ความสำคัญของการเลือกแพลตฟอร์มออนไลน์ที่ตอบโจทย์ผู้ใช้งานยุคปัจจุบัน

Other |

2026-03-12 17:02:35

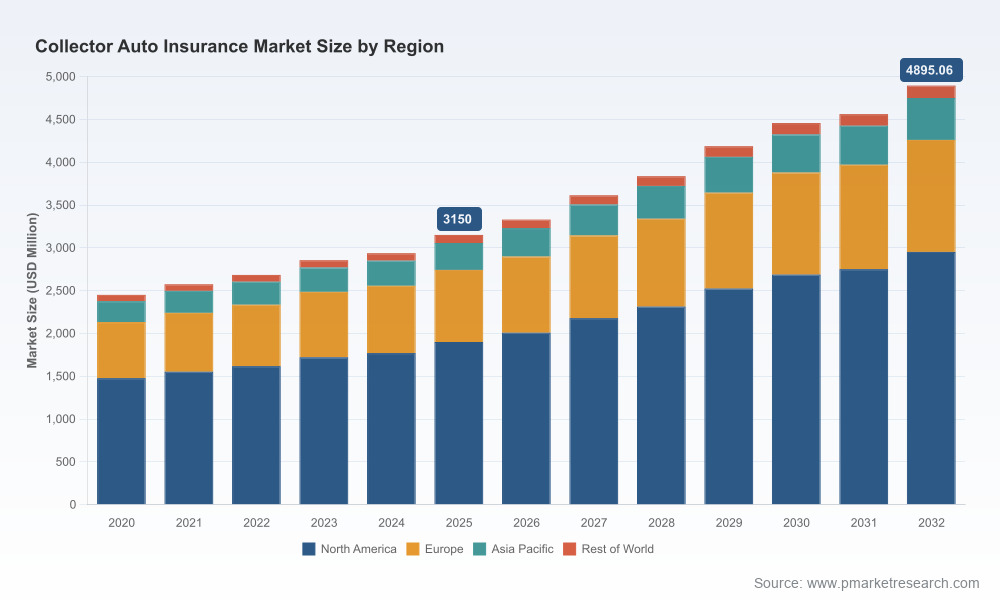

PW Consulting’s latest Collector Auto Insurance Market research — anchored on a 2025 base year with historical coverage from 2020–2025 and forecast horizon 2026–2032 — reframes how insurers, distributors, investors, and platform operators should approach the specialty collector segment in 2026. The market has expanded materially over the past half-decade, rising from roughly USD 2,450 million in 2020 to about USD 3,150 million in 2025, and under our central-case modelling is forecast to approach roughly USD 4,895 million by 2032. That trajectory implies a compound annual growth rate (CAGR) of approximately 6.5% over the forecast window — a steady, attractive growth profile for specialty underwriting and adjacent services.

Collector Auto Insurance Market

Capital allocation: Specialty collector insurance offers durable margin potential that can outperform commoditised personal lines if carriers execute disciplined underwriting, product differentiation, and targeted distribution investments.

Collector Auto Insurance Market

Partnership economics: Marketplace and OEM distribution partnerships are already reshaping access to customers and to acquisition channels — a theme that will accelerate in 2026 as platforms and insurers codify referral and fulfilment economics.

Collector Auto Insurance Market

Regulatory and data risk: State-level privacy developments and enforcement actions create immediate compliance and operational implications for usage-based pricing, telematics pilots, and analytics-driven marketing.

Consolidation opportunity: Market concentration metrics demonstrate meaningful room for scale plays and consolidation; a focused M&A agenda can be a high-impact route to accelerate premium growth and technical capability.

Our brief public summary highlights directional findings; the full PW Consulting report includes the actionable modules behind those findings. Clients will receive:

A validated market-sizing model with historical series (2020–2025) and scenario-based forecasts through 2032, enabling stress-testing against macro shocks, inflation, and hobbyist behavior shifts.

Competitive benchmarking and positioning maps across product design, distribution, claims handling, and valuation methodology — including a payback analysis for distribution partnerships and agent vs. direct acquisition channels.

Underwriting playbooks for collector portfolios: appetite matrices, agreed-value product design options, exposure controls, mileage- and usage-based endorsements, and recommended reinsurance structures for tail events.

Claims and valuation tooling: workflow blueprints for rapid damage assessment, preferred vendor networks for restoration and parts sourcing, and technology options for integrating valuation indices into adjudication engines.

Data governance and privacy compliance templates aligned with U.S. state-level developments, telematics use-case architectures that are privacy-first, and contract language to de-risk third-party analytics partnerships.

Go-to-market roadmaps for incumbents and new entrants including partnership scorecards, channel economics, and a three-year execution plan with prioritized pilot markets and KPIs.

M&A screening tools: target archetypes, integration playbooks, and illustrative valuation multiples derived from specialty-insurer precedents and current concentration dynamics.

The collector insurance ecosystem is a blend of specialist underwriters, heritage brands, and generalist insurers using partnerships to access the segment. Market concentration indicates that a relatively small group of firms account for a meaningful share of premiums, leaving scale advantages for those who can combine distribution, brand authority, and underwriting expertise.

