Car Blind Spot Surveillance Lens Market: Strategic Intelligence Briefing for 2026 — PW Consulting

PW Consulting today releases an executive briefing accompanying our full market research report on the Car Blind Spot Surveillance Lens Market. Prepared by our Advanced Mobility team, this briefing synthesizes the report’s high-consequence insights and explains why the analysis is essential for boardrooms, product leaders, procurement heads, and M&A teams planning for 2026 and beyond. The full report provides the granular segmentations, supplier scorecards, and scenario-models that we deliberately summarize here to preserve competitive value and motivate direct access to the source.

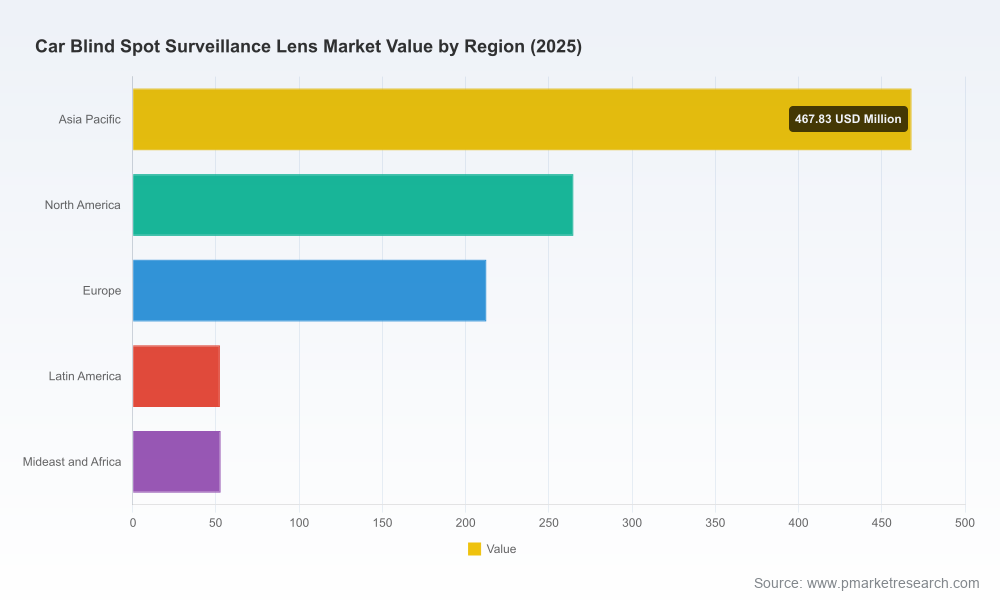

Car Blind Spot Surveillance Lens Market

Why this market matters in 2026

Blind spot surveillance lenses are a core optical component of advanced driver assistance systems (ADAS) and increasingly of vehicle camera ecosystems that enable lane-change assistance, side monitoring, and compliance with new safety mandates. Our analysis shows the market expanding from USD 719.58 Million in 2020 to USD 1,050.0 Million in 2025, and continuing to grow across the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 7.85% (base year 2025). By 2032 the market is forecast to reach approximately USD 1,782.05 Million. That trajectory underscores rising camera content per vehicle, regulatory tightness on side-object detection, and OEMs’ preference for higher-resolution sensing stacks.

Car Blind Spot Surveillance Lens Market

Top-line dynamics shaping strategy

- Regulatory acceleration: Recent policy developments — notably EU General Safety Regulation updates requiring advanced blind spot information systems (BSIS), alongside UN ECE R159 (MOIS) standards applicable to commercial vehicles — are shifting ADAS feature sets from optional differentiators into compliance-driven standard kit for many segments. Companies that move early to align optical capability and system validation with these requirements will secure first-mover advantages in OEM qualification cycles.

- Optical material and supply-chain pressures: Lightweight optical plastics such as lens-grade polycarbonate continue to be the material of choice for impact resistance and packaging economies; industry indicators point to continuing demand stress in adjacent polycarbonate markets. Procurement teams must account for lead-time volatility and variant-specific yield issues that can materially affect cost of goods sold for camera modules.

- Technology upgrade path: The shift to higher-resolution sensors (8MP and above), wider fields of view, and hybrid optical configurations increases engineering complexity but enables differentiation in surveillance performance. Lens architects and system integrators who can demonstrate validated performance under thermal, ingress, and optical distortion envelopes will win OEM design wins.

- Moderate market concentration: The market shows middle-tier concentration dynamics (our concentration ratios indicate a meaningful presence of established players but with substantial room for specialized entrants). This competitive topology creates opportunities for focused players to capture niche OEM programs or aftermarket channels while larger suppliers pursue scale-based contracts.

Competitive landscape — what matters to decision-makers

The report examines profiles, capability maps, and go-to-market postures of incumbent optics specialists, automotive Tier-1s, and aftermarket suppliers. Among the companies we analyze in depth are:

Car Blind Spot Surveillance Lens Market

- Wintop Optics (China): Focused on automotive camera lenses for side-view and blind spot use cases, Wintop’s strengths include wide-FOV and high-resolution optical designs tailored for truck and vehicle ADAS applications. Their orientation toward ADAS optics and relationships in regional supply chains make them a noteworthy competitor for volume programs.

