High Performance Liner Release Paper Market — 2026 Strategic Brief

PW Consulting’s new High Performance Liner Release Paper Market report (base year 2025) is designed as an executive playbook for commercial leaders, procurement heads, and corporate strategists preparing for critical decisions in 2026. Drawing on a five‑year historical foundation (2020–2025) and a forward-looking forecast through 2032, the study translates market movements into actionable choices. The market’s aggregate trajectory — rising from a multi‑hundred million USD base in 2025 and expected to expand at a compound annual growth rate (CAGR) of 6.1% over the forecast window — frames both opportunity and strategic urgency for incumbent producers, converters, and end‑users of high‑performance release liners.

High Performance Liner Release Paper Market

Why this report matters for 2026 decision cycles

- Timing of strategic commitments: 2026 is a pivotal year for capex, supplier consolidation, and product road‑mapping decisions. The combination of moderate, sustained market growth and accelerating regulatory pressure means decisions made now will determine cost position and market access over the next funding cycle.

- Regulation as a re‑rating catalyst: New packaging regulations and Extended Producer Responsibility (EPR) schemes across major jurisdictions are reshaping product specifications, recyclability requirements, and reporting obligations. The report models regulatory scenarios and quantifies their likely impact on manufacturing cost, material selection, and end‑market demand elasticity.

- Supply chain risk and margin preservation: Volatility in pulp and silicone pricing continues to be the principal input risk. The study provides practical hedging frameworks and procurement levers that procurement teams can deploy to protect margin without sacrificing customer service levels.

What’s in the box — practical, decision‑grade content

- Market sizing and forward demand pathways: Our baseline and alternate scenarios quantify industry scale from the 2020–2025 historical period into a 2026–2032 forecast horizon (figures expressed in USD Million). These models isolate secular demand drivers from cyclical noise to support budgeting and ROI calculations.

- Commercial playbooks by end‑use: Actionable route maps for labelstock, medical adhesives, hygiene, electronics and industrial composites — covering go‑to‑market positioning, value‑based pricing levers, and channel strategies tailored to long and short release formulations.

- Technology & product roadmaps: Comparative analysis of substrate types and silicone systems (including emulsion, solvent‑based, solvent‑free, and curing technologies) that influence coating compatibility, release performance, and recyclability. We outline where incremental R&D spend yields the greatest commercial lift.

- Supply chain and raw material playbooks: Scenario planning for pulp and silicone input price swings, logistics shocks, and regional capacity constraints, plus recommended sourcing strategies — from long‑term offtake agreements to regional buffer capacity and collaborative inventory models.

- Regulatory impact assessment and compliance checklist: A step‑by‑step compliance path for EPR and emerging packaging rules, including cost pass‑through options, circular‑economy product designs, and documentation requirements that buyers and producers must embed into contracts and product specifications.

- M&A and partnership screening: A pragmatic screening matrix to prioritize targets by strategic fit (technology, footprint, customer access), integration complexity, and expected return timeline — useful for corporates seeking inorganic scale or technology tuck‑ins.

- Benchmarking pack: KPIs and cost curves for operations, coating efficiency, silicone usage, and recyclability performance — enabling internal performance gaps to be quantified and prioritized for improvement.

Competitive dynamics — what the leading players signal

The release liner ecosystem remains a mix of global specialty paper producers, regional converters, and vertically integrated suppliers. Market concentration metrics indicate a market with meaningful national and regional champions but room for mid‑market consolidation: the top three firms control a significant share of value, and the top five deepen that footprint further. This balance creates win‑wins for scale players who invest in differentiation and for nimble specialists who can capture premium niches.

High Performance Liner Release Paper Market

- Incumbent innovation leaders: Several legacy paper and specialty materials groups continue to invest in product families tailored for sustainability and higher technical performance. Recent product introductions designed for improved recyclability and optimized silicone anchoring underscore that innovation remains an important route to defend margins.

- Coating and chemistry competency: Producers that couple base paper expertise with advanced silicone systems (from solvent‑free processes to UV/thermal cure technologies) enjoy superior release control and lower total cost‑of‑ownership for customers — a growing selection criterion for major brand owners.

- Trade shows and ongoing commercialization: Active participation in specialist events remains a reliable bellwether of pipeline development and customer engagement intensity; companies using trade platforms effectively accelerate adoption of novel liner formats.

Signals from recent developments

- Product launches that emphasize recyclability and improved silicone anchoring demonstrate that sustainability and performance are no longer trade‑offs; market leaders are pushing double‑sided recyclable liners and optimized base papers to maintain access to regulated markets.

- New base‑paper introductions that simplify silicone curing workflows reduce converter cycle time and coating variability — a tangible operational benefit that supports premium pricing when proven at scale.

- Consistent event participation by European and global players highlights the continued importance of direct customer engagement for specification wins — particularly in high‑value segments such as medical and electronics.

