PW Consulting Releases Strategic Outlook: Network Interface Controller (NIC) Market to 2032 — Essential Intelligence for 2026 Decision-Making

PW Consulting today publishes the executive summary of its forthcoming Network Interface Controller (NIC) Market Report, a practitioner-focused guide designed to inform capital allocation, procurement, and product strategy decisions through 2032. Built on detailed primary research and rigorous modelling, the study frames how NIC economics and architectures are being reshaped by hyperscale AI, cloud-native stacks, edge compute and evolving regulatory and infrastructure cost realities.

Network Interface Controller Nic Market

Headline takeaways (high-level)

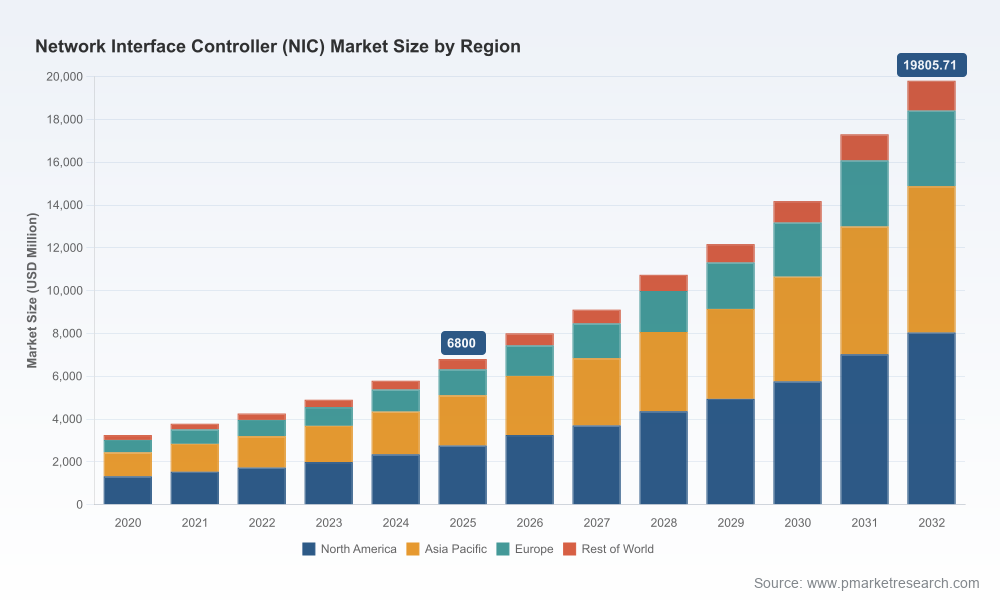

- The NIC market has accelerated materially over the past half decade, expanding from a base of approximately USD 3,250 Million in 2020 to about USD 6,800 Million in 2025 (base year).

- PW Consulting projects sustained expansion across 2026–2032 at a compound annual growth rate of 16.5%, taking total market value to roughly USD 19,806 Million by 2032 under our central scenario.

- Market concentration remains meaningful: the top-three vendor group accounts for a clear majority of market value (CR3 ~58.5%) and the top-five exceed two-thirds (CR5 ~72.2%), shaping competitive dynamics and procurement leverage.

Why this matters for enterprise and service-provider strategies in 2026

2026 is a strategic inflection point. Organizations are deciding whether to standardize on accelerated NIC architectures (SmartNICs/DPUs) as part of server refresh cycles, or to retain a mix that prioritizes unit cost and legacy software compatibility. These choices have ripple effects across data center capex, power profiles, deployment automation, and long-term vendor lock-in.

Network Interface Controller Nic Market

PW Consulting’s report translates market trajectories and vendor roadmaps into executable options that CIOs, network architects and procurement leaders can adopt this year. The analysis answers three practical questions facing executive teams:

Network Interface Controller Nic Market

- Where to allocate incremental 2026–2027 networking CAPEX to maximize application performance per watt?

- Which vendor advancements materially change total cost of ownership (TCO) and operational risk over a 3–5 year lifecycle?

- How to design procurement timelines that align with new silicon and form-factor availability without overpaying for soon-to-be-commodity features?

What the report contains — practical, actionable modules

- Proprietary market-sizing and scenario modelling: fully transparent methodology with base-year validation and sensitivity runs to stress-test growth assumptions.

- Vendor scorecards and technology maps: comparative analyses of incumbent and challenger strategies across hardware, software offload, and ecosystem support.

- TCO and energy-impact calculators: templates that integrate device power profiles with regional electricity-cost scenarios and scale factors for hyperscale deployments.

- Procurement and integration playbooks: RFP templates, test-lab validation checklists, and recommended contract clauses to mitigate software-compatibility and lifecycle risks.

- Go-to-market and M&A intelligence: signals and thresholds that indicate consolidation or vertical-integration opportunities.

Strategic themes shaping NIC demand

Our research highlights several convergent forces that will determine winners and losers through 2026 and beyond:

- Acceleration of SmartNICs and DPUs. As AI workloads and distributed storage systems demand more in-host processing, programmable NICs that offload networking, security and storage tasks are transitioning from premium niche to central platform component.

- 400GbE and higher bandwidth inflection. Higher-speed transport and corresponding host interfaces (e.g., advanced PCIe generations) are driving a refresh cycle across hyperscalers and telcos, compressing product lifecycles.

- Energy and infrastructure constraints. Rising electricity costs and utility tariff structures materially alter TCO calculations; energy now factors as heavily as acquisition price when evaluating NIC choices for large facilities.

- Supply chain and fiber investments. Large hyperscale buyers are vertically coordinating fiber and interconnect supply, reshaping demand profiles and supplier bargaining power in cabling and optics ecosystems.

- Regulatory tailwinds and simplifications. Recent policy actions that streamline network transitions reduce deployment friction for modern IP-based architectures, lowering non‑technical barriers to NIC upgrades in certain jurisdictions.

Competitive landscape — capability contrasts and implications

The competitive field is split between silicon/platform leaders, system integrators and cost-focused OEMs. Key observations from the vendor analysis:

- Intel remains a strategic anchor for many server OEMs, emphasizing Ethernet controller roadmaps that integrate higher host-interface bandwidth, deterministic features for industrial and telco edge, and broad ecosystem compatibility. Recent launches reinforce Intel’s intent to sustain relevance across both standard NIC and programmable adapter segments.

- Broadcom’s portfolio targets cloud and telco acceleration with heavy emphasis on offload features and multi‑rate support. Their integrations with PCIe Gen5/6 and virtualized network offload make them a default choice for scale-out cloud environments where mature software integration is a priority.

- NVIDIA has redefined the upper echelon of the market through its ConnectX and BlueField lineage. BlueField DPUs bring a differentiated proposition by coupling high aggregate throughput with programmable compute and security primitives—an attractive option for AI-dense clusters and hyperscale operators prioritizing workload isolation and accelerated networking stacks.

- Marvell is notable for aligning DPU throughput, CXL support and native RDMA capabilities for cloud and 5G core use cases. Their offerings are positioned to capture vendor-neutral infrastructure that demands tight storage and networking convergence.

- System integrators and traditional networking vendors (Cisco, Juniper, Fujitsu) maintain influence where bundled switching and software-defined network solutions matter, while low-cost OEMs (Realtek, TP-Link, NETGEAR) remain dominant in consumer, SMB and certain edge segments.

- Specialists (Chelsio, Silicom, Lantronix, Abaco, LR-LINK) are important for niche use-cases: offload-centric storage fabrics, ruggedized deployments, security appliances and industrial edge networking where form-factor, reliability and customization trump raw throughput.

Recent product movements reinforce the themes above: several marquee announcements through late 2025 and early 2026 indicate a near-term industry cadence toward higher-speed, programmable adapters. These vendor milestones materially compress time-to-value for adoption but also create timing risk for organizations rolling out multi-year refresh programs.

Macro context—why non‑network factors change NIC ROI

- Data center CAPEX remains enormous: independent infrastructure forecasts place global data center buildout requirements in the multiple trillions through 2030, with sizeable allocations to fiber and interconnect. This backdrop elevates the strategic importance of NIC selection within broader data center investment plans.

- Electricity and operating costs can dominate lifecycle economics for large deployments; regional rate differences and utility tariff structures can swing vendor TCO comparisons materially.

- Major hyperscalers’ procurement decisions—such as multi‑year fiber partnerships—shift entire value chains and create localized demand surges for higher-performance NICs and optics.

- Regulatory simplifications around network transitions reduce some non‑technical deployment risk, increasing the speed at which modern NIC architectures can be adopted in affected markets.

Actionable recommendations for 2026

- Prioritize proof-of-concept deployments of SmartNIC/ DPU platforms for scale-critical workloads while maintaining a tranche-based procurement schedule to capture price declines as features commoditize.

- Integrate energy-cost modelling into NIC TCO assessments; in large facilities, power efficiency can outweigh minor differences in initial acquisition cost.

- Embed software and driver support KPIs into vendor contracts to mitigate integration risk—benchmarks should include real-world offload scenarios, security primitives and failover behaviour under mixed workloads.

- Monitor vendor M&A and partnership signals closely—consolidation among the top suppliers will have downstream effects on supply timelines, warranty approaches and ecosystem lock-in.

How PW Consulting’s NIC Market Report supports your 2026 roadmap

Our report is organized as a practitioner’s toolkit: market forecasts (scenario and sensitivity models), vendor and technology playbooks, procurement templates, hands‑on deployment checklists, and energy‑aware TCO calculators. For teams planning refresh cycles or evaluating upgrades for AI, storage converged fabrics, or edge compute, the study converts market intelligence into executable steps and measurable criteria for vendor selection.

To maintain the utility of this executive brief as a strategic indicator, detailed segment-level tables and granular regional/appliance splits are intentionally reserved for the full report and supporting datasets. PW Consulting’s full delivery provides the raw forecasts, downloadable models (USD Million unit), and the proprietary scorecards necessary to embed findings into capital-plan decision processes.

Next steps

Executives weighing NIC-related investments in 2026 should: procure the full report to access the proprietary datasets and vendor scorecards; schedule a strategy workshop with PW Consulting to translate findings into a 90–180 day procurement and validation plan; and run the included TCO scenarios against your internal workload profiles and energy-cost assumptions.

PW Consulting’s Network Interface Controller Market Report is available now. The full dataset and detailed segment breakdowns—including vendor-level forecast models, scenario scripts and RFP templates—are provided as part of the commercial release to enable confident, immediate decision-making in 2026.

For detailed analysis of this topic, please visit the official page:Network Interface Controller Nic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com