- Tesoo Optical (China): A manufacturer with an emphasis on ruggedization (including high ingress protection and extended temperature ranges). Tesoo is positioned to serve OEMs and commercial vehicle integrators prioritizing durability and environmental performance.

- Sunny Automotive Optech (China): A high-volume lens supplier with OEM relationships across premium vehicle programs. Sunny’s announced capacity expansions and integration with camera subsystem providers underscore their intent to capture Level 2+ ADAS content increases.

- Robert Bosch GmbH (Germany): Bosch’s systems-level expertise means their lens technology is often packaged inside broader blind spot detection solutions, combining sensing, calibration, and functional safety credentials attractive to global OEMs.

- Continental AG (Germany): Continental integrates lens and camera modules into ADAS portfolios; their strength is in end-to-end system validation and scale for passenger and commercial vehicle platforms.

- Rostra (USA): A major aftermarket provider of dual-camera blind spot systems; Rostra’s low-profile CMOS camera offerings serve retrofit demand and markets where aftermarket penetration remains attractive.

- EverFocus Electronics (Taiwan): Offers dual-lens smart camera solutions compliant with EU BSIS standards for commercial vehicles, representing a specialist route-to-market for fleet OEMs and telematics integrators.

Recent developments underscore these dynamics: in January 2026 Garmin launched a dual-camera system for trucks combining blind-spot monitoring with incident recording, while in February 2026 Sunny Optical Technology announced a dedicated automotive lens production line for 8MP ADAS cameras. Both moves highlight how product innovation and capacity positioning are being used to capture accelerating demand in higher-resolution blind spot applications.

What the PW Consulting report delivers (operationally focused)

- Macro-to-micro market model: time-series demand and supply balances across 2020–2032 (base year 2025), including price, content-per-vehicle scenarios, and sensitivity to sensor resolution migration.

- Regulatory impact assessment: mapped to product requirements and validation timelines for BSIS and MOIS-type standards, with implications for component-level certification strategies.

- Technology deep-dive: optical architectures (glass, hybrid, polymer), manufacturing process trade-offs, tolerance stacks, and integration challenges for thermal/ingress resilience.

- Cost and procurement playbook: bill-of-materials benchmarking, supplier cost-driver decomposition, and levers for supplier negotiation under constrained polycarbonate supply dynamics.

- Competitive scorecards: capability matrices, qualification timelines, and likely OEM pairing scenarios for global and regional suppliers (note: detailed scorecard appendices are exclusive to the full report).

- Commercial scenarios & investment roadmaps: three market adoption scenarios tied to ADAS content uplift, with implicated R&D spend, capacity investments, and break-even timelines for new lens lines.

- M&A and partnership screening: target prioritization criteria for acquirers and strategic partnership templates to bridge capability gaps (optics, coating, and system calibration competencies).

Strategic imperatives for 2026

- Align engineering roadmaps with regulation-driven specs: OEM and Tier-1 procurement timelines will be compressed by regulatory adoption. Suppliers should prioritize test labs, functional safety traceability, and certification pathways now to be present in 2026-2027 qualification cycles.

- Design for modularity: Given the bifurcation between mass-market passenger vehicles and commercial fleets, companies should pursue modular optical platforms that enable scale while accommodating different environmental and resolution requirements.

- Secure polymer supply and secondary sources: With continued demand for lens-grade polycarbonate and episodic supply pressure in adjacent markets, dual-sourcing strategies and longer-term offtake agreements will be critical to stabilize COGS and time-to-market.

- Differentiate with systems integration: Pure optical IP is necessary but not sufficient — value accrues to players who can demonstrate reduced system calibration time, improved distortion correction, and robust field diagnostics that ease OEM integration.

- Prepare M&A playbooks focused on capability gaps: Strategic acquisitions of niche optical coating houses, thermal-stable polymer labs, or specialized calibration software firms can fast-track system-level credentials and OEM acceptance.

How to use this intelligence

For executives, this briefing should be treated as a directional framework: it identifies where investment, procurement, and product priorities should land in order to capture the upside from regulatory adoption and ADAS content migration. For strategy and BD teams, the report’s supplier scorecards and scenario models provide templates to assess which partnerships or acquisitions will most effectively close capability gaps.

Importantly, in line with our “trailer” approach, this briefing highlights the insights that will most influence 2026 decisions while withholding the fine-grained, segment-level numerical breakouts and supplier-specific margin models contained in the full PW Consulting report. Those granular datasets — including subsegment revenue breakouts, regional and application splits, and supplier-specific financial proxies — are available in the complete release and are essential for transaction diligence or a definitive sourcing strategy.

Next steps

- Procurement leaders: request the report appendices for BOM-level cost drivers to inform 2026 sourcing cycles.

- Product and engineering heads: engage PW Consulting for a tailored workshop to map your optical roadmap against regulatory certification windows.

- M&A and corporate development: commissioning our target-screening module will prioritize acquisition candidates against your capability and geographic needs.

To access the full Car Blind Spot Surveillance Lens Market report, including complete segmentation, supplier scorecards, and dynamic scenario models, visit the PW Consulting report page or contact our Advanced Mobility practice. The detailed datasets and appendices are designed to convert these strategic signals into execution-ready decisions for 2026.

For detailed analysis of this topic, please visit the official page:Car Blind Spot Surveillance Lens Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com