Strategic implications and recommended actions for 2026

- Prioritize product sustainability roadmaps: Firms must accelerate development of paper‑recyclable liner formats and demonstrate lifecycle improvements to stay eligible for large contracts subject to EPR and other packaging mandates. Targeted capex next year should emphasize trials and scalability rather than incremental line upgrades.

- Hedge and diversify raw material exposure: Locking in multi‑tier supplier agreements for both pulp and silicone raw materials, combined with flexible co‑manufacturing arrangements, will blunt price shocks while enabling volume elasticity for new products.

- Differentiate through coating science: Investments in silicone application technology and curing optimization deliver measurable downstream savings for converters — use these technical differentials in negotiations to protect margin and reduce churn.

- Use M&A selectively to accelerate capability: With moderate market concentration, bolt‑on acquisitions of specialty converters, coating houses, or regional mills can accelerate geographic market access without the integration drag of full‑scale greenfield builds.

- Operationalize regulatory readiness: Embed compliance costs into pricing models and sales contracts now. Create product SKU families that map to known EPR and packaging requirements to avoid last‑minute redesigns and contractual penalties.

How PW Consulting’s report delivers value in practice

This report translates macro forecasts, technology analysis, and regulatory scenarios into a compact set of decision support tools: ROI calculators for new line investments, supplier scorecards for procurement negotiations, an M&A screening matrix, and a commercial launch checklist for sustainable liner SKUs. Rather than a catalog of disaggregated market shares, the deliverables are engineered to answer the question that matters in 2026: "Where should we place our next dollar to maximize defensible margin, regulatory access, and growth optionality?"

High Performance Liner Release Paper Market

What readers will not find — and why

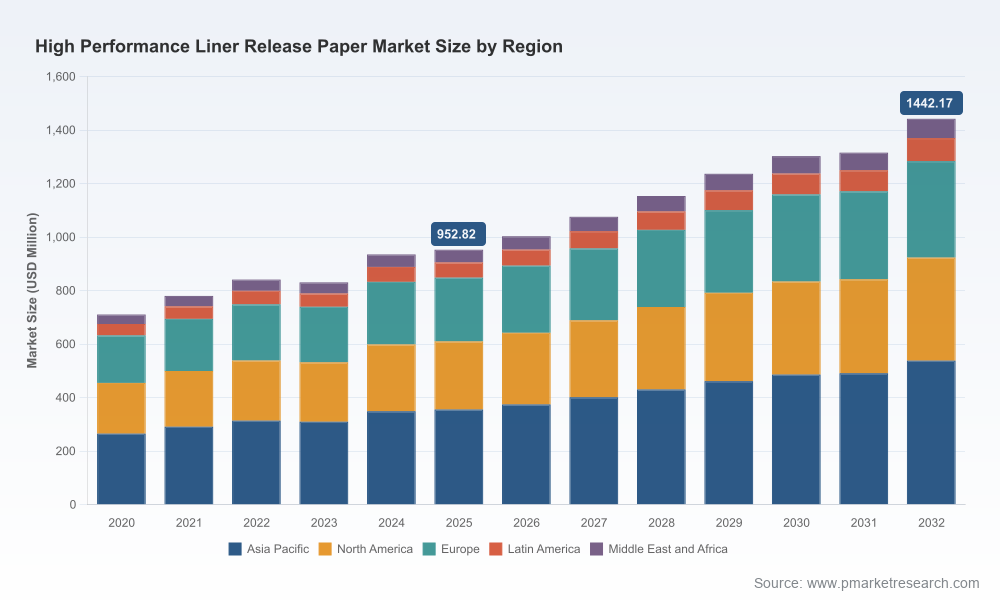

In keeping with the "trailer" principle, this public briefing intentionally omits detailed segmented tables and exact regional/application revenue splits that appear in the full report. Those granular breakdowns — including substrate‑by‑application matrices, converter pricing bands, and region‑level demand curves — are preserved for subscribers and consulting engagements, where they can be delivered with bespoke interpretation and confidentiality protections.

Final takeaway — immediate next steps for 2026 planning

- Incorporate regulatory scenario outputs into your 2026 budget and product roadmap reviews.

- Prioritize pilot programs for recyclable and optimized‑curing liner grades and secure limited supply agreements to prove scale economics.

- Use the benchmarking KPIs in the report to identify the top two operational improvements that will drive margin recovery if raw material costs rise again.

- Consider targeted M&A or strategic partnerships to accelerate entry into premium niches where coating competency and regulatory readiness command a premium.

For senior executives evaluating capital allocation, supply chain and product strategy in 2026, PW Consulting’s High Performance Liner Release Paper Market report converts macro momentum and regulatory inflection points into a clear, prioritized set of actions. To access the full dataset, regional and application breakdowns, and the toolkits mentioned above, please visit our report page or contact our industry advisory team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:High Performance Liner Release Paper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com