Hagerty (Traverse City, MI): As a market-leading specialist, Hagerty’s brand and community-centric model give it privileged access to hobbyist customers and valuations expertise. Recent strategic activity — including a distribution partnership with a major carrier announced in late 2025 and strong premium growth in early 2026 — underscores an aggressive strategy to broaden reach while preserving product distinctiveness.

American Collectors Insurance (West Chester, PA): Long-standing specialist reputation combined with high-touch service makes this type of incumbent attractive to hobbyists who prioritize agreed-value certainty and concierge-style claims handling.

Grundy Insurance (Horsham, PA): Known for comprehensive coverage features and flexible mileage options, Grundy’s 2026 partnership with a collector marketplace demonstrates how platform alliances can drive direct distribution and frictionless purchase protection for buyers.

American Modern Insurance Group (Amelia, OH) & other agency-distributed specialists: These insurers leverage agency networks and specialty platforms to offer flexible products — a useful counterweight to direct-to-consumer specialists.

Heacock Classic Insurance, J.C. Taylor, Chubb, Safeco (Liberty Mutual): Each brings a differentiated angle — lifestyle focus, long-term customer relationships, HNW product packaging, or broad distribution reach via partnerships. Generalist carriers are increasingly relying on specialist partners to deliver collector-grade coverage.

Marketplace integrations: Strategic supplier arrangements between insurers and collector-vehicle marketplaces signal a shift from referral marketing to embedded protection. These integrations shorten the customer journey from discovery to coverage and increase cross-sell lifetime value.

Distribution partnerships: Hagerty’s 2025 partnership to expand distribution through a major national carrier is illustrative: incumbents with brand credibility will increasingly provide white‑label or co-branded products to mainstream carriers eager to serve collector clients without building specialist capabilities in-house.

Underwriting momentum: Public disclosures from market leaders showing double-digit premium growth in early 2026 suggest demand resilience for enthusiast-oriented products even as macro volatility persists.

Regulatory and privacy pressure: New and updated privacy laws (California, Oregon) and enforcement actions (notably activity targeting telematics data collection and sale) are already altering how insurers collect, process, and monetise driving and vehicle telemetry. Risk teams must act now to redesign data architectures with compliance by design.

2026 opens with heightened legal and regulatory scrutiny of personal and telematics data. Several U.S. state actions require insurers to re-evaluate consent flows, data retention, and monetisation strategies. For collector insurers, the practical implications include:

Revising telematics pilots to a privacy-by-default model and developing robust opt-in consent frameworks.

Updating customer communications and product disclosure templates to address state-level access, deletion, and portability requests.

Reworking vendor contracts and data-sharing agreements with telematics providers and analytics vendors to isolate compliance liability and secure data processing assurances.

Based on our analysis and scenario modelling, PW Consulting recommends that market participants prioritise the following actions this year:

Fast-track partnership pilots with marketplaces and OEM channels. Integrations that embed coverage at point-of-sale increase conversion and reduce customer acquisition costs; negotiate API-level fulfilment and clear SLA-based claims handoffs.

Invest in valuation and claims automation. Build or partner for digital valuation indices, restore-partner networks, and image-based triage tools to shorten cycle times and improve loss ratios.

Adopt a privacy-first telematics roadmap. Pivot usage-based experiments to privacy-preserving telemetry (on-device scoring, aggregate signals) and implement state-specific compliance playbooks to avoid enforcement and reputational risk.

Consider targeted M&A to capture scale and technical capabilities. Given measurable concentration at the top of the market, acquisitive strategies that add distribution or technical know-how can materially accelerate premium and margin growth.

Design tiered product architectures. Offer modular products that span hobbyist-only, limited-use collectors to high-value, unlimited-mileage policies for collection portfolios, with clear underwriting guardrails and premium segmentation.

Strengthen community and content strategies. Leverage events, valuation content, restoration guides, and trade partnerships to deepen engagement and reduce churn among passionate owners.

Specialty collector insurance combines predictable premium growth with opportunities for margin expansion through operational improvements and scale. For investors, the proposition hinges on three value levers: brand and distribution, technical underwriting, and claims efficiency. Sellers with defensible brand equity or proprietary valuation/claims capabilities command premium multiples; buyers should prioritise targets that deliver immediate distribution uplift or unique data assets that reduce loss uncertainty.

If your 2026 planning requires a defensible view of where to deploy capital, hire technical talent, or launch distribution pilots, our Collector Auto Insurance Market report provides the models, the competitive diagnostics, and the implementation templates that decision teams need. The public synopsis here intentionally abstracts granular segment-level figures; the full report contains the detailed regional, vehicle-category, and coverage-type breakouts alongside downloadable financial models and playbooks tailored for insurers, MGAs, broker-dealers, and strategic investors.

For executive briefings, model access, or enterprise licensing of the report and its datasets, PW Consulting offers direct advisory packages to translate the research into a 90-day execution plan aligned to your organization’s risk appetite and distribution strategy.

Contact PW Consulting to arrange a demonstration of the forecast model, competition maps, and sample underwriting playbooks — these resources are available to licensed report purchasers and bespoke-advisory clients.

PW Consulting’s Collector Auto Insurance Market research is designed to be both a roadmap and a springboard: it identifies where durable value sits within the specialty ecosystem, what operational and regulatory obstacles must be addressed in 2026, and which strategic moves will best position organisations to capture the market’s next phase of growth.

For detailed analysis of this topic, please visit the official page:Collector Auto Insurance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com