Disposable Supplies Market Trends and Competitive Insights 2026–2034

Home |

2026-06-23 14:06:39

PW Consulting today publishes its flagship market intelligence briefing on the Polyalkylene Glycol (PAG) compressor oil market, delivering a compact yet operationally focused view that senior executives, procurement leads, product managers and M&A teams can use immediately in 2026 planning cycles. The report blends a rigorous market model with scenario-tested commercial playbooks, regulatory impact assessments and supplier-side scorecards — enough insight to inform strategy, while reserving the full, proprietary segmentation detail for the complete report.

Pag Compressor Oil Market

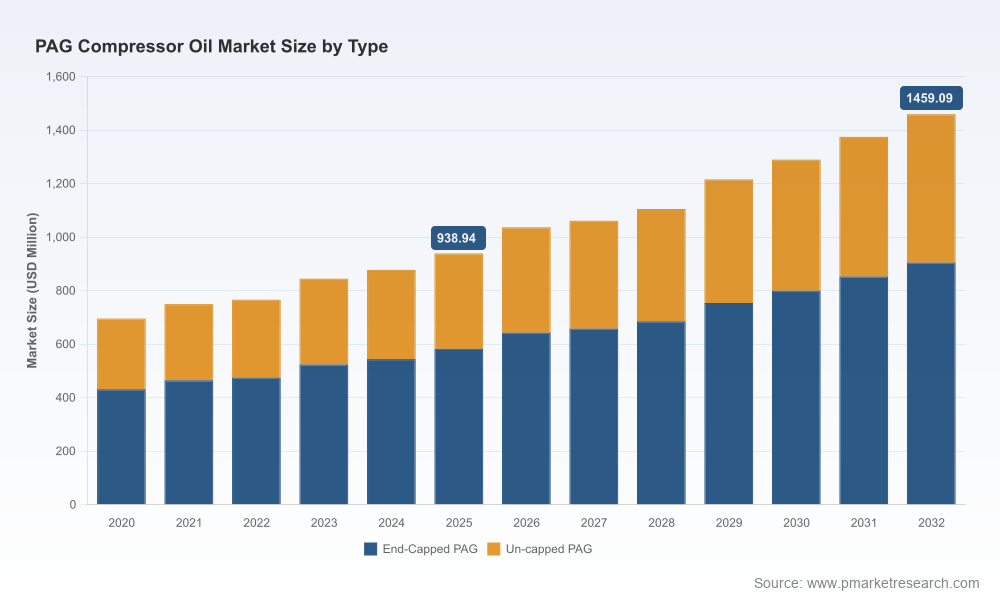

The PAG compressor oil market has moved from niche specialty to strategic ingredient. Our analysis shows the global market expanding from approximately USD 695 million in 2020 to roughly USD 939 million in 2025, with a projected increase to about USD 1,036 million in 2026 and a continued climb to an estimated USD 1,459 million by 2032. This trajectory corresponds to a compound annual growth rate of 6.51% over the 2026–2032 forecast window. For decision-makers, that profile implies both durable demand and attractive optionality for value capture — but under several conditional risks and opportunities that must be actively managed in 2026.

Pag Compressor Oil Market

PAG compressor oils are supplied by a mix of global oil majors, specialty lubricants manufacturers and chemical base-stock producers. Market concentration is meaningful but not prohibitive: the three largest suppliers control a substantive portion of global sales, and the five largest move toward a majority share, creating a mid-to-high concentration environment where scale matters but niche differentiation still wins share in technical applications.

Pag Compressor Oil Market

Strategic implications for suppliers and buyers in 2026:

Market activity over the past 24 months has been informative for strategic planning in 2026:

Recent public developments that influenced our analysis include product launches aimed at R134a and R1234yf systems, large-scale acquisitions consolidating lubricant portfolios, and multi-year launches of high-service-life air compressor oils. These events underscore two simultaneous dynamics: consolidation around scale and innovation focused on refrigerant compatibility and extreme-service performance.

Raw-material dynamics are central to margin planning for both suppliers and buyers. Polyalkylene glycol production costs rose in late 2025 amid upstream inflation and feedstock price swings. Primary feedstocks — ethylene oxide and propylene oxide — have shown volatility, and downstream polypropylene glycol pricing spikes in late 2025 reinforced margin pressures for formulators.

For 2026 procurement strategies, three levers are critical:

Two interlocking trends are accelerating product evolution and commercial decisions in 2026:

For R&D and product strategy, the immediate priorities are validated compatibility matrices, accelerated field trials with OEMs, and development of low-ash or optimized dielectric formulations for emergent compressor designs.

Our forecasting engine is purpose-built for scenario planning. Three scenarios are especially relevant to 2026 corporate planning:

Each scenario in the report is accompanied by recommended KPIs, capital allocation priorities and a 90–180 day checklist that procurement, technical and commercial teams can execute immediately.

PW Consulting’s full Pag Compressor Oil Market report contains the granular, proprietary segmentation and supplier-level data that corporates and investors need to finalize 2026 budgets, sourcing decisions and M&A screening. This release is intentionally selective — offering the strategic framing, risk context, and operational playbooks to inform immediate decisions while directing readers to the full report for transaction-grade detail.

Clients who engage with PW Consulting gain access to our interactive forecast model, supplier scorecards and bespoke scenario workshops designed to convert market intelligence into executable plans within 60 days.

For 2026, the PAG compressor oil market represents a classic strategic inflection: rising demand driven by refrigerant transitions and industrial growth, offset by upstream feedstock volatility and a competitive landscape that rewards both scale and technical differentiation. Companies that hardwire supply security, accelerate compatibility validation and align commercial models to lifecycle economics will convert the 6%+ market growth profile into sustainable share and margin expansion. PW Consulting’s report is designed to be the operational guidebook for that conversion.

For detailed analysis of this topic, please visit the official page:Pag Compressor Oil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com