engine upgrades, emissions controls) to residual value outcomes and operational schedules.

Deal-desk materials for corporate development teams: target screening criteria, valuation sensitivities tied to fleet composition, and integration checklists for bolt-on acquisitions.

The market exhibits a moderate concentration among established OEMs and specialist suppliers. Our analysis emphasizes product architecture (mast design, lumen output), ruggedization for rental and mining applications, rental channel penetration, and service network depth.

Atlas Copco (Stockholm, Sweden) — Offers robust portable units with high-output metal halide fixtures and heavy-duty canopies geared toward quarry and rental environments. Strengths: brand, durability and rental-focused options.

Generac Mobile / Magnum (Waukesha, WI, USA) — Known for compact vertical mast designs and modular lamp banks targeted at construction and industrial contractors. Strengths: product breadth and familiarity with North American construction standards.

Wacker Neuson (Munich, Germany) — Delivers vertical-mast towers suitable for job-site utility and event applications with options for metal halide lamps. Strengths: integration with compact equipment portfolios and dealer networks.

Grandwatt Electric Corp (USA/China operations) — Focus on custom and standard configurations serving project-specific lighting requirements. Strengths: customization and China-based manufacturing flexibility.

Boss LTG (Baton Rouge, LA, USA) — Produces heavy-duty trailer-mounted towers with very high lumen outputs for mining and industrial turnarounds. Strengths: high-output products and industrial market orientation.

DMI Light Towers (Greenwell Springs, LA, USA) — Offers very large portable towers capable of covering extensive areas, addressing heavy industrial sites. Strengths: extreme coverage and bespoke large-site solutions.

Trime USA (part of Trime Group) — Mobile towers with modular lighting options targeting construction and industrial buyers. Strengths: European engineering pedigree and adaptable product lines.

Larson Electronics (Kemp, TX, USA) — Supplies portable tower solutions, including units built for hazardous areas and high-lumen output needs. Strengths: application-specific offerings and catalog breadth.

Market concentration metrics indicate that a small number of suppliers command significant but not overwhelming shares, creating space for mid-tier players and specialized manufacturers to scale through channel partnerships, rental fleet contracts and targeted product differentiation.

Independent market syntheses published in late 2025 and updated in early 2026 underline sustained demand pockets in construction, mining and events while highlighting a diversified supply architecture — a sign that procurement teams should be prepared to manage multi-supplier relationships and inventory redundancy.

Regulatory updates and emissions enforcement are increasing the relative attractiveness of retrofit and hybridization projects for fleet owners seeking to maintain metal halide performance for high-intensity tasks while reducing environmental costs on lower-intensity deployments.

Critical-component scarcity: metal halide compounds and quartz arc tubes are specialty items; buyers should map lead times and dual-source where feasible.

Engine and emissions compliance: Tier 4 and equivalent standards affect acquisition choices and residual values; budgeting for compliance retrofits is essential.

Service network depth: downtime is costly on large projects; prioritize vendors with proven field service coverage or secure third-party maintenance contracts.

Conduct a fleet audit tied to use-case intensity: identify assets that must remain metal halide for performance reasons versus those that can transition to LED/hybrid solutions.

Adopt a staged retrofit strategy: prioritize emissions or engine upgrades where regulatory exposure or resale impact is highest.

Structure procurement as outcome-based contracts: shift toward “light-as-a-service” models with SLA-driven availability, particularly for intermittent high-intensity needs common in events and turnarounds.

Build a multi-sourcing playbook: secure alternatives for critical lamps and engine components to reduce single-supplier exposure.

Evaluate M&A and partnership opportunities among mid-tier suppliers to accelerate product line diversification or geographic expansion in regions where rental penetration is expanding.

Stress-test capital plans against the report’s three scenario outcomes (base, accelerated adoption of alternatives, and regulatory-intensified) to quantify downside on stranded assets.

For corporate development and procurement teams, the report provides deal-level input — valuation sensitivities tied to fleet composition, contract diligence templates, and integration checklists for acquired rental fleets. For operations and maintenance leaders, there are actionable O&M playbooks, spare-parts optimization matrices and retrofit cost templates. For investors and strategy teams, our scenario-based forecasts (2026–2032) offer the forward-looking revenue and demand curves needed to underwrite growth plans and re-pricing strategies.

This communication follows the “preview” principle: it demonstrates the analytical rigor and practical utility of PW Consulting’s study while withholding granular regional, type and application splits that are included in the full report and interactive model package. Organizations preparing 2026 capex budgets, procurement cycles or portfolio optimization reviews should request the full report to access transaction-ready spreadsheets, supplier scorecards and the complete segmentation dataset necessary for operational implementation.

For immediate strategic use, consider commissioning a tailored workshop with our industry specialists to translate the global forecast into a localized action plan aligned with your asset base, regulatory exposure and growth ambitions.

For detailed analysis of this topic, please visit the official page:Metal Halide Light Tower Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com