Modular CNG Fueling System Market: Strategic Imperatives for 2026 — PW Consulting Industry Brief

As fleets, utilities and public agencies accelerate low‑carbon transitions, modular compressed natural gas (CNG) fueling systems have moved from niche pilot projects to core infrastructure plays. PW Consulting’s latest industry study — covering historical performance from 2020–2025 and forward projections for 2026–2032 — offers the kind of operationally focused, decision‑grade intelligence that executives and investors will use to calibrate 2026 deployment and capital allocation strategies.

Modular Cng Fueling System Market

Market trajectory and what it means for 2026 decisions

Our analysis shows that the global modular CNG fueling systems market has expanded steadily in the first half of the decade, rising from USD 1,120.4 Million in 2020 to USD 1,556.7 Million in the base year 2025. Under the central scenario modeled in the report, the market is expected to continue growing through the forecast window, reaching USD 2,458.8 Million by 2032 — a compound annual growth rate (CAGR) of 6.75% for the forecast period. These headline numbers conceal meaningful structural shifts that should shape boardroom priorities in 2026:

Modular Cng Fueling System Market

- Demand is being driven by fleet electrification strategies that favor a mixed-technology approach (battery EVs where suitable; CNG/RNG where duty cycles and energy density favor gaseous fuels).

- Policy levers and fiscal incentives — both enacted and proposed — are creating asymmetries in project IRR that make near‑term infrastructure investments more attractive in certain jurisdictions.

- Modular architectures and “virtual pipeline” delivery models are materially lowering the time-to-service and initial capital required to open fueling sites, shifting the investment calculus in favor of smaller, distributed deployments.

For 2026, the strategic implication is clear: organizations that treat modular CNG as a tactical, rapidly deployable asset class — rather than a large up‑front, single-site capital program — will capture outsized benefits in operations continuity and route optimization.

Modular Cng Fueling System Market

What PW Consulting’s report delivers — practical, executable intelligence

This study is organized to support active decision‑makers. Highlights of the operational content include:

- Decomposed market sizing and confidence intervals, with sensitivity to fuel price and incentive permutations (scenarios that show how changes in natural gas commodity price and tax credits affect deployment economics).

- Unit‑level cost models for modular station builds (equipment, civil balance‑of‑plant, commissioning) and standardized templates for OPEX projections, useful for CapEx committees and project finance desks.

- A supplier benchmarking framework and vendor scorecards that rate technology maturity, delivery footprint, aftermarket capability and third‑party certification compliance (NFPA, UL, ASME and equivalent regional standards).

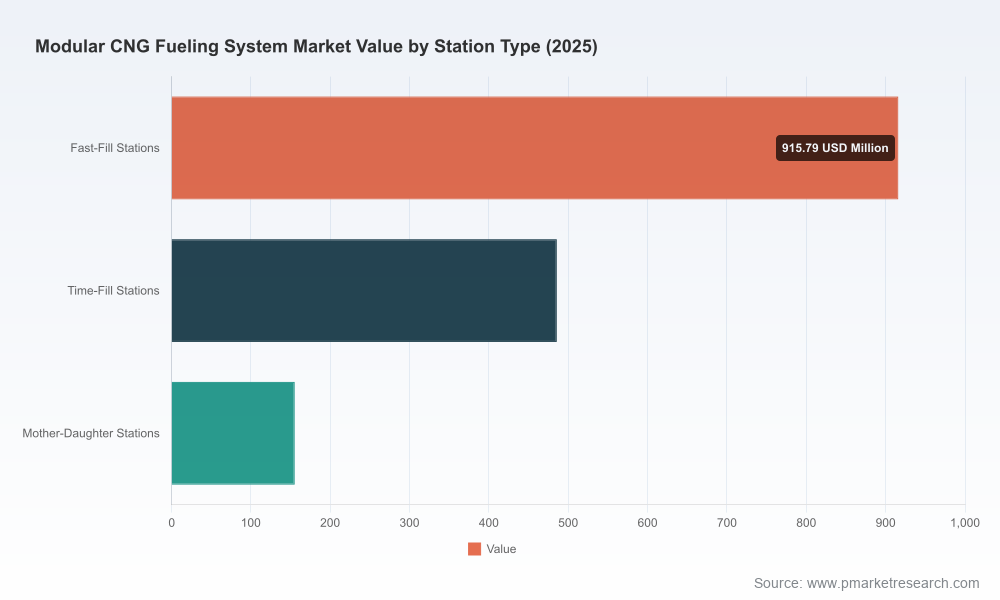

- Site selection and network optimization playbooks — including time‑fill vs. fast‑fill decision matrices, virtual pipeline integration matrices, and permitting/timeline checklists — to reduce deployment lead times from months to weeks.

- Regulatory and incentives playbooks that map the practical steps to monetize tax credits and low‑carbon fuel credits, and the compliance documentation required to secure them.

- M&A and partnership diagnostics: due diligence checklists for acquiring modular CNG providers, joint‑venture term sheets, and a short list of integration risks that typically emerge post‑close.

The report is intentionally prescriptive: each analytical chapter concludes with recommended actions tailored to operators, OEMs, developers and investors, enabling rapid translation from insight to execution.

Competitive landscape — who matters and where they play

Market concentration is moderate: the top three providers account for a meaningful share of deployed modular systems, while the top five collectively command just over half of the market. That balance produces both competitive pressure on commoditized components (compressors, storage cascades) and room for differentiation through services, integration and financing models.

Key commercial players profiled in the report — and the strategic roles they occupy in the ecosystem — include:

- CMD Alternative Energy Solutions (Appleton, Wisconsin, USA) — portable, scalable modular systems with strong compliance and telematics capabilities suited to fleet applications.

- Galileo Technologies (Argentina, global operations) — modular compression solutions with plug‑and‑play positioning and biogas compatibility that lower integration risk for RNG projects.

- BAUER Kompressoren (Munich, Germany) — turnkey module supplier with emphasis on long-term investment protection and industrial-grade compressor packages.

- ANGI Energy Systems (part of Gilbarco Veeder-Root, USA) — turnkey CNG/RNG stations with field‑tested modular architectures for heavy-duty fleet applications.

- Chart Industries (USA, global) — provider of fueling system components spanning cryogenic and modular infrastructure elements, useful for diversified fuel portfolios.

- CORE Fueling (USA) — specialist in modular and virtual pipeline CNG/RNG solutions enabling on‑site refueling for remote operations that lack traditional pipeline access.

- Neftgen (distributor of Cubogas/SNAM), GRASYS (with Aspro/DELTA), Trillium CNG (now under Love’s Alternative Energy), IMW Industries, Enric (Bengbu), Atlas Copco — each providing regional or component specialization that buyers should weigh during procurement.

Our vendor scorecards, included in the full report, go beyond marketing descriptions to show real-world delivery lead times, spare parts availability, and warranty claim performance — the kind of forensic supplier intelligence that prevents schedule slippage and latent cost overruns.

Regulatory and commodity environment shaping 2026

Policy and commodity drivers are central to near‑term economics:

- Natural gas pricing remains a critical input — Henry Hub spot prices averaged about USD 3.05/MMBtu in March 2026 — which helps preserve favorable fuel cost differentials versus diesel for many fleet routes.

- Tax incentive developments are material. Proposed IRS regulations for the Section 45Z Clean Fuel Production Credit (issued February 3, 2026) change the calculus for low‑emission transportation fuels, offering base and prevailing‑wage enhanced credits that materially improve project IRRs for eligible RNG/CNG production and sale.

- California’s Low Carbon Fuel Standard continues to reward bio‑CNG aggressively — bio‑CNG can qualify for strongly negative carbon intensity scores under the LCFS framework — unlocking incremental revenue streams that project developers can model into long‑term cash flows.

- Congressional proposals and bipartisan incentives (such as a proposed RNG vehicle fuel credit) remain in play and alter forward scenarios; the report includes breakpoints and sensitivity tables that show how different policy outcomes affect payback timelines.

Importantly for 2026 planners, some proposed rules include geographic and feedstock constraints (for example, restrictions on eligible feedstock origin under certain credit rules) that affect project eligibility — a compliance and structuring risk that must be assessed before capital commit.

Recent market activity — evidence of momentum

Several near‑term developments illustrate market momentum and the diversity of vendor roles:

- Commercial orders for auxiliary power and on‑site generation equipment are supporting compression projects in emerging markets, signaling cross‑sector demand for integrated solutions.

- Retail network expansions by major travel‑stop operators continue to add capacity at strategic highways and freight corridors, demonstrating the commercial value of modular, rapidly deployed stations.

- Public sector commissioning of municipal and waste management CNG projects shows that project types extend beyond transit: refuse fleets, regional haul, and private logistics fleets are all active adopters.

These case studies are summarized in the report with anonymized project economics and timeline charts, enabling readers to benchmark their own deployment plans against comparable projects.

Strategic recommendations for 2026

For executives setting 2026 priorities, PW Consulting recommends a three‑track approach:

- Platformize procurement: standardize on a small set of modular configurations and a common control/telemetry stack to reduce unit cost and speed replacement cycles.

- Monetize carbon: integrate LCFS, 45Z and other low‑carbon incentives into base case models and design contractual frameworks that allocate credit revenue transparently between station owner, fuel producer and fleet operator.

- Mitigate delivery risk: require supplier performance bonds or milestone‑based payments and include spare parts and service SLAs in contracts; use the vendor scorecards in the full report to shortlist suppliers for RFPs.

For investors and M&A teams, the report pins down valuation multiples by technology and service layer and highlights recurring revenue pools (service, telematics, fuel contracts) that justify higher transaction multiples for vertically integrated models.

Next steps — how to use this brief

This article is a strategic preview. The full PW Consulting Modular CNG Fueling System Market report provides the proprietary segment-level forecasts, vendor scorecards, project economics templates, and downloadable tools that permit immediate operationalization of the strategies summarized above. If your 2026 planning cycle includes station rollouts, JV negotiations, or portfolio allocation to alternative fuel infrastructure, the full report contains the granular data and executable templates required to shorten your decision timelines and de-risk implementation.

To access the complete study — including interactive scenario models, anonymized project case files, and the vendor due diligence appendices — please visit PW Consulting’s market reports page for modular CNG fueling systems.

For detailed analysis of this topic, please visit the official page:Modular Cng Fueling System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com