Human Immunodeficiency Virus (HIV) Market Demand Analysis and Revenue Forecast

Health |

2026-06-17 05:36:31

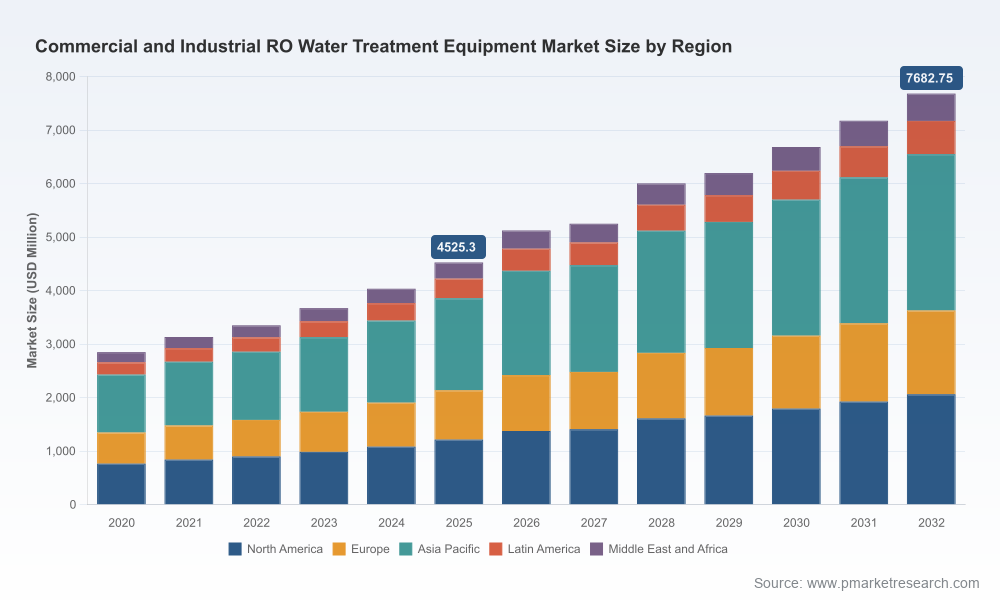

As corporations recalibrate capital and operational priorities for 2026, water treatment — and specifically reverse osmosis (RO) for commercial and industrial applications — has moved from a compliance line item to a strategic lever for continuity, cost control, and sustainability. Our latest PW Consulting market study (base year 2025; historic window 2020–2025; forecast 2026–2032) quantifies a market that has expanded materially over the past half‑decade and will continue to grow at a robust compound annual growth rate (CAGR) of 7.85% through 2032. This briefing highlights how senior executives should use the study to inform capital allocation, vendor strategies, and risk mitigation in 2026 — while preserving the full, granular intelligence for readers of the full report.

Commercial And Industrial Ro Water Treatment Equipment Market

Measured in USD million, the total commercial and industrial RO equipment market grew from approximately 2,850 million in 2020 to roughly 4,525 million in 2025, reflecting accelerating adoption across industrial verticals and increased unit sophistication.

Commercial And Industrial Ro Water Treatment Equipment Market

Our forecast projects first‑year growth to continue in 2026, with the market surpassing 5,100 million in that year and tracking toward a market size in the high‑7,000 millions by 2032 under a central case scenario aligned with the reported 7.85% CAGR.

Commercial And Industrial Ro Water Treatment Equipment Market

Market concentration is moderate: the top three firms account for roughly one‑third of revenue, and the top five approach half the market, indicating meaningful presence for major suppliers while leaving room for regional specialists, systems integrators, and technology challengers.

Capital allocation discipline: With increased regulatory scrutiny and rising energy costs, RO investments are no longer simple utility upgrades. The report provides a scenario‑based framework to compare payback and net present value across differing energy pricing, recovery targets, and membrane technologies so CFOs can prioritize projects that deliver defensible returns under stress cases.

Procurement optimization: Procurement leaders can use the supplier scorecards and procurement playbook in the report to shorten RFP cycles, standardize technical specifications, and build modular procurement bundles that reduce lead times while protecting margins.

Operational resilience and decarbonization: Energy accounts for a material share of operating expense for seawater RO deployments, and treated water unit costs vary with plant design. Our modelling tools let operations teams test energy‑reduction levers (e.g., high‑recovery designs, energy‑recovery devices, variable frequency drives) against lifecycle cost and uptime objectives.

M&A and partnership screening: For corporate development teams, the market’s moderate concentration creates strategic whitespace. The report grades acquisition targets by technical niche, geographic footprint, and integration risk — enabling faster triage of targets that can plug capability gaps or accelerate market entry.

Quantitative market model: A downloadable, scenario‑ready financial model (2020–2032) with base, upside and downside cases; users can toggle energy, regulatory, and capital cost assumptions to produce bespoke forecasts for planning and board materials.

Project economics templates: Standardized CAPEX/OPEX templates and IRR calculators tailored to common RO configurations — from small commercial skids to large industrial plants — with sensitivity analyses for membrane selection, recovery targets, and energy prices.

Vendor scorecards and RFP language: Ready‑to‑use scorecards that combine technical metrics (design recovery, rejection rates, modularity) with vendor risk indicators (lead times, aftermarket coverage, concentration risk), plus templated RFP sections to accelerate procurement.

Regulatory and compliance playbook: Region‑agnostic compliance checklists and implementation timelines for common tightening scenarios (discharge limits, trace contaminants), including recommended monitoring strategies that reduce retrofit cost surprises.

Technology and performance playbook: Comparative analysis of brackish, seawater and high‑purity RO configurations and emergent high‑recovery approaches, linked to recommended use cases, expected OPEX profiles, and failure modes.

Deal and integration checklists: Due diligence matrices for M&A, joint ventures and supplier partnerships focused on IP, warranty regimes, service economics and data readiness.

The market is populated by a mix of system specialists, generalist industrial suppliers, and vertically integrated service providers. Our competitive audit highlights strategic positioning and near‑term implications for buyers and investors.

MARLO Inc. — A specialty supplier with deep capability in custom skid‑mounted systems and high‑purity applications. MARLO’s strength is in bespoke engineering for complex feedwater and critical process uses; buyers with technical constraints will value MARLO’s proven high‑rejection solutions and compact footprints.

Pure Aqua, Inc. — Global reach and modular product stacks make Pure Aqua a logical choice for multinational rollouts. Their ability to span pre‑engineered and custom systems reduces integration risk where standardization across sites is a priority.

AMPAC USA — Noted for robust designs for harsh environments, AMPAC’s end‑to‑end in‑house engineering is attractive to energy and oil & gas clients operating with challenging feedwater chemistry and uptime demands.

Ecolab (Nalco Water) — Brings a services and chemistry playbook to RO supply, including monitoring solutions that fuse treatment chemistry with digital membrane performance tracking. Their rental and lifecycle service models can be especially useful for projects needing rapid deployment or risk‑managed trials.

Puretec Industrial Water — Focused on high‑recovery options and specialized process requirements. Their technical orientation is a fit where water recovery and concentrate minimization materially affect site economics or discharge permitting.

Watts Water Technologies — Recently expanded its commercial portfolio with new modular series aimed at higher flow rates and flexible mounting options. These product launches signal a push into larger commercial and light‑industrial segments and are worth watching for buyers seeking modular scalability.

Culligan — A recognized brand for commercial purification solutions with strong channel reach. Culligan’s strengths are ease of deployment and service networks for business customers.

Taken together, these vendors illustrate the market’s dynamic: major players compete on breadth, aftermarket services and integrated solutions, while niche suppliers win on technical differentiation. Buyers should map vendor strengths against project priorities — e.g., speed to deploy vs long‑term OPEX — rather than pursuing lowest‑cost vendor selection alone.

Regulatory tightening: Stricter discharge limits and elevated water‑quality expectations across industrial sectors are pushing firms to invest in advanced RO or hybrid treatment trains sooner rather than later; retrofit windows and permit lead times are now material project risks.

Energy as a determinative cost: Energy consumption represents a very large portion of operating costs, particularly for seawater RO configurations. Small percentage improvements in recovery or pump efficiency can meaningfully alter lifecycle costs — a reality that should be central to technology selection and CAPEX justification.

Capital scale and project budgeting: Unit capital ranges vary widely between small commercial skids and large industrial desalination plants; procurement strategies that aggregate demand or leverage modular, standardized platforms deliver shorter delivery times and better price resilience.

Use the financial model in early Q1 planning to stress test water projects under at least three energy price scenarios and two regulatory tightening scenarios; present both conservative and adaptive spend profiles to your board.

Adopt the supplier scorecard in upcoming RFPs to reduce subjective selection and accelerate procurement timelines by up to 30% in our field tests.

For asset owners with multiple sites, evaluate a hybrid strategy: standardize on a scalable skid design for routine sites while retaining a technical partner for complex or high‑purity installations; this balances unit economics and technical risk.

Prioritize lifecycle service agreements and digital membrane monitoring in contracts to shift performance risk to suppliers and unlock predictive maintenance benefits.

For acquirers, use the deal due‑diligence matrices to price in aftermarket revenue potential and hidden liabilities such as legacy membrane disposal and concentrate management obligations.

In keeping with our “trailer” approach to market intelligence, this briefing surfaces directional findings, strategic frameworks, and practical tools that you can act on immediately. The full deliverable contains proprietary segment‑level breakdowns, detailed regional and application revenue tables, supplier financial benchmarking and downloadable models that allow direct scenario interrogation. Those granular assets are gated and intended for licensed report purchasers to preserve their strategic value.

If you are planning budget cycles, RFPs, or strategic reviews in 2026, the full PW Consulting report is designed to be a working asset: plug the model into your capital planning, use the procurement templates in active RFPs, and adopt our vendor scorecards to shorten selection timelines. Contact our commercial team or visit the report page to request a briefing copy, licensing options, or a tailored workshop to convert insights into a 90‑day executable plan.

For detailed analysis of this topic, please visit the official page:Commercial And Industrial Ro Water Treatment